2.6. Reinsurance Pricing

Objectives: Applications of the Aggregate class to reinsurance exposure rating, including swings and slides, aggregate stop loss and swing rated programs, illustrated using problems from CAS Parts 8 and 9.

Audience: Reinsurance pricing, broker, or ceded re actuary.

Prerequisites: DecL, underwriting and reinsurance terminology, aggregate distributions, risk measures.

See also: The Reinsurance Clauses, Individual Risk Pricing. For other related examples see Published Problems and Examples, especially Bahnemann Monograph.

Contents:

2.6.1. Helpful References

2.6.2. Basic Examples

Here are some basic examples. They are not realistic, but it is easy to see what is going on. The subsequent sections add realism. The basic example gross loss is a “die roll of dice rolls”: roll a die, then roll that many dice and sum, see Student. The outcome is between 1 (probability 1/36) and 36 (probability 1/6**7), as confirmed by this output.

In [1]: import pandas as pd

In [2]: from aggregate import build, qd

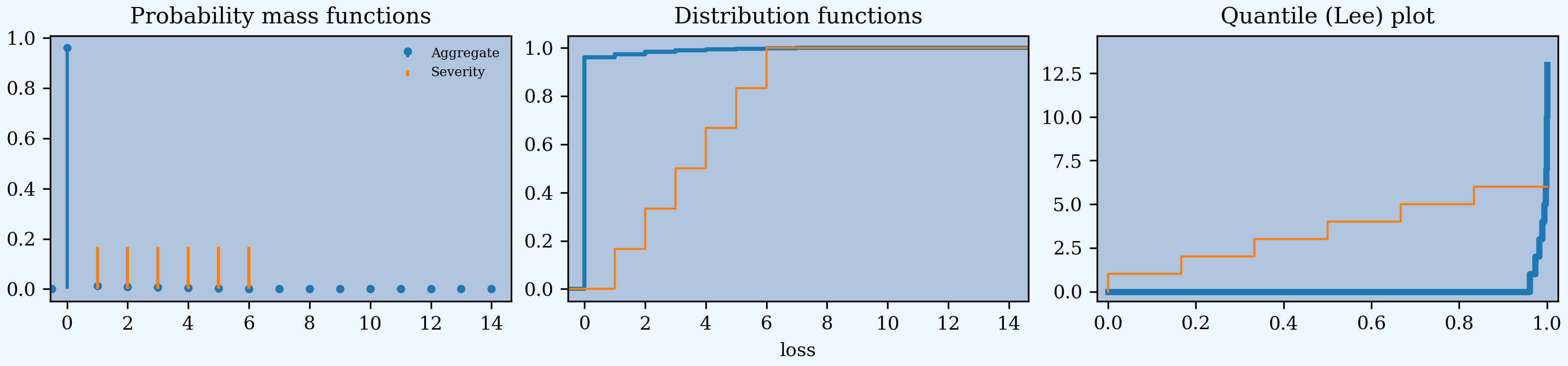

In [3]: a01 = build('agg Re:01 '

...: 'dfreq [1 2 3 4 5 6] '

...: 'dsev [1 2 3 4 5 6] ')

...:

In [4]: a01.plot()

In [5]: qd(a01)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3.5 0.48795 0

Sev 3.5 3.5 0 0.48795 0.48795 0 2.8529e-15

Agg 12.25 12.25 1.5543e-15 0.55328 0.55328 0.28689 0.28689

log2 = 7, bandwidth = 1, validation: not unreasonable.

In [6]: print(f'Pr D = 1: {a01.pmf(1) : 11.6g} = {a01.pmf(1) * 36:.0f} / 36\n'

...: f'Pr D = 36: {a01.pmf(36):8.6g} = {a01.pmf(36) * 6**7:.0f} / 6**7')

...:

Pr D = 1: 0.0277778 = 1 / 36

Pr D = 36: 3.57225e-06 = 1 / 6**7

An occurrence excess of loss reinsurance layer is specified between the severity and frequency clauses because you need to know severity but not frequency. Multiple layers can be applied at once. This example enters 2 xs 4 as two layers:

occurrence net of 1 xs 4 and 1 xs 5

Requesting net of propagates losses net of the cover through to the aggregate.

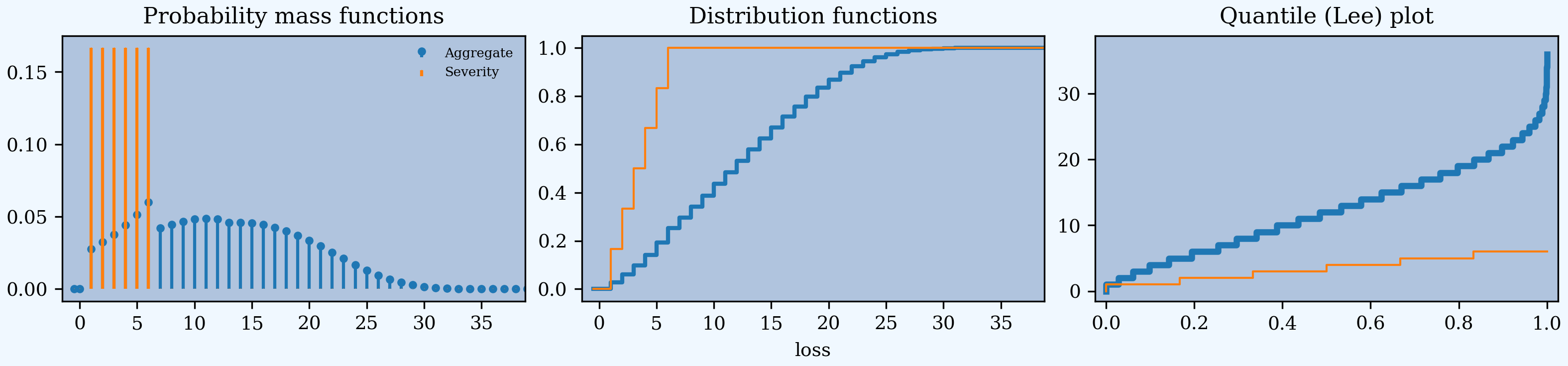

In [7]: a02 = build('agg Re:02 '

...: 'dfreq [1:6] '

...: 'dsev [1:6] '

...: 'occurrence net of 1 xs 4 and 1 xs 5')

...:

In [8]: a02.plot()

In [9]: qd(a02)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3.5 0.48795 0

Sev 3.5 3 -0.14286 0.48795 0.3849 0 -0.64952

Agg 12.25 10.5 -0.14286 0.55328 0.52955 0.28689 0.18324

log2 = 7, bandwidth = 1, validation: n/a, reinsurance.

[1:6] is shorthand for [1,2,3,4,5,6]. The net severity equals 3 = (1 + 2 + 3 + 4 + 4 + 4) / 6.

The reinsurance_audit_df dataframe shows unconditional (per ground up claim) severity statistics by layer. Multiply by the claim count a02.n to get layer loss picks. The severity, ex, equals (1 + 2) / 6 = 0.5 (first block). The expected loss to the layer equals 0.5 * 3.5 = 1.75 (second block).

In [10]: qd(a02.reinsurance_audit_df['ceded'])

ex var sd cv skew

kind share limit attach

occ 1.0 1.0 4.0 0.33333 0.22222 0.4714 1.4142 0.70711

5.0 0.16667 0.13889 0.37268 2.2361 1.7889

all inf gup 0.5 0.58333 0.76376 1.5275 1.1223

In [11]: qd(a02.reinsurance_audit_df['ceded'], sparsify=False)

ex var sd cv skew

kind share limit attach

occ 1.0 1.0 4.0 0.33333 0.22222 0.4714 1.4142 0.70711

occ 1.0 1.0 5.0 0.16667 0.13889 0.37268 2.2361 1.7889

occ all inf gup 0.5 0.58333 0.76376 1.5275 1.1223

In [12]: qd(a02.reinsurance_audit_df['ceded'][['ex']] * a02.n)

ex

kind share limit attach

occ 1.0 1.0 4.0 1.1667

5.0 0.58333

all inf gup 1.75

The reinsurance_occ_layer_df shows conditional layer expected loss and CV of loss, along with expected counts by layer and layer severity. The expected count to 1 xs 4 equals 3.5 / 3, because there is a 1/3 chance the layer attaches.

In [13]: qd(a02.reinsurance_occ_layer_df, sparsify=False)

stat ex ex ex cv cv cv en severity pct

view ceded net subject ceded net subject ceded ceded ceded

share limit attach

1.0 1.0 4.0 1.1667 11.083 12.25 1.4142 0.42433 0.48795 1.1667 1 0.095238

1.0 1.0 5.0 0.58333 11.667 12.25 2.2361 0.44721 0.48795 0.58333 1 0.047619

all inf gup 1.75 10.5 12.25 1.5275 0.3849 0.48795 3.5 0.5 0.14286

An aggregate excess of loss reinsurance layer, 12 xs 24, is specified after the frequency clause (you need to know frequency):

aggregate ceded to 12 xs 34.

Requesting ceded to propagates the ceded losses through to the aggregate. Refer to agg.Re:01 by name as a shorthand. reinsurance_audit_df reports expected loss to the aggregate layer. The layer is shown in two parts to illustrate reporting.

