2.13.8. Other Papers

Miscellaneous short examples from various texts.

2.13.8.1. Contents

2.13.8.2. Wang on the Wang Transform

Source paper: Wang [2000].

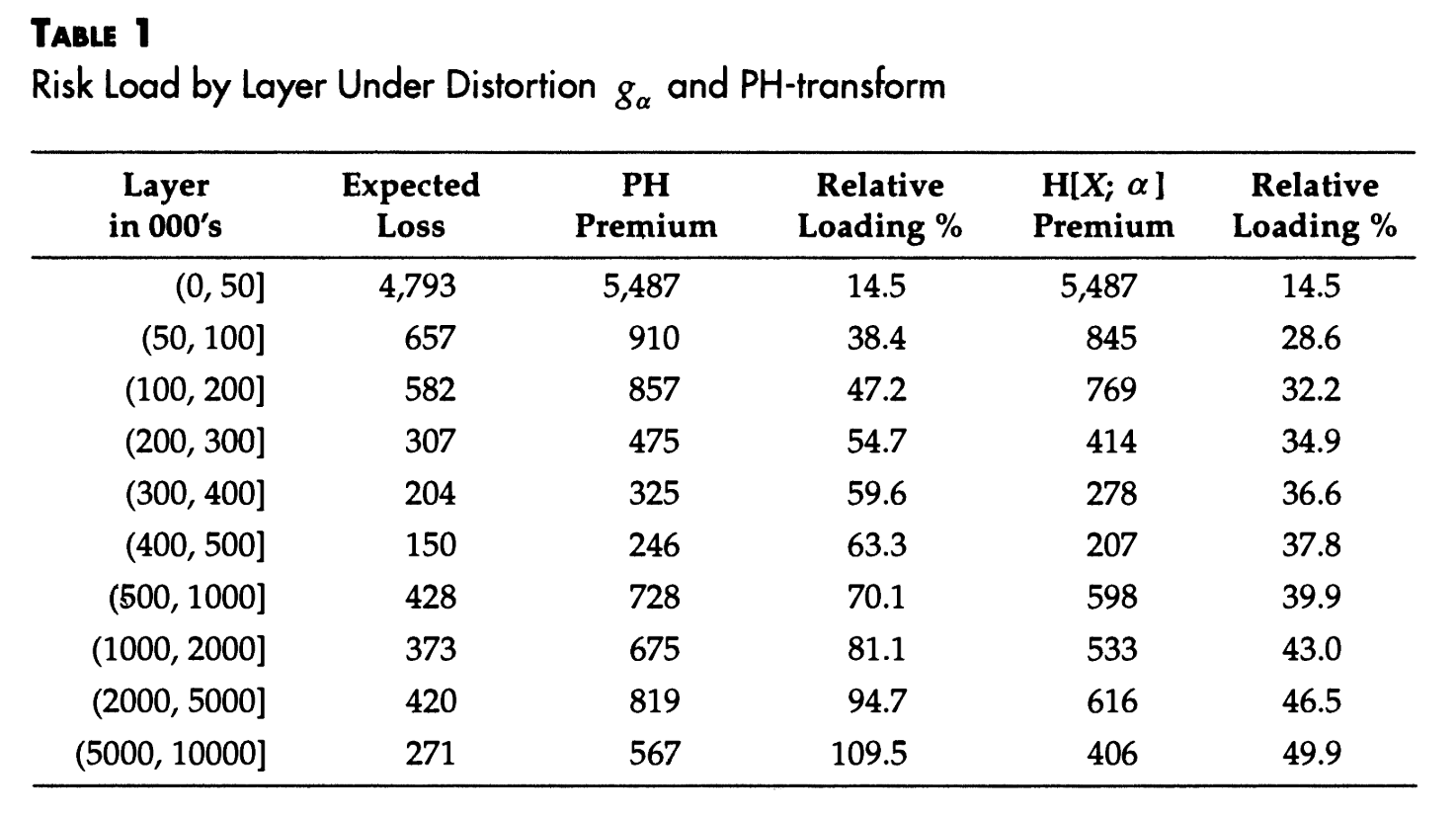

2.13.8.2.1. Pricing by Layer

Concepts: Layer expected loss and risk adjusted layer technical premium with Wang and proportional spectral risk measures.

Setup: Ground-up Pareto risk, shape 1.2, scale 2000. Layer and compare Wang(0.1) and PH(0.9245) pricing.

Source Exhibits:

Thanks: Zach Eisenstein of Aon.