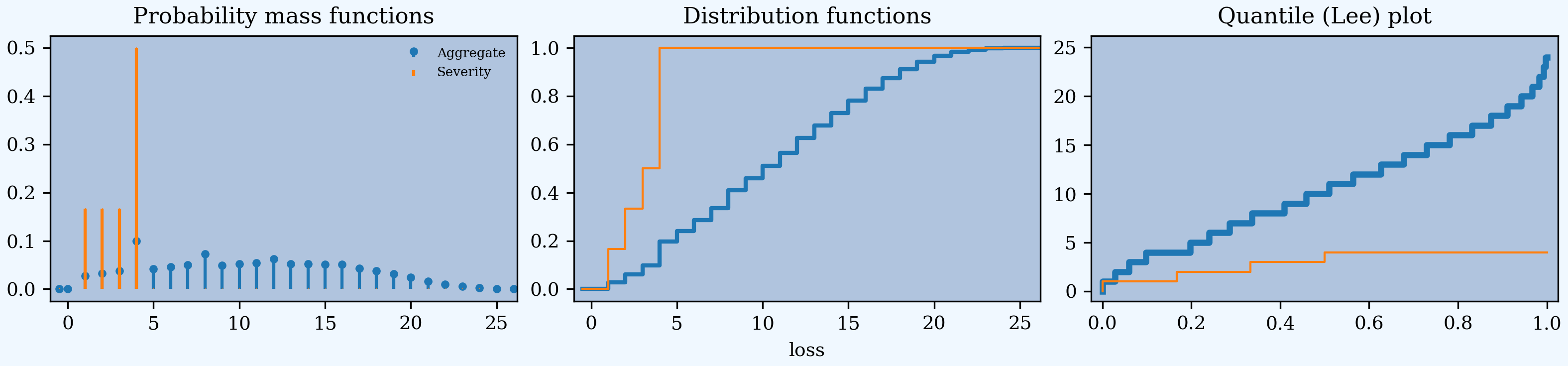

In [14]: a03 = build('agg Re:03 agg.Re:01 '

....: 'aggregate ceded to 6 xs 24 and 6 xs 30')

....:

In [15]: a03.plot()

In [16]: qd(a03)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3.5 0.48795 0

Sev 3.5 3.5 0 0.48795 0.48795 0 2.8529e-15

Agg 12.25 0.10661 -0.9913 0.55328 5.9383 0.28689 7.6018

log2 = 7, bandwidth = 1, validation: n/a, reinsurance.

In [17]: qd(a03.reinsurance_audit_df.stack(0))

ex var sd cv skew

kind share limit attach

agg 1.0 6.0 24.0 ceded 0.10378 0.36108 0.6009 5.7901 6.9432

net 12.146 43.082 6.5637 0.54039 0.15351

subject 12.25 45.938 6.7777 0.55328 0.28689

30.0 ceded 0.0028292 0.0063577 0.079735 28.183 35.705

net 12.247 45.831 6.7698 0.55277 0.27937

subject 12.25 45.938 6.7777 0.55328 0.28689

all inf gup ceded 0.10661 0.4008 0.63309 5.9383 7.6018

net 12.143 43.009 6.5581 0.54005 0.1501

subject 12.25 45.938 6.7777 0.55328 0.28689

Occurrence and aggregate programs can both be applied. The ceded to and net of clauses can be mixed. You cannot refer to agg.Re:01 by name because you need to see into the object to apply the occurrence reinsurance.

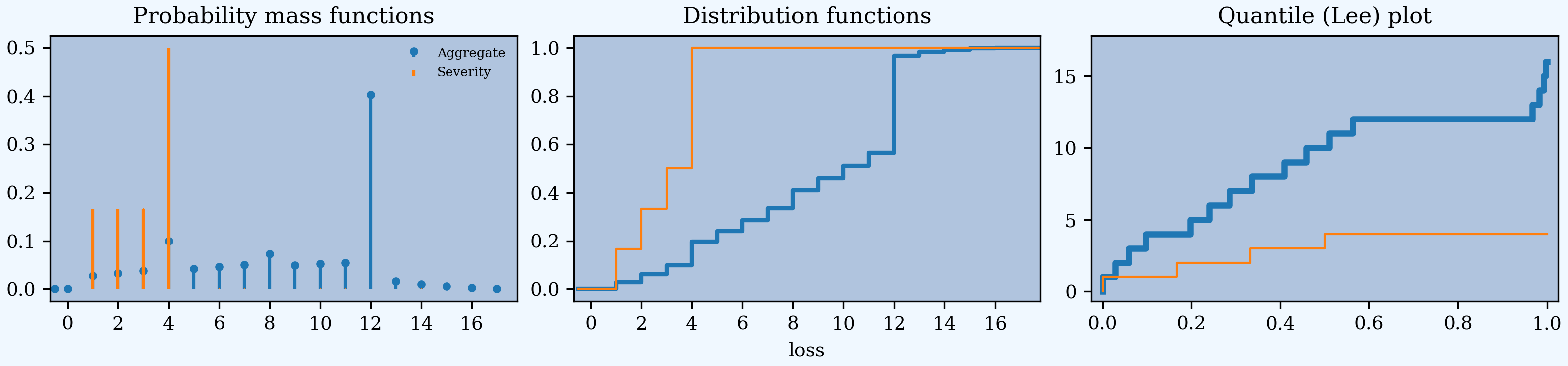

In [18]: a04 = build('agg Re:04 dfreq [1:6] dsev [1:6] '

....: 'occurrence net of 1 xs 4 and 1 xs 5 '

....: 'aggregate net of 4 xs 12 and 4 xs 16')

....:

In [19]: a04.plot()

In [20]: qd(a04)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3.5 0.48795 0

Sev 3.5 3 -0.14286 0.48795 0.3849 0 -0.64952

Agg 12.25 8.8731 -0.27566 0.55328 0.41047 0.28689 -0.61588

log2 = 7, bandwidth = 1, validation: n/a, reinsurance.

In [21]: qd(a04.reinsurance_audit_df['ceded'])

ex var sd cv skew

kind share limit attach

occ 1.0 1.0 4.0 0.33333 0.22222 0.4714 1.4142 0.70711

5.0 0.16667 0.13889 0.37268 2.2361 1.7889

all inf gup 0.5 0.58333 0.76376 1.5275 1.1223

agg 1.0 4.0 12.0 1.186 2.8219 1.6798 1.4164 0.88095

16.0 0.44087 1.1991 1.095 2.4838 2.4346

all inf gup 1.6269 6.5022 2.5499 1.5674 1.3628

Layers can be specified as a share of or part of to account for coinsurance (partial placement) of the layer:

0.5 so 2 xs 2, read 50% share of 2 xs 2, or1 po 4 xs 10, read 1 part of 4 xs 10.

Warning

aggregate works with discrete distributions. All outcomes are multiples of the bucket size, bs. Any cession is rounded to a multiple of bs. Ensure bs is appropriate to capture cessions when applying share or part of. By default build uses bs=1 when it detects a discrete distribution, such as the die roll example. Ceding to 0.5 so 2 xs 2 produces ceded losses of 0.5 and net losses of 2.5. To capture these needs a much smaller discretization grid. Non-discrete aggregates plot as though they are continuous or mixed distributions.

These concepts are illustrated in the next example. Note the bucket size.

In [22]: a05 = build('agg Re:05 '

....: 'dfreq [1:6] dsev [1:6] '

....: 'occurrence net of 0.5 so 2 xs 2 and 2 xs 4 '

....: 'aggregate net of 1 po 4 xs 10 '

....: , bs=1/512, log2=16)

....:

In [23]: a05.plot()

In [24]: qd(a05)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3.5 0.48795 0

Sev 3.5 2.4167 -0.30952 0.48795 0.30258 0 -0.98865

Agg 12.25 8.2063 -0.3301 0.55328 0.49122 0.28689 0.0035585

log2 = 16, bandwidth = 1/512, validation: n/a, reinsurance.

In [25]: qd(a05.reinsurance_audit_df['ceded'])

ex var sd cv skew

kind share limit attach

occ 0.5 2.0 2.0 0.58333 0.20139 0.44876 0.76931 -0.33297

1.0 2.0 4.0 0.5 0.58333 0.76376 1.5275 1.1223

all inf gup 1.0833 1.2014 1.0961 1.0118 0.64163

agg 0.25 4.0 10.0 0.25202 0.14516 0.38099 1.5117 1.1168

all inf gup 0.25202 0.14516 0.38099 1.5117 1.1168

A tower of limits can be specified by giving the attachment points of each layer. The shorthand:

occurrence ceded to tower [0 1 2 5 10 20 36]

is equivalent to:

occurrence ceded to 1 xs 0 and 1 xs 1 and 3 xs 2 \

and 5 xs 5 and 10 xs 10 and 16 xs 20

Here is a summary of these examples. The audit dataframe gives a layering of aggregate losses. The plot is omitted; it is identical to gross since the tower covers all losses.

In [26]: a06 = build('agg Re:06 '

....: 'agg.Re:01 '

....: 'aggregate ceded to tower [0 1 2 5 10 20 36]')

....:

In [27]: a06.plot()

In [28]: qd(a06)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3.5 0.48795 0

Sev 3.5 3.5 0 0.48795 0.48795 0 2.8529e-15

Agg 12.25 12.25 2.2204e-16 0.55328 0.55328 0.28689 0.28689

log2 = 7, bandwidth = 1, validation: n/a, reinsurance.

In [29]: qd(a06.reinsurance_audit_df['ceded'], sparsify=False)

ex var sd cv skew

kind share limit attach

agg 1.0 1.0 0.0 1 4.4409e-16 2.1073e-08 2.1073e-08 -4.7453e+07

agg 1.0 1.0 1.0 0.97222 0.027006 0.16434 0.16903 -5.747

agg 1.0 3.0 2.0 2.6997 0.64684 0.80426 0.29791 -2.6177

agg 1.0 5.0 5.0 3.5291 4.2422 2.0597 0.58361 -0.87928

agg 1.0 10.0 10.0 3.573 15.609 3.9508 1.1057 0.56831

agg 1.0 16.0 20.0 0.47593 2.2625 1.5042 3.1604 3.8783

agg all inf gup 12.25 45.938 6.7777 0.55328 0.28689

See Reinsurance Functions for more about the reinsurance functions.

2.6.3. Modes of Reinsurance Analysis

Inwards reinsurance pricing is begins with an estimated loss pick, possibly supplemented by distribution and volatility statistics such as loss standard deviation or quantiles. aggregate can help in two ways.

Excess of loss exposure rating that accounts for the limits profile of the underlying business and how it interacts with excess layers. Uses only the severity distribution through difference of increased limits factors. This application is peripheral to the underlying purpose of

aggregate, but is very convenient nonetheless.The impact of treaty variable features that are derived from the full aggregate distribution of ceded losses and expenses—a showcase application.

Outwards reinsurance is evaluated based on the loss pick and the impact of the cession on the distribution of retained losses. Ceded re and broker actuaries often want the full gross and net outcome distributions.

2.6.4. Reinsurance Functions

This section demonstrates Aggregate methods and properties for reinsurance analysis. These are:

reinsurance_kinds()a text description of the kinds (occurrence and/or aggregate) of reinsurance applied.reinsurance_description()a text description of the layers and shares, by kind.reinsurance_occ_plot()plots subject (usually gross), ceded, and net severity, and aggregates created from each. Does not consider aggregate reinsurance.reinsurance_audit_dfdataframe summary by ceded, net, and subject, showing mean, CV, SD, and skewness of occurrence loss by layer and in total by kind.reinsurance_occ_layer_dfdataframe showing an expected loss layering analysis for occurrence reinsurance.reinsurance_dfdataframe showing all possible densities.reinsurance_report_dfdataframe showing mean, CV, skew, and SD statistics for each column inreinsurance_df.

These are illustrated using the a more realistic example that includes occurrence and aggregate reinsurance. Notice that the occurrence program just layers gross (subject) losses. Gross losses are then passed through to the aggregate program. This is done to illustrate the functions below. In a real-world application is is likely the bottom few occurrence layers would be dropped and you would pass the net of through to the aggregate.

In [30]: from aggregate import build, qd

In [31]: a = build('agg ReTester '

....: '10 claims '

....: '5000 xs 0 '

....: 'sev lognorm 100 cv 5 '

....: 'occurrence ceded to 250 xs 0 and 250 xs 250 and 500 xs 500 and 1000 xs 1000 and 3000 xs 2000 '

....: 'poisson '

....: 'aggregate ceded to 250 xs 750 and 1500 xs 1000 '

....: )

....:

In [32]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 10 0.31623 0.31623

Sev 95.058 95.057 -2.0186e-06 3.2307 3.2307 9.4329 9.4329

Agg 950.58 310.2 -0.67367 1.0695 1.7183 2.8646 1.7399

log2 = 16, bandwidth = 1/2, validation: n/a, reinsurance.

In [33]: print(a.reinsurance_kinds())

Occurrence and aggregate

In [34]: print(a.reinsurance_description())

Ceded to 100% share of 250 xs 0 and 100% share of 250 xs 250 and 100% share of 500 xs 500 and 100% share of 1,000 xs 1,000 and 100% share of 3,000 xs 2,000 per occurrence then ceded to 100% share of 250 xs 750 and 100% share of 1,500 xs 1,000 in the aggregate.

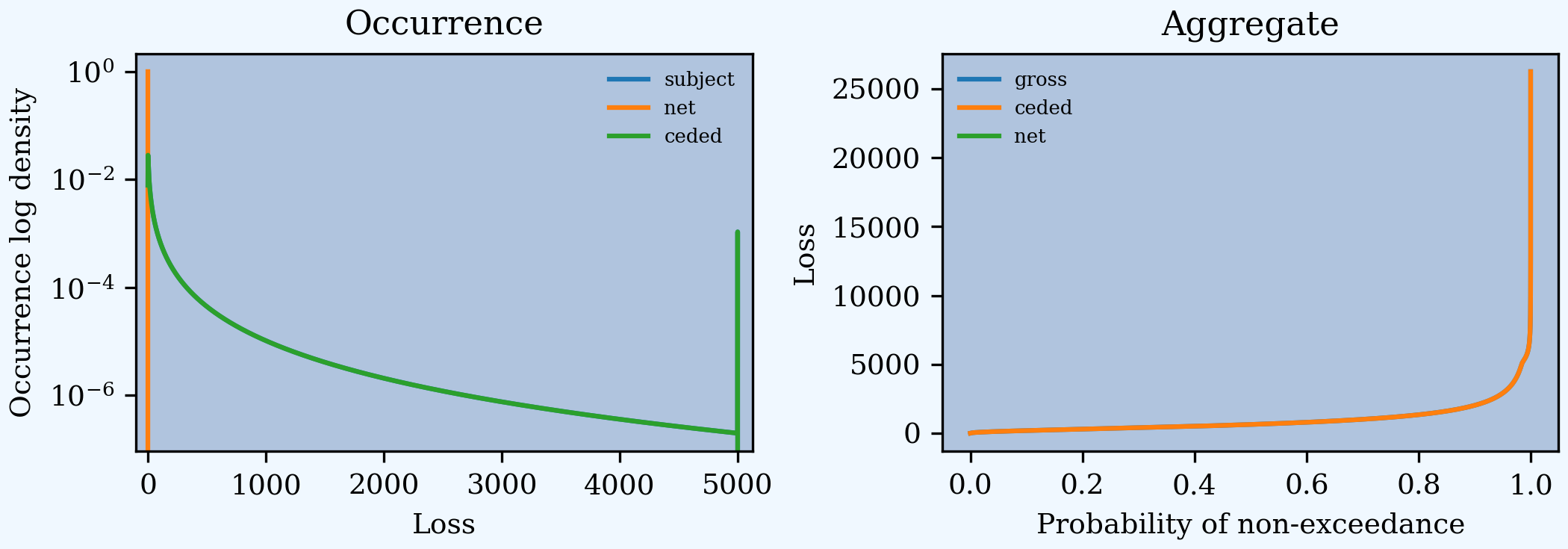

'plot shows the impact of occurrence reinsurance on severity and aggregate losses, and the ceded severity and aggregate.

In [35]: a.reinsurance_occ_plot()

The reinsurance_audit_df dataframe shows unconditional layer severity that “adds-up” to the total layer severity; compare to the total with the severity statistics in description above. These only match when the reinsurance layers exhaust the ground-up limit.

In [36]: qd(a.reinsurance_audit_df, sparsify=False)

ceded ceded ceded ceded ceded net net net net \

ex var sd cv skew ex var sd cv

kind share limit attach

occ 1.0 250.0 0.0 54.459 5603.2 74.854 1.3745 1.6845 40.599 72833 269.88 6.6474

occ 1.0 250.0 250.0 13.305 2720.7 52.16 3.9204 3.9945 81.753 73469 271.05 3.3155

occ 1.0 500.0 500.0 11.481 4748.2 68.907 6.0018 6.3905 83.576 64191 253.36 3.0315

occ 1.0 1000.0 1000.0 8.7092 7140.4 84.501 9.7025 10.609 86.348 57052 238.86 2.7662

occ 1.0 3000.0 2000.0 7.1035 15770 125.58 17.678 20.596 87.954 51379 226.67 2.5771

occ all inf gup 95.057 94314 307.11 3.2307 9.4329 0 0 0 NaN

agg 1.0 250.0 750.0 89.854 13133 114.6 1.2754 0.58829 860.72 8.8125e+05 938.75 1.0907

agg 1.0 1500.0 1000.0 220.35 2.004e+05 447.67 2.0316 2.0217 730.22 4.2122e+05 649.02 0.88879

agg all inf gup 310.2 2.8411e+05 533.02 1.7183 1.7399 640.37 3.3956e+05 582.72 0.90997

net subject subject subject subject subject

skew ex var sd cv skew

kind share limit attach

occ 1.0 250.0 0.0 11.537 95.057 94314 307.11 3.2307 9.4329

occ 1.0 250.0 250.0 10.96 95.057 94314 307.11 3.2307 9.4329

occ 1.0 500.0 500.0 10.74 95.057 94314 307.11 3.2307 9.4329

occ 1.0 1000.0 1000.0 8.7905 95.057 94314 307.11 3.2307 9.4329

occ 1.0 3000.0 2000.0 5.6194 95.057 94314 307.11 3.2307 9.4329

occ all inf gup NaN 95.057 94314 307.11 3.2307 9.4329

agg 1.0 250.0 750.0 3.242 950.57 1.0335e+06 1016.6 1.0695 2.8646

agg 1.0 1500.0 1000.0 3.9477 950.57 1.0335e+06 1016.6 1.0695 2.8646

agg all inf gup 4.8085 950.57 1.0335e+06 1016.6 1.0695 2.8646

The reinsurance_occ_layer_df dataframe shows unconditional aggregate statistics. The blocks ex and cv show values from audit_df times expected claim counts; en shows claim counts by layer. severity shows the implied conditional layer severity, equal to expected loss from audit_df divided by the probability of attaching the layer.