Code:

Build the portfolio.

In [1]: from aggregate import build, qd

In [2]: layers = [0, 50e3, 100e3, 200e3, 300e3, 400e3, 500e3, 1000e3, 2000e3, 5000e3, 10000e3]

In [3]: a1 = build('agg Wang.t1 '

...: '1 claim '

...: '10000e3 xs 0 ' # limit the severity to avoid infinite variance

...: 'sev 2000 * pareto 1.2 - 2000 '

...: f'occurrence ceded to tower {layers} '

...: 'fixed'

...: )

...:

In [4]: qd(a1)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1 0

Sev 8179.5 8178.5 -0.00012201 11.595 11.596 70.841 70.841

Agg 8179.5 8178.5 -0.00012201 11.595 11.596 70.841 70.841

log2 = 16, bandwidth = 200, validation: n/a, reinsurance.

Expected loss and other ceded statistics by layer.

In [5]: ff = lambda x: x if type(x)==str else (

...: f'{x/1e6:,.1f}M' if x >= 500000 else

...: (f'{x:,.3f}' if x < 100 else f'{x:,.0f}'))

...:

In [6]: fp = lambda x: f'{x:.1%}'

In [7]: qdl = lambda x: qd(x, index=False, line_width=200, formatters={'pct': fp},

...: float_format=ff, col_space=10)

...:

In [8]: qdl(a1.reinsurance_occ_layer_df .xs('ceded', 1, 1).droplevel(0).reset_index(drop=False))

limit attach ex cv en severity pct

50,000 0.000 4,787 1.908 1.000 4,787 58.5%

50,000 50,000 657 8.058 0.020 32,776 8.0%

100,000 100,000 582 12.148 0.009 65,143 7.1%

100,000 200,000 307 17.279 0.004 78,055 3.8%

100,000 300,000 204 21.484 0.002 83,955 2.5%

100,000 400,000 150 25.182 0.002 87,349 1.8%

0.5M 0.5M 428 31.751 0.001 324,046 5.2%

1.0M 1.0M 373 48.091 0.001 0.6M 4.6%

3.0M 2.0M 420 76.476 0.000 1.7M 5.1%

5.0M 5.0M 271 126 0.000 3.2M 3.3%

infM gup 8,179 11.596 1.000 8,179 100.0%

ZE provided function to make the exhibit table. The column pct shows the relative loading.

In [9]: def make_table(agg, layers):

...: agg_df = agg.density_df

...: layer_df = agg_df.loc[layers, ['F', 'S', 'lev', 'gS', 'exag']]

...: layer_df['layer_el'] = np.diff(layer_df.lev, prepend = 0)

...: layer_df['premium'] = np.diff(layer_df.exag, prepend = 0)

...: layer_df['pct'] = layer_df['premium'] / layer_df['layer_el'] - 1

...: layer_df = layer_df.rename_axis("exhaust").reset_index()

...: layer_df['attach'] = layer_df['exhaust'].shift(1).fillna(0)

...: qdl(layer_df.loc[1:, ['attach', 'exhaust', 'layer_el', 'premium', 'pct']])

...:

Make the distortions and apply. First, Wang.

In [10]: d1 = build('distortion wang_d1 wang 0.1')

In [11]: a1.apply_distortion(d1)

In [12]: make_table(a1, layers)

attach exhaust layer_el premium pct

0.000 50,000 4,787 5,481 14.5%

50,000 100,000 657 845 28.6%

100,000 200,000 582 769 32.2%

200,000 300,000 307 414 34.9%

300,000 400,000 204 278 36.6%

400,000 0.5M 150 207 37.8%

0.5M 1.0M 428 598 39.9%

1.0M 2.0M 373 533 43.0%

2.0M 5.0M 420 616 46.5%

5.0M 10.0M 271 406 49.9%

Make the distortions and apply. Second, PH.

In [13]: d2 = build('distortion wang_d2 ph 0.9245')

In [14]: a1.apply_distortion(d2)

In [15]: make_table(a1, layers)

attach exhaust layer_el premium pct

0.000 50,000 4,787 5,480 14.5%

50,000 100,000 657 910 38.4%

100,000 200,000 582 856 47.2%

200,000 300,000 307 475 54.7%

300,000 400,000 204 325 59.6%

400,000 0.5M 150 246 63.3%

0.5M 1.0M 428 727 70.1%

1.0M 2.0M 373 675 81.1%

2.0M 5.0M 420 818 94.7%

5.0M 10.0M 271 567 109.5%

It appears the layer 50000 xs 0 is reported incorrectly in the paper.