In [37]: qd(a.reinsurance_occ_layer_df, sparsify=False)

stat ex ex ex cv cv cv en severity pct

view ceded net subject ceded net subject ceded ceded ceded

share limit attach

1.0 250.0 0.0 544.59 405.99 950.57 1.3745 6.6474 3.2307 10 54.459 0.5729

1.0 250.0 250.0 133.05 817.53 950.57 3.9204 3.3155 3.2307 0.79248 167.89 0.13997

1.0 500.0 500.0 114.81 835.76 950.57 6.0018 3.0315 3.2307 0.36394 315.47 0.12078

1.0 1000.0 1000.0 87.092 863.48 950.57 9.7025 2.7662 3.2307 0.14697 592.59 0.09162

1.0 3000.0 2000.0 71.035 879.54 950.57 17.678 2.5771 3.2307 0.052009 1365.8 0.074729

all inf gup 950.57 0 950.57 3.2307 NaN 3.2307 10 95.057 1

The reinsurance_df density dataframe shows subject, ceded, and net occurrence (severity); aggregates created from each (without aggregate reinsurance); and subject, ceded, and net of requested aggregate reinsurance.

In [38]: qd(a.reinsurance_df, max_rows=20)

loss p_sev_gross p_sev_ceded p_sev_net p_agg_gross_occ p_agg_ceded_occ \

loss

0.0 0 0.0078283 0.0078283 1 4.9097e-05 4.9097e-05

0.5 0.5 0.027461 0.027461 0 1.3482e-05 1.3482e-05

1.0 1 0.028318 0.028318 0 1.5754e-05 1.5754e-05

1.5 1.5 0.026716 0.026716 0 1.7104e-05 1.7104e-05

2.0 2 0.024836 0.024836 0 1.83e-05 1.83e-05

2.5 2.5 0.023058 0.023058 0 1.9467e-05 1.9467e-05

3.0 3 0.021453 0.021453 0 2.0635e-05 2.0635e-05

3.5 3.5 0.020023 0.020023 0 2.1812e-05 2.1812e-05

4.0 4 0.01875 0.01875 0 2.3e-05 2.3e-05

4.5 4.5 0.017615 0.017615 0 2.42e-05 2.42e-05

... ... ... ... ... ... ...

32763.0 32763 0 0 0 0 0

32763.5 32764 0 0 0 0 0

32764.0 32764 0 0 0 0 0

32764.5 32764 0 0 0 0 0

32765.0 32765 0 0 0 0 0

32765.5 32766 0 0 0 0 0

32766.0 32766 0 0 0 0 0

32766.5 32766 0 0 0 0 0

32767.0 32767 0 0 0 0 0

32767.5 32768 0 0 0 0 0

p_agg_net_occ p_agg_gross p_agg_ceded p_agg_net

loss

0.0 1 4.9097e-05 0.57612 4.9097e-05

0.5 0 1.3482e-05 0.00029446 1.3482e-05

1.0 0 1.5754e-05 0.00029422 1.5754e-05

1.5 0 1.7104e-05 0.00029398 1.7104e-05

2.0 0 1.83e-05 0.00029374 1.83e-05

2.5 0 1.9467e-05 0.00029351 1.9467e-05

3.0 0 2.0635e-05 0.00029327 2.0635e-05

3.5 0 2.1812e-05 0.00029303 2.1812e-05

4.0 0 2.3e-05 0.00029279 2.3e-05

4.5 0 2.42e-05 0.00029256 2.42e-05

... ... ... ... ...

32763.0 0 4.5631e-19 0 0

32763.5 0 4.471e-19 0 0

32764.0 0 4.6061e-19 0 0

32764.5 0 4.5894e-19 0 0

32765.0 0 4.3986e-19 0 0

32765.5 0 4.4694e-19 0 0

32766.0 0 4.4323e-19 0 0

32766.5 0 4.3824e-19 0 0

32767.0 0 4.3557e-19 0 0

32767.5 0 4.4901e-19 0 0

The reinsurance_report_df shows statistics for the densities in reinsurance_df. The p_agg_gross column matches the theoretical (gross) output shown in qd(a) at the top and the p_agg_ceded column matches the estimated output because the aggregate program requested ceded to output. The net column is the difference.

In [39]: qd(a.reinsurance_report_df)

p_sev_gross p_sev_ceded p_sev_net p_agg_gross_occ p_agg_ceded_occ p_agg_net_occ \

mean 95.057 95.057 0 950.57 950.57 0

cv 3.2307 3.2307 NaN 1.0695 1.0695 NaN

sd 307.11 307.11 NaN 1016.6 1016.6 NaN

skew 9.4329 9.4329 NaN 2.8646 2.8646 NaN

p_agg_gross p_agg_ceded p_agg_net

mean 950.57 310.2 640.37

cv 1.0695 1.7183 0.90997

sd 1016.6 533.02 582.72

skew 2.8646 1.7399 4.8085

2.6.5. Casualty Exposure Rating

This example calculates the loss pick for excess layers across a subject portfolio with different underlying limits and deductibles but a common severity curve. The limit profile is given by a premium distribution and the expected loss ratio varies by limit. Values are in 000s. Policies at 1M and 2M limits are ground-up and those at 5M and 10M limits have a 100K and 250K deductible. The full assumptions are:

In [40]: profile = pd.DataFrame({'limit': [1000, 2000, 5000, 10000],

....: 'ded' : [0, 0, 100, 250],

....: 'premium': [10000, 5000, 2500, 1500],

....: 'lr': [.75, .75, .7, .65]

....: }, index=pd.Index(range(4), name='class'))

....:

In [41]: qd(profile)

limit ded premium lr

class

0 1000 0 10000 0.75

1 2000 0 5000 0.75

2 5000 100 2500 0.7

3 10000 250 1500 0.65

The severity is a lognormal with an unlimited mean of 50 and cv of 10, \(\sigma=2.148\).

The gross portfolio and tower are created in a07.

A typical XOL tower up to 10M is created by specifying the layer break points in an occurrence ceded to tower clause.

In [42]: a07 = build('agg Re:07 '

....: f'{profile.premium.values} premium at {profile.lr.values} lr '

....: f'{profile.limit.values} xs {profile.ded.values} '

....: 'sev lognorm 50 cv 10 '

....: 'occurrence ceded to tower [0 250 500 1000 2000 5000 10000] '

....: 'poisson '

....: , approximation='exact', log2=18, bs=1/2)

....:

In [43]: qd(a07)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 292.72 0.058448 0.058448

Sev 47.741 47.737 -8.6055e-05 4.0096 4.01 15.901 15.901

Agg 13975 13974 -8.6055e-05 0.24153 0.24156 0.88974 0.88974

log2 = 18, bandwidth = 1/2, validation: n/a, reinsurance.

There are special options in build because the claim count is high: 292.7. To force a convolution use approximation='exact'. Reviewing the default bs=1/2 and log2=16 shows a moderate error. Looking at the density via:

a07.density_df.p_total.plot(logy=True)

shows aliasing, i.e., there is not enough space in the answer. Adjust by increasing log2 from 16 to 18 and leaving bs=1/2.

The dataframe reinsurance_occ_layer_df shows layer expected loss, CV, counts, and conditional severity. The last column shows the percent of subject ceded to each layer.

In [44]: qd(a07.reinsurance_occ_layer_df, sparsify=False)

stat ex ex ex cv cv cv en severity pct

view ceded net subject ceded net subject ceded ceded ceded

share limit attach

1.0 250.0 0.0 8724.1 5249.7 13974 1.9905 8.8564 4.01 292.72 29.803 0.62432

1.0 250.0 250.0 2076.6 11897 13974 5.4793 4.0236 4.01 12.063 172.15 0.14861

1.0 500.0 500.0 1917.9 12056 13974 8.0564 3.7267 4.01 5.8545 327.58 0.13725

1.0 1000.0 1000.0 775.37 13198 13974 17.887 3.5805 4.01 1.2306 630.1 0.055488

1.0 3000.0 2000.0 400.74 13573 13974 41.327 3.509 4.01 0.26392 1518.4 0.028678

1.0 5000.0 5000.0 79.06 13895 13974 122.64 3.8196 4.01 0.027983 2825.3 0.0056577

all inf gup 13974 -7.8694e-09 13974 4.01 NaN 4.01 292.72 47.737 1

2.6.6. Property Risk Exposure Rating

Property risk exposure rating differs from casualty in part because the severity distribution varies with each risk (location). Rather than a single ground-up severity curve per class, there is a size of loss distribution normalized by property total insured value (TIV).

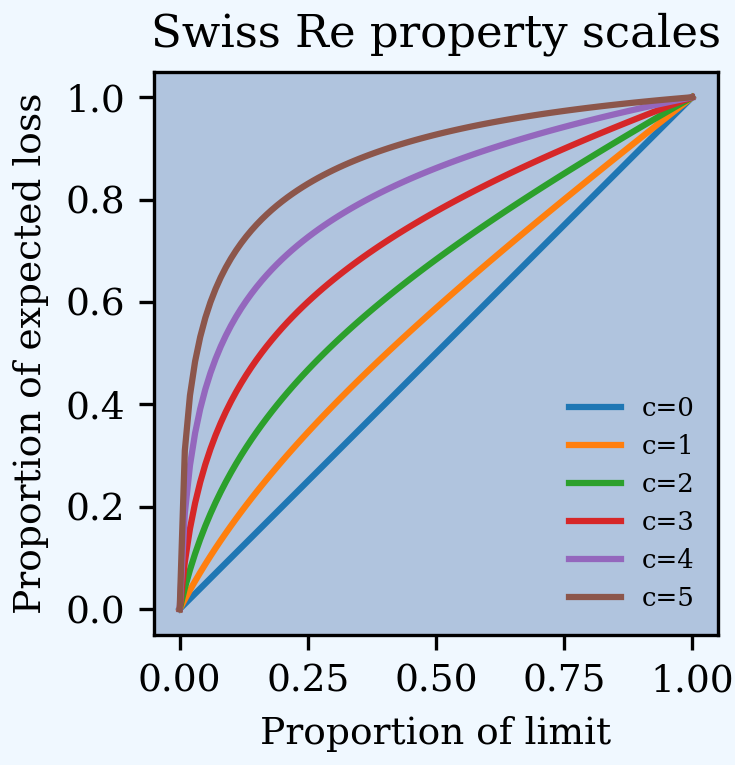

We start by introducing the Swiss Re severity curves, Bernegger [1997] using a moments-matched beta distribution. The function G defines the MBBEFD distribution, parameterized by c.

In [45]: from aggregate import xsden_to_meancv

In [46]: import scipy.stats as ss

In [47]: import numpy as np

In [48]: import matplotlib.pyplot as plt

In [49]: def bb(c):

....: return np.exp(3.1 - 0.15*c*(1+c))

....:

In [50]: def bg(c):

....: return np.exp((0.78 + 0.12*c)*c)

....:

In [51]: def G(x, c):

....: b = bb(c)

....: g = bg(c)

....: return np.log(((g - 1) * b + (1 - g * b) * b**x) / (1 - b)) / np.log(g * b)

....:

Here are the base curves, compare Figure 4.2 in Bernegger [1997]. The curve c=5 is close to the Lloyd’s curve (scale).

In [52]: fig, ax = plt.subplots(1, 1, figsize=(2.45, 2.55), constrained_layout=True)

In [53]: ans = []

In [54]: ps = np.linspace(0,1,101)

In [55]: for c in [0, 1, 2, 3, 4, 5]:

....: gs = G(ps, c)

....: ax.plot(ps, gs, label=f'c={c}')

....: ans.append([c, *xsden_to_meancv(ps[1:], np.diff(gs))])

....:

In [56]: ax.legend(loc='lower right');

In [57]: ax.set(xlabel='Proportion of limit', ylabel='Proportion of expected loss',

....: title='Swiss Re property scales');

....:

Next, approximate these curves with a beta distribution to make them easier for us to use in aggregate. Here are the parameters and fit graphs for each curve.

In [58]: swiss = pd.DataFrame(ans, columns=['c', 'mean', 'cv'])

In [59]: def beta_ab(m, cv):

....: v = (m * cv) ** 2

....: sev_a = m * (m * (1 - m) / v - 1)

....: sev_b = (1 - m) * (m * (1 - m) / v - 1)

....: return sev_a, sev_b

....:

In [60]: a, b = beta_ab(swiss['mean'], swiss.cv)

In [61]: swiss['a'] = a

In [62]: swiss['b'] = b

In [63]: swiss = swiss.set_index('c')

In [64]: qd(swiss)

mean cv a b

c

0 0.505 0.57161 1.01 0.99

1 0.44108 0.67278 0.79375 1.0058

2 0.36415 0.81654 0.58953 1.0294

3 0.28003 1.0103 0.42538 1.0937

4 0.19858 1.2531 0.31176 1.2582

5 0.13101 1.5171 0.24654 1.6353

In [65]: fig, axs = plt.subplots(2, 3, figsize=(3 * 2.45, 2 * 2.45), constrained_layout=True)

In [66]: for ax, (c, r) in zip(axs.flat, swiss.iterrows()):

....: gs = G(ps, c)

....: fz = ss.beta(r.a, r.b)

....: ax.plot(ps, gs, label=f'c={c}')

....: ax.plot(ps, fz.cdf(ps), label=f'beta fit')

....: ans.append([c, *xsden_to_meancv(ps[1:], np.diff(gs))])

....: ax.legend(loc='lower right');

....:

In [67]: fig.suptitle('Beta approximations to Swiss Re property curves');

Work on a property schedule with the following TIVs and deductibles. The premium rate is 0.35 per 100 and the loss ratio is 55%.

In [68]: schedule = pd.DataFrame({

....: 'locid': range(10),

....: 'tiv': [850, 950, 1250, 1500, 4500, 8000, 9000, 12000, 25000, 50000],

....: 'ded': [ 10, 10, 20, 20, 50, 100, 500, 1000, 5000, 5000]}

....: ).set_index('locid')

....:

In [69]: schedule['premium'] = schedule.tiv / 100 * 0.35

In [70]: schedule['lr'] = 0.55

In [71]: qd(schedule)

tiv ded premium lr

locid

0 850 10 2.975 0.55

1 950 10 3.325 0.55

2 1250 20 4.375 0.55

3 1500 20 5.25 0.55

4 4500 50 15.75 0.55

5 8000 100 28 0.55

6 9000 500 31.5 0.55

7 12000 1000 42 0.55

8 25000 5000 87.5 0.55

9 50000 5000 175 0.55

Build the stochastic model using a Swiss Re c=3 scale. Use a gamma mixed Poisson frequency with a CV of 3 to reflect the potential for catastrophe losses. Use a tower clause to set up the analysis of a per risk tower. Increase bs to 2 based on high error with recommended bs=1.

In [72]: beta_a, beta_b = swiss.loc[3, ['a', 'b']]

In [73]: a08 = build('agg Re:08 '

....: f'{schedule.premium.values} premium at {schedule.lr.values} lr '

....: f'{schedule.tiv.values} xs {schedule.ded.values} '

....: f'sev {schedule.tiv.values} * beta {beta_a} {beta_b} ! '

....: 'occurrence ceded to tower [0 1000 5000 10000 20000 inf] '

....: 'mixed gamma 2 '

....: , bs=2)

....:

In [74]: qd(a08)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.081693 4.03 5.0226

Sev 2663.9 2663.9 -1.2094e-07 2.2311 2.2311 3.8455 3.8455

Agg 217.62 217.62 -1.3778e-07 8.7849 8.7849 14.303 14.303

log2 = 16, bandwidth = 2, validation: n/a, reinsurance.

The shared mixing increases the frequency and aggregate CV and skewness.

In [75]: qd(a08.report_df.loc[

....: ['freq_m', 'freq_cv', 'freq_skew', 'agg_cv', 'agg_skew'],

....: ['independent', 'mixed']])

....:

view independent mixed

statistic

freq_m 0.081693 0.081693

freq_cv 3.5576 4.03

freq_skew 3.6749 5.0226

agg_cv 8.6169 8.7849

agg_skew 14.248 14.303

Look at reinsurance_occ_layer_df to summarize the analysis.

In [76]: qd(a08.reinsurance_occ_layer_df, sparsify=False)

stat ex ex ex cv cv cv en severity pct

view ceded net subject ceded net subject ceded ceded ceded

share limit attach

1.0 1000.0 0.0 38.473 179.15 217.62 0.93539 2.612 2.2311 0.05879 654.41 0.17679

1.0 4000.0 1000.0 74.293 143.33 217.62 1.6859 2.7968 2.2311 0.027946 2658.4 0.34139

1.0 5000.0 5000.0 43.156 174.47 217.62 2.6872 2.2324 2.2311 0.012623 3418.8 0.19831

1.0 10000.0 10000.0 37.782 179.84 217.62 4.1476 1.9578 2.2311 0.0059027 6400.9 0.17362

1.0 inf 20000.0 23.917 193.7 217.62 7.2389 1.91 2.2311 0.0021465 11143 0.1099

all inf gup 217.62 0 217.62 2.2311 NaN 2.2311 0.081693 2663.9 1

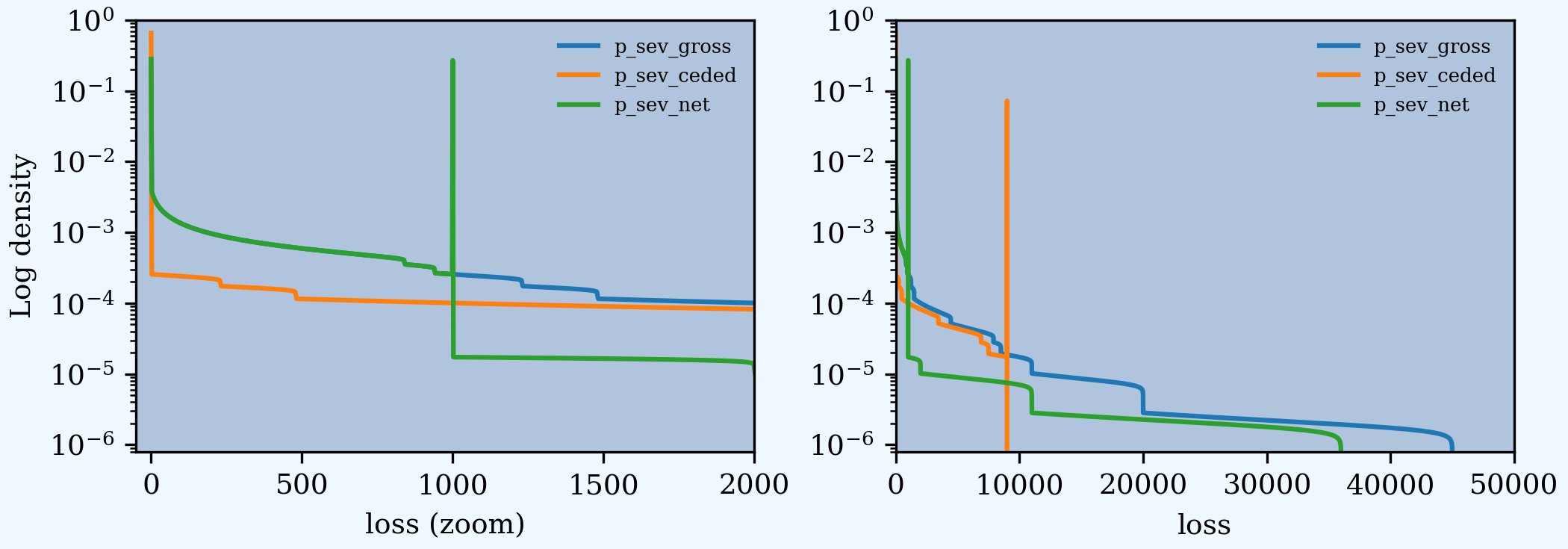

Add plots of gross, ceded, and net severity with the placed program, 4000 xs 1000 and 5000 xs 5000. (The net is zero with the tower clause, so we have to recompute.) The left and right plots differ only in the x-axis scale.