2.13.8.2.2. Satellite Pricing

Concepts: The cost of a Bernoulli risk with a 5% probability of a total loss of $100m using Wang(0.1) distortion.

Thanks: Zach Eisenstein of Aon.

Code:

Build the portfolio. Illustrates how to set up a Bernoulli.

In [16]: a2 = build('agg wang2 0.05 claims dsev [100] bernoulli')

In [17]: qd(a2)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.05 4.3589 4.1295

Sev 100 100 0 0 0

Agg 5 5 8.8818e-16 4.3589 4.3589 4.1295 4.1295

log2 = 8, bandwidth = 1, validation: not unreasonable.

Check the distribution output.

In [18]: qd(a2.density_df.query('p_total > 0')[['p_total', 'F', 'S']])

p_total F S

loss

0.0 0.95 0.95 0.05

100.0 0.05 1 0

Build and apply the distortion. Use the price() method. The first argument selects the 100% quantile for pricing, i.e., the limit is fully collateralized. First with the Wang from above. The relative loading reported is the complement of the loss ratio.

In [19]: qd(a2.price(1, d1))

statistic L P M Q a LR PQ ROE

line

wang2 5 6.1191 1.1191 93.881 100 0.81712 0.065179 0.01192

Try with a more severe distortion.

In [20]: d3 = build('distortion wang_d2 wang 0.15')

In [21]: qd(a2.price(1, d2))

statistic L P M Q a LR PQ ROE

line

wang2 5 6.269 1.269 93.731 100 0.79758 0.066883 0.013539

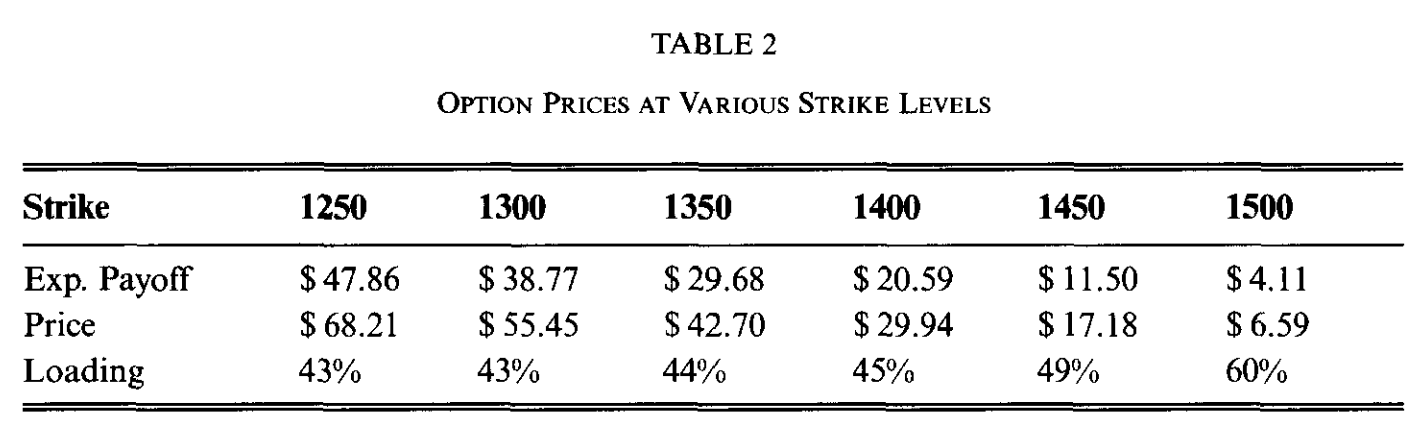

2.13.8.3. Wang on Weather Derivatives

Source paper: Wang [2002].

Concepts: Applying Wang transform to empirical distribution via an Aggregate object.

Source Exhibits:

Data:

Create a dataframe from the heating degree days (HDD) history laid out in Table 1.

In [22]: d = '''Dec-79

....: 972.5

....: Dec-87

....: 1018.5

....: Dec-95

....: 1199.5

....: Dec-80

....: 1147.0

....: Dec-88

....: 1155.0

....: Dec-96

....: 1156.0

....: Dec-81

....: 1244.0

....: Dec-89

....: 1474.5

....: Dec-97

....: 1040.0

....: Dec-82

....: 901.0

....: Dec-90

....: 1129.5

....: Dec-98

....: 940.5

....: Dec-83

....: 1573.0

....: Dec-91

....: 1077.5

....: Dec-99

....: 1090.5

....: Dec-84

....: 1055.0

....: Dec-92

....: 1129.5

....: Dec-00

....: 1517.5

....: Dec-85

....: 1488.0

....: Dec-93

....: 1090.5

....: Dec-86

....: 1065.5

....: Dec-94

....: 938.5'''

....:

In [23]: import pandas as pd

In [24]: d = d.split('\n')

In [25]: df = pd.DataFrame(zip(d[::2], d[1::2]), columns=['month', 'hdd'])

In [26]: df['hdd'] = df.hdd.astype(float)

In [27]: qd(df.head())

month hdd

0 Dec-79 972.5

1 Dec-87 1018.5

2 Dec-95 1199.5

3 Dec-80 1147

4 Dec-88 1155

In [28]: qd(df.describe())

hdd

count 22

mean 1154.7

std 193.37

min 901

25% 1043.8

50% 1110

75% 1188.6

max 1573

Code:

Create an empirical aggregate based on the HDD data.

In [29]: hdd = build(f'agg HDD 1 claim dsev {df.hdd.values} fixed'

....: , bs=1/32, log2=16)

....:

In [30]: qd(hdd)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1 0

Sev 1154.7 1154.7 2.2204e-16 0.16362 0.16362 0.95984 0.95984

Agg 1154.7 1154.7 2.2204e-16 0.16362 0.16362 0.95984 0.95984

log2 = 16, bandwidth = 1/32, validation: not unreasonable.

Build the distortion and apply to call options at different strikes. Reproduces Table 2.

In [31]: from aggregate.extensions import Formatter

In [32]: d1 = build('distortion w25 wang .25')

In [33]: ans = []

In [34]: strikes = np.arange(1250, 1501, 50)

In [35]: bit = hdd.density_df.query('p_total > 0')[['p_total']]

In [36]: for strike in strikes:

....: ser = bit.groupby(by= lambda x: np.maximum(0, x - strike)).p_total.sum()

....: ans.append(d1.price(ser, kind='both'))

....:

In [37]: df = pd.DataFrame(ans, index=strikes,

....: columns=['bid', 'el', 'ask'])

....:

In [38]: df.index.name = 'strike'

In [39]: df['loading'] = (df.ask - df.el) / df.el

In [40]: qd(df.T, float_format=Formatter(dp=2, w=8))