In [77]: a09 = build('agg Re:09 '

....: f'{schedule.premium.values} premium at {schedule.lr.values} lr '

....: f'{schedule.tiv.values} xs {schedule.ded.values} '

....: f'sev {schedule.tiv.values} * beta {beta_a} {beta_b} ! '

....: 'occurrence ceded to 4000 xs 1000 and 5000 xs 5000 '

....: 'mixed gamma 2 ', bs=2)

....:

In [78]: qd(a09)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.081693 4.03 5.0226

Sev 2663.9 1437.7 -0.46031 2.2311 1.9215 3.8455 1.8785

Agg 217.62 117.45 -0.46031 8.7849 7.838 14.303 9.4024

log2 = 16, bandwidth = 2, validation: n/a, reinsurance.

In [79]: fig, axs = plt.subplots(1, 2, figsize=(2 * 3.5, 2.45), constrained_layout=True); \

....: ax0, ax1 = axs.flat; \

....: df = a09.reinsurance_df; \

....: df.filter(regex='sev_[gcn]').plot(logy=True, xlim=[-50, 2000], ylim=[0.8e-6, 1] , ax=ax0); \

....: df.filter(regex='sev_[gcn]').plot(logy=True, xlim=[0, 50000], ylim=[0.8e-6, 1], ax=ax1); \

....: ax0.set(xlabel='loss (zoom)', ylabel='Log density');

....:

In [80]: ax1.set(xlabel='loss', ylabel='');

And finally, plot the corresponding aggregate distributions.

In [81]: fig, axs = plt.subplots(2, 2, figsize=(2 * 3.5, 2 * 2.45), constrained_layout=True); \

....: ax0, ax1, ax2, ax3 = axs.flat; \

....: df.filter(regex='agg_.*_occ').plot(logy=True, xlim=[-50, 2000], ylim=[0.8e-6, 1] , ax=ax0); \

....: (1 - df.filter(regex='agg_.*_occ').cumsum()).plot(logy=True, xlim=[-50, 2000], ylim=[1e-3, 1], ax=ax2); \

....: df.filter(regex='agg_.*_occ').plot(logy=True, xlim=[0, 50000], ylim=[0.8e-12, 1], ax=ax1); \

....: (1 - df.filter(regex='agg_.*_occ').cumsum()).plot(logy=True, xlim=[0, 50000], ylim=[1e-9, 1], ax=ax3); \

....: ax0.set(xlabel='', ylabel='Log density'); \

....: ax1.set(xlabel='', ylabel=''); \

....: ax2.set(xlabel='loss (zoom)', ylabel='Log survival');

....:

In [82]: ax3.set(xlabel='loss', ylabel='');

2.6.7. Variable Features

Reinsurance treaties can incorporate variable features that alter the contract cash flows. These can impact losses, premiums, or expenses (through the ceding commission). They can apply to quota share and excess treaties.

Variable features altering Loss cash flows

Aggregate limits and deductibles

Loss corridor

Limited reinstatements for excess treaties, by number of covered events or an aggregate limit

Variable features altering Premium cash flows

Swing or retro rating or margin-plus premium, where the premium equals losses times an expense factor subject to a maximum and minimum. See also Individual Risk Pricing.

Variable features altering Expense cash flows

Sliding scale commission

Profit commission or profit share

A loss corridor and sliding scale commission have a similar impact; both concentrate the impact of the treaty on tail outcomes. Aggregate features have the opposite effect; concentrating the impact on body outcomes and lowering effectiveness on tail outcomes.

Premium and expense related features are substitutes, the former used on treaties without ceding commissions.

2.6.8. Inwards Analysis of Bear and Nemlick Variable Features

Bear and Nemlick [1990] analyze six treaties with variable features across four portfolios.

These examples are included because they are realistic and show that aggregate produces the same answers as a published reference.

The subject losses defined as follows.

Treaty 1 and 4.

Cover: 160 xs 40

Subject business

Two classes

Subject premium 3000 and 6000

Loss rate 4% and 3%

Severity: single parameter Pareto with shape 0.9 and 0.95

Treaty 2 and 5.

Cover: 700 xs 300

Subject business

Three classes

Subject premium 2000 each

Loss rate 10%, 14%, 21%

Severity: single parameter Pareto with shape 1.5, 1.3, 1.1

Treaty 3.

Cover: 400 xs 100

Subject business

Three classes

Subject premium 4500, 4500, 1000

Loss rate 3.2%, 3.8%, 3.5%

Severity: single parameter Pareto with shape 1.1.

Treaty 6.

Cover: 900 xs 100

Subject business

Subject premium 25000

Layer loss cost 10% of subject premium

Portfolio CV 0.485

They include a variety of frequency assumptions, including Poisson, negative binomial with variance multiplier based on a gross multiplier of 2 or 3 adjusted for excess frequency, mixing variance 0.05 and 0.10. Excess counts get closer to Poisson and so the difference between the two is slight.

The next table shows Bear and Nemlick’s estimated premium rates.

Bear and Nemlick’s estimated premium rates by program by numerical method. The Lognormal Model column uses a method of moments fit to the aggregate mean and CV. The Collective Risk Model columns uses the Heckman-Meyers continuous FFT method.

Heckman and Meyers describe claim count contagion and frequency parameter uncertainty, which they model using a mixed-Poisson frequency distribution. Their parameter \(c\) is the variance of the mixing distribution. The value c=0.05 is replicated in DecL with the frequency clause mixed gamma 0.05**0.5, since DecL is based on the CV of the mixing distribution (the mean is always 1).

Heckman and Meyers also describe severity parameter uncertainty, which they model with an inverse gamma variable with mean 1 and variance \(b\). There is no analog of severity uncertainty in DecL. For finite excess layers it has a muted impact on results. Heckman and Meyers call \(c\) the contagion parameter and \(b\) the mixing parameter, which is confusing in our context. To approximate these columns use

c=0,b=0corresponds to the DecL frequency clausepoisson.c=0.05,b=...is close to DecL frequency clausemixed gamma 0.05**0.5.c=0.1,b=...is close to DecL frequency clausemixed gamma 0.1**0.5.

2.6.8.1. Specifying the Single Parameter Pareto

Losses to an excess layer specified by a single parameter Pareto are the same as losses to a ground-up layer with a shifted Pareto.

Example.

For 400 xs 100 and Pareto shape 1.1, these two DecL programs produce identical results:

4 claims 400 xs 100 sev 100 * pareto 1.1 poisson

4 claims 400 xs 0 sev 100 * pareto 1.1 - 100 poisson

2.6.8.2. Treaty 1: Aggregate Deductible

Treaty 1 adds an aggregate deductible of 360, equal to 3% of subject premium.

Setup the gross portfolio.

In [83]: import numpy as np

In [84]: from aggregate import build, mv, qd, xsden_to_meancvskew, \

....: mu_sigma_from_mean_cv, lognorm_lev

....:

In [85]: mix_cv = ((1.036-1)/5.154)**.5; mix_cv

Out[85]: 0.08357551150546018

In [86]: a10 = build('agg Re:BN1 '

....: '[9000 3000] exposure at [0.04 0.03] rate '

....: '160 xs 0 '

....: 'sev 40 * pareto [0.9 0.95] - 40 '

....: f'mixed gamma {mix_cv} ')

....:

In [87]: qd(a10)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 6.4966 0.40114 0.41855

Sev 69.267 69.267 -1.2751e-08 0.87703 0.87703 0.50056 0.50056

Agg 450 450 -2.1418e-07 0.5285 0.5285 0.62441 0.62436

log2 = 16, bandwidth = 1/32, validation: fails agg mean error >> sev, possible aliasing; try larger bs.

The portfolio CV matches 0.528, reported in Bear and Nemlick Appendix F, Exhibit 1.

There are several ways to estimate the impact of the AAD on recovered losses.

By hand, adjust losses and use the distribution of outcomes from a.density_df. The last line computes the sum-product of losses net of AAD times probabilities, i.e., the expected loss cost.

In [88]: bit = a10.density_df[['loss', 'p_total']]

In [89]: bit['loss'] = np.maximum(0, bit.loss - 360)

In [90]: bit.prod(axis=1).sum()

Out[90]: np.float64(142.75712297665373)

More in the spirit of aggregate: create a new Aggregate applying the AAD using a DecL aggregate net of reinsurance clause. Alternatively use aggregate ceded to inf xs 360 (not shown).