strike 1250 1300 1350 1400 1450 1500

bid 32.01 25.84 19.67 13.51 7.34 2.44

el 47.86 38.77 29.68 20.59 11.50 4.11

ask 68.21 55.45 42.70 29.94 17.18 6.59

loading 42.5% 43.0% 43.8% 45.4% 49.4% 60.1%

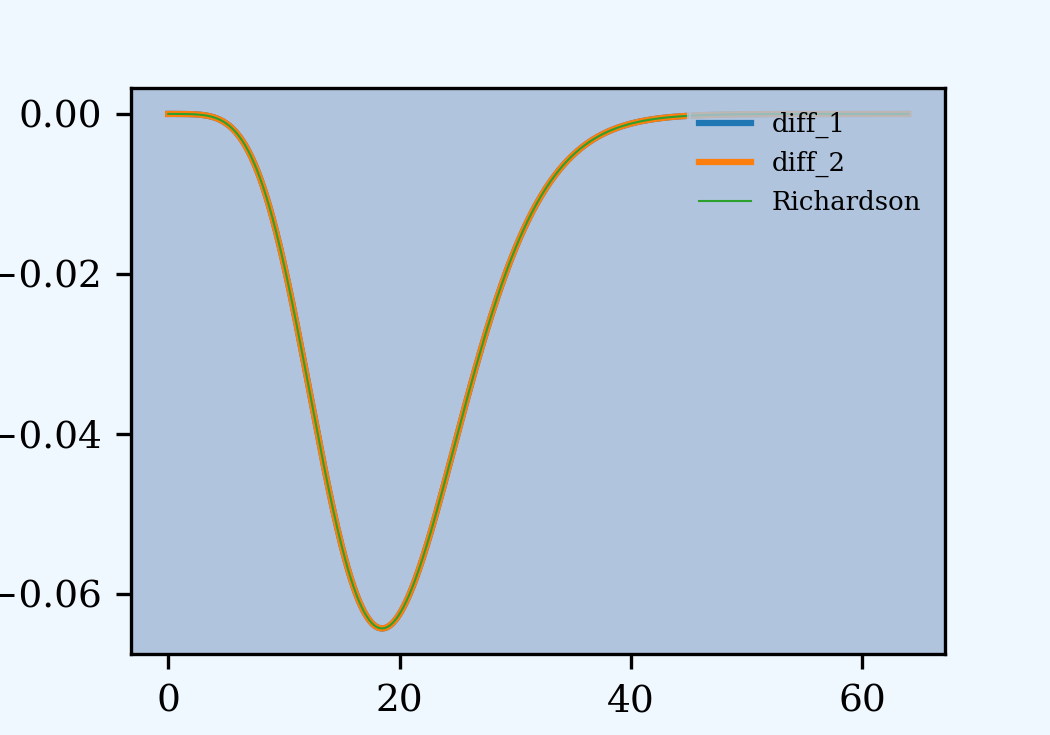

2.13.8.5. Richardson’s Deferred Approach to the Limit

Source papers: Embrechts et al. [1993], Grübel and Hermesmeier [2000].

Concepts: Given estimators of an unknown quantity \(A^* = A(h) + ch^\alpha + O(h^\beta)\) with \(\alpha < \beta\). Evaluate at \(h\) and \(h/t\). Multiply the estimate at \(h/t\) by \(t^\alpha\), subtract the original estimate, and rearrange to get

The truncation error order of magnitude has decreased. The constant \(c\) need not be known. Applying this approach to estimate the density as pmf divided by bucket size, \(f_{h} / h\), Embrechts et al. [1993] report the following.

Setup: Poisson(20) exponential aggregate.

Source Exhibits: Figure 1.

The variable egp3 is treated as the exact answer. It could also be approximated using the series expansion, but this has been shown already, in REF. Set up basic portfolios evaluated at different bucket sizes.

In [56]: egp1 = build('agg EGP 20 claims sev expon 1 poisson',

....: bs=1/16, log2=10)

....:

In [57]: qd(egp1)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 20 0.22361 0.22361

Sev 1 0.99984 -0.00016274 1 1.0005 2 1.998

Agg 20 19.997 -0.00016277 0.31623 0.3163 0.47434 0.47429

log2 = 10, bandwidth = 1/16, validation: fails sev mean, agg mean.

In [58]: egp2 = build('agg EGP 20 claims sev expon 1 poisson',

....: bs=1/32, log2=11)

....:

In [59]: qd(egp2)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 20 0.22361 0.22361

Sev 1 0.99996 -4.0689e-05 1 1.0001 2 1.9995

Agg 20 19.999 -4.0713e-05 0.31623 0.31625 0.47434 0.47432

log2 = 11, bandwidth = 1/32, validation: not unreasonable.

In [60]: egp3 = build('agg EGP 20 claims sev expon 1 poisson',

....: log2=16)

....:

In [61]: qd(egp3)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 20 0.22361 0.22361

Sev 1 1 -1.5895e-07 1 1 2 2

Agg 20 20 -1.5895e-07 0.31623 0.31623 0.47434 0.47434

log2 = 16, bandwidth = 1/512, validation: not unreasonable.

Concatenate and estimated densities from pmf. Compute errors to egp3. Compute the Richardson extrapolation. It is indistinguishable from egp3. The last table shows cases with the largest errors.

In [62]: import pandas as pd

In [63]: df = pd.concat((egp1.density_df.p_total, egp2.density_df.p_total, egp3.density_df.p_total),

....: axis=1, join='inner', keys=[1, 2, 3])

....:

In [64]: df[1] = df[1] * 16; \

....: df[2] = df[2] * 32; \

....: df[3] = df[3] * (1<<10); \

....: df['rich'] = (4 * df[2] - df[1]) / 3; \

....: df['diff_1'] = df[1] - df[3]; \

....: df['diff_2'] = df[2] - df[3]; \

....: m = df.diff_2.max() * .9; \

....: ax = df[['diff_1', 'diff_2']].plot(figsize=(3.5, 2.45)); \

....: (df['rich'] - df[3]).plot(ax=ax, lw=.5, label='Richardson');

....:

In [65]: ax.legend(loc='upper right')

Out[65]: <matplotlib.legend.Legend at 0x71a3d41d7fa0>

In [66]: qd(df.query(f'diff_2 > {m}').iloc[::10])

Empty DataFrame

Columns: [1, 2, 3, rich, diff_1, diff_2]

Index: []