In [91]: a11 = build('agg Re:BN1a '

....: '[9000 3000] exposure at [0.04 0.03] rate '

....: '160 xs 0 '

....: 'sev 40 * pareto [0.9 0.95] - 40 '

....: f'mixed gamma {mix_cv} '

....: 'aggregate net of 360 xs 0 ')

....:

In [92]: qd(a11)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 6.4966 0.40114 0.41855

Sev 69.267 69.267 -1.2751e-08 0.87703 0.87703 0.50056 0.50056

Agg 450 142.76 -0.68276 0.5285 1.2873 0.62441 1.5337

log2 = 16, bandwidth = 1/32, validation: n/a, reinsurance.

In [93]: gross = a11.agg_m; net = a11.est_m; ins_charge = net / gross

In [94]: net, ins_charge

Out[94]: (np.float64(142.75888602897442), np.float64(0.31724196895327644))

Bear and Nemlick use a lognormal approximation to the aggregate.

In [95]: mu, sigma = mu_sigma_from_mean_cv(a10.agg_m, a10.agg_cv)

In [96]: elim_approx = lognorm_lev(mu, sigma, 1, 360)

In [97]: a11.agg_m - elim_approx, 1 - elim_approx / a11.agg_m

Out[97]: (np.float64(132.0633321885802), np.float64(0.29347407153017824))

The lognormal overstates the value of the AAD, resulting in a lower net premium. This is because the approximating lognormal is much more skewed.

In [98]: fz = a11.approximate('lognorm')

In [99]: fz.stats('s'), a11.est_skew

Out[99]: (np.float64(5.995433538387627), np.float64(1.5337492513582904))

Bear and Nemlick report the Poisson approximation and a Heckman-Meyers convolution with mixing and contagion equal 0.05. We can compute the Poisson exactly and approximate Heckman-Meyers with contagion but no mixing. Changing 0.05 to 0.10 is close to the b=0.1 column.

In [100]: a12 = build('agg Re:BN1p '

.....: '[9000 3000] exposure at [0.04 0.03] rate '

.....: '160 xs 0 '

.....: 'sev 40 * pareto [0.9 0.95] - 40 '

.....: f'poisson '

.....: 'aggregate net of 360 xs 0 ')

.....:

In [101]: qd(a12)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 6.4966 0.39234 0.39234

Sev 69.267 69.267 -1.2751e-08 0.87703 0.87703 0.50056 0.50056

Agg 450 141.8 -0.68489 0.52185 1.2794 0.60775 1.5152

log2 = 16, bandwidth = 1/32, validation: n/a, reinsurance.

In [102]: a13 = build('agg Re:BN1c '

.....: '[9000 3000] exposure at [0.04 0.03] rate '

.....: '160 xs 0 '

.....: 'sev 40 * pareto [0.9 0.95] - 40 '

.....: 'mixed gamma 0.05**.5 '

.....: 'aggregate net of 360 xs 0 ')

.....:

In [103]: qd(a13)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 6.4966 0.45158 0.5623

Sev 69.267 69.267 -5.1006e-08 0.87703 0.87703 0.50056 0.50056

Agg 450 148.41 -0.6702 0.56774 1.3332 0.72251 1.6412

log2 = 16, bandwidth = 1/16, validation: n/a, reinsurance.

Here is a summary of the different methods, compare Bear and Nemlick Table 1, row 1, page 75.

In [104]: bit = pd.DataFrame([a10.agg_m,

.....: a11.describe.iloc[-1, 1],

.....: a12.describe.iloc[-1, 1],

.....: a13.describe.iloc[-1, 1],

.....: a11.agg_m - elim_approx],

.....: columns=['Loss cost'],

.....: index=pd.Index(['Gross', 'NB', 'Poisson', 'c=0.05', 'lognorm'],

.....: name='Method'))

.....:

In [105]: bit['Premium'] = bit['Loss cost'] * 100 / 75

In [106]: bit['Rate'] = bit.Premium / 12000

In [107]: qd(bit, accuracy=5)

Loss cost Premium Rate

Method

Gross 450 600 0.05

NB 142.76 190.35 0.015862

Poisson 141.8 189.07 0.015755

c=0.05 148.41 197.88 0.01649

lognorm 132.06 176.08 0.014674

2.6.8.3. Treaty 2: Aggregate Limit

Treaty 2 adds an aggregate limit of 2800, i.e., 3 full reinstatements plus the original limit.

Setup the gross portfolio.

In [108]: a14 = build('agg Re:BN2 '

.....: '[2000 2000 2000] exposure at [.1 .14 .21] rate '

.....: '700 xs 0 '

.....: 'sev 300 * pareto [1.5 1.3 1.1] - 300 '

.....: 'mixed gamma 0.07 '

.....: , bs=1/8)

.....:

In [109]: qd(a14)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2.8949 0.5919 0.60017

Sev 310.9 310.9 -8.2604e-09 0.83714 0.83714 0.46335 0.46335

Agg 900 900 -8.4265e-09 0.76969 0.76969 0.90207 0.90207

log2 = 16, bandwidth = 1/8, validation: not unreasonable.

Specify bs=1/8 since the error was too high with the default bs=1/16.

The portfolio CV matches 0.770, reported in Bear and Nemlick Appendix G, Exhibit 1. The easiest way to value the aggregate limit to use an aggregate ceded to clause.

In [110]: a14n = build('agg Re:BN2a '

.....: '[2000 2000 2000] exposure at [.1 .14 .21] rate '

.....: '700 xs 0 '

.....: 'sev 300 * pareto [1.5 1.3 1.1] - 300 '

.....: 'mixed gamma 0.07 '

.....: 'aggregate ceded to 2800 xs 0'

.....: , bs=1/8)

.....:

In [111]: qd(a14n)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2.8949 0.5919 0.60017

Sev 310.9 310.9 -8.2604e-09 0.83714 0.83714 0.46335 0.46335

Agg 900 894.68 -0.0059104 0.76969 0.7544 0.90207 0.72143

log2 = 16, bandwidth = 1/8, validation: n/a, reinsurance.

Applying a 20% coinsurance and grossing up by 100/60 produces the premium and rate. Using Poisson frequency, or mixed gamma with mix \(\sqrt{0.05}\) or \(\sqrt{0.1}\) ties closely to Table I, row 2.

In [112]: p = a14n.est_m * (1 - 0.2) * 100 / 60

In [113]: p, p / 6000

Out[113]: (np.float64(1192.907570662762), np.float64(0.19881792844379367))

aggregate induces correlation between the three classes because they share mixing variables. The report_df shows the details by line and compares with an independent sum.

In [114]: qd(a14.report_df.iloc[:, :-2])

view 0 1 2 independent mixed

statistic

name Re:BN2 Re:BN2 Re:BN2 Re:BN2 Re:BN2

limit 700 700 700 700 700

attachment 0 0 0 0 0

el 200 280 420 900 900

freq_m 0.73701 0.92362 1.2342 2.8949 2.8949

freq_cv 1.1669 1.0429 0.90284 0.58919 0.5919

freq_skew 1.1711 1.0476 0.90827 0.59209 0.60017

sev_m 271.37 303.15 340.3 310.9 310.9

sev_cv 0.9087 0.84973 0.78339 0.83714 0.83714

sev_skew 0.72529 0.51332 0.27989 0.46335 0.46335

agg_m 200 280 420 900 900

agg_cv 1.5755 1.3672 1.1456 0.76767 0.76969

agg_skew 1.9025 1.6073 1.3121 0.89708 0.90207

2.6.8.4. Treaty 3: Loss Corridor

Treaty 3 is a loss corridor from expected layer losses to twice expected. The reinsurance pays up to expected and beyond twice expected.

Setup the gross portfolio with CV 0.905. Use a larger bs to reduce error.

In [115]: a15 = build('agg Re:BN3 '

.....: '[4500 4500 1000] exposure at [.032 .038 .035] rate '

.....: '400 xs 0 '

.....: 'sev 100 * pareto 1.1 - 100 '

.....: 'poisson', bs=1/16)

.....:

In [116]: qd(a15)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2.3544 0.65172 0.65172

Sev 148.66 148.66 -1.1633e-08 0.96405 0.96405 0.79141 0.79141

Agg 350 350 -1.1694e-08 0.90526 0.90526 1.0937 1.0937

log2 = 16, bandwidth = 1/16, validation: not unreasonable.

There are several ways to model a loss corridor, but the most natural is to use an aggregate net of 350 xs 350 clause; expected layer loss equals 350.

In [117]: a15_lc = build('agg Re:BN3lc '

.....: '[4500 4500 1000] exposure at [.032 .038 .035] rate '

.....: '400 xs 0 '

.....: 'sev 100 * pareto 1.1 - 100 '

.....: 'poisson '

.....: 'aggregate net of 350 xs 350 ', bs=1/16)

.....:

In [118]: qd(a15_lc)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2.3544 0.65172 0.65172

Sev 148.66 148.66 -1.1633e-08 0.96405 0.96405 0.79141 0.79141

Agg 350 256.88 -0.26607 0.90526 0.79669 1.0937 1.2854

log2 = 16, bandwidth = 1/16, validation: n/a, reinsurance.

Compare the results with the lognormal approximation, see Table 1 line 3.

In [119]: mu, sigma = mu_sigma_from_mean_cv(1, 0.905)

In [120]: ler = lognorm_lev(mu, sigma, 1, 2) - lognorm_lev(mu, sigma, 1, 1)

In [121]: p = a15_lc.est_m * 100 / 70

In [122]: bit = pd.DataFrame(

.....: [a15_lc.est_m, 1 - a15_lc.est_m / a15.est_m, ler, p, p/10000,

.....: 350 * (1 - ler) * 100 / 70 / 10000, 350 * 100 / 70 / 10000],

.....: index=pd.Index(['Loss cost', 'LER', 'Lognorm LER', 'Premium',

.....: 'Rate', 'Lognorm rate', 'Unadjusted rate'],name='Item'),

.....: columns=['Value'])

.....:

In [123]: qd(bit, accuracy=4)

Value

Item

Loss cost 256.88

LER 0.26607

Lognorm LER 0.19535

Premium 366.97

Rate 0.036697

Lognorm rate 0.040233

Unadjusted rate 0.05

2.6.8.5. Treaty 4: Retro Rated Program

Treaty 4 is a retro rated program on the same business as Treaty 1. The flat rate is 5%, given by a 100/75 load on the 3.75% loss cost. Subject premium equals 12000. The retrospective rating plan has a one-year adjustment period. The adjusted treaty premium equals 100/75 times incurred losses and ALAE in the layer limited to a maximum of 10% of subject premium and a minimum of 3%.

The gross portfolio is the same as Treaty 1. Use Poisson frequency.

In [124]: a16 = build('agg Re:BN4 '

.....: '[9000 3000] exposure at [0.04 0.03] rate '

.....: '160 xs 0 '

.....: 'sev 40 * pareto [0.9 0.95] - 40 '

.....: 'poisson ')

.....:

In [125]: qd(a16)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 6.4966 0.39234 0.39234

Sev 69.267 69.267 -1.2751e-08 0.87703 0.87703 0.50056 0.50056

Agg 450 450 -1.3429e-07 0.52185 0.52185 0.60775 0.60771

log2 = 16, bandwidth = 1/32, validation: fails agg mean error >> sev, possible aliasing; try larger bs.

The estimated retro premium (erp) and corresponding rate are easy to compute.

In [126]: bit = a16.density_df[['loss', 'p_total']]

In [127]: subject = 12000; min_rate = 0.03; max_rate = 0.10; lcf = 100 / 75

In [128]: bit['premium'] = np.minimum(max_rate * subject,

.....: np.maximum(min_rate * subject, lcf * bit.loss))

.....:

In [129]: erp = bit[['premium', 'p_total']].prod(1).sum()

In [130]: erp, erp / subject

Out[130]: (np.float64(624.5089537546489), np.float64(0.05204241281288741))

Bear and Nemlick also report the lognormal approximation.

In [131]: from scipy.integrate import quad

In [132]: fz = a16.approximate('lognorm')

In [133]: lognorm_approx = quad(lambda x: min(max_rate * subject,

.....: max(min_rate * subject, lcf * x)) * fz.pdf(x),

.....: 0, np.inf)

.....:

In [134]: lognorm_approx[0], lognorm_approx[0] / subject

Out[134]: (602.6887696334264, 0.05022406413611887)

2.6.8.7. Treaty 6: Sliding Scale Commission

Treaty 6 models a one-year sliding scale commission plan. The details of the plan are:

Minimum commission of 20% at or above a 65% loss ratio

Slide 0.5:1 between 55% and 65% to a 25% commission

Slide 0.75:1 between 35% and 55% to a 40% commission

Maximum commission of 40% at or below a 35% loss ratio.

The underlying portfolio is specified only as a 900 xs 100 layer on 25M premium with a 10% layer loss cost and a CV of 0.485. No other details are provided. Based on trial and error and the other examples, model the portfolio using a single parameter Pareto with \(q=1.05\) and a gamma mixed Poisson with mixing CV 0.095.

In [151]: a18 = build('agg Re:BN5 '

.....: '25000 exposure at 0.1 rate '

.....: '900 xs 0 '

.....: 'sev 100 * pareto 1.05 - 100 '

.....: 'mixed gamma 0.095')

.....:

In [152]: qd(a18)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 11.494 0.30988 0.339

Sev 217.5 217.5 -1.246e-07 1.2656 1.2656 1.5532 1.5532

Agg 2500 2500 -1.246e-07 0.48516 0.48516 0.64857 0.64857

log2 = 16, bandwidth = 1/4, validation: not unreasonable.

We use the function make_ceder_netter to model the commission function. It takes a list of triples (s, y, a) as argument, interpreted as a share s of the layer y excess a. It returns two functions, a netter and a ceder, that map a subject loss to net or ceded. Multiple non-overlapping layers can be provided. They are combined into a single function. We will model the slide as the maximum 40% commission minus a cession to two layers with different shares. The required layer descriptions, in loss ratio points, are

Layer 1

(0.25, 0.2, 0.35)for the slide between 35% and 55% andLayer 2

(0.5, 0.1, 0.55)for the slide between 55% and 65%.

The function giving the slide payoff is easy to create, using a Python lambda function. The figure illustrates the ceder and netter functions and the function that computes the slide.

In [153]: from aggregate import make_ceder_netter

In [154]: import matplotlib.pyplot as plt

In [155]: from matplotlib import ticker

In [156]: c, n = make_ceder_netter([(0.25, .2, .35), (0.5, .1, .55)])

In [157]: f = lambda x: 0.4 - c(x); \

.....: lrs = np.linspace(0.2, 0.8, 61); \

.....: slide = f(lrs); \

.....: fig, axs = plt.subplots(1,3,figsize=(3*3.5, 2.45), constrained_layout=True); \

.....: ax0, ax1, ax2 = axs.flat; \

.....: ax0.plot(lrs, c(lrs)); \

.....: ax0.set(xlabel='Loss ratio', ylabel='"Ceded"'); \

.....: ax1.plot(lrs, n(lrs)); \

.....: ax1.set(xlabel='Loss ratio', ylabel='"Net"'); \

.....: ax2.plot(lrs, slide);

.....:

In [158]: for ax in axs.flat:

.....: ax.xaxis.set_major_locator(ticker.MultipleLocator(0.1))

.....: ax.xaxis.set_minor_locator(ticker.MultipleLocator(0.05))

.....: ax.xaxis.set_major_formatter(ticker.StrMethodFormatter('{x:.0%}'))

.....: ax.yaxis.set_major_formatter(ticker.StrMethodFormatter('{x:.0%}'))

.....: if ax is ax1:

.....: ax.yaxis.set_major_locator(ticker.MultipleLocator(0.1))

.....: ax.yaxis.set_minor_locator(ticker.MultipleLocator(0.05))

.....: else:

.....: ax.yaxis.set_major_locator(ticker.MultipleLocator(0.05))

.....: ax.yaxis.set_minor_locator(ticker.MultipleLocator(0.025))

.....: ax.grid(lw=.25, c='w')

.....:

In [159]: ax2.set(xlabel='Loss ratio', ylabel='Slide commission');

The expected commission across the estimated aggregate distribution can be computed by hand.

In [160]: subject = 25000; re_rate = 0.2; re_premium = subject * re_rate

In [161]: bit = a18.density_df[['loss', 'p_total']]

In [162]: bit['lr'] = bit.loss / re_premium

In [163]: bit['slide'] = f(bit.lr)

In [164]: (bit.slide * bit.p_total).sum()

Out[164]: np.float64(0.35742739117598255)

The same quantity can be estimated using a lognormal approximation and numerical integration. The second value returned by quad estimates the relative error of the answer.

In [165]: import scipy.stats as ss

In [166]: mu, sigma = mu_sigma_from_mean_cv(0.5, 0.485)

In [167]: fz = ss.lognorm(sigma, scale=np.exp(mu))

In [168]: quad(lambda x: (0.4 - c(x)) * fz.pdf(x), 0, np.inf)

Out[168]: (0.3613013481625082, 5.3330516163912675e-09)

Bear and Nemlick use a coarser lognormal approximation to estimate the slide commission, Appendix K Exhibit I.

In [169]: mu, sigma = mu_sigma_from_mean_cv(1, 0.485)

In [170]: lr = 0.5; max_slide = 0.4

In [171]: entry_ratios = [1.3, 1.1, 0.7, 0]

In [172]: ins_charge = [1 - lognorm_lev(mu, sigma, 1, i) for i in entry_ratios]

In [173]: lr_points = np.diff(np.array(ins_charge), prepend=0) * lr

In [174]: slide_scale = np.array([0, .5, .75, 0])

In [175]: red_from_max = slide_scale * lr_points

In [176]: expected_slide = max_slide - np.sum(red_from_max)

In [177]: expected_slide

Out[177]: np.float64(0.3106485062930016)

The lognormal distribution is not a great fit to the specified distribution.

In [178]: bit['logn'] = fz.pdf(bit.loss / re_premium)

In [179]: bit.logn = bit.logn / bit.logn.sum()

In [180]: fig, axs = plt.subplots(1, 2, figsize=(2 * 3.5, 2.45), constrained_layout=True)

In [181]: ax0, ax1 = axs.flat

In [182]: bit.index = bit.index / re_premium

In [183]: bit[['p_total', 'logn']].plot(ax=ax0);

In [184]: bit[['p_total', 'logn']].cumsum().plot(ax=ax1);

In [185]: for ax in axs.flat:

.....: for lr in [.35, .55, .65]:

.....: ax.axvline(lr, lw=.5, c='C7')

.....:

In [186]: ax0.set(ylabel='Probability density or mass');

In [187]: ax1.set(ylabel='Probability distribution');

TODO: investigate differences!

2.6.9. Outwards Analysis

Bear and Nemlick’s analysis starts with a description of the frequency and severity of ceded loss. They do not consider the gross portfolio from which the cession occurs. In this section, we model gross, ceded, and net portfolios, mimicking a ceded re or broker actuary evaluation. We use an example from Mata et al. [2002]. Our methods are similar in spirit to theirs, but the details are slightly different, and our estimates do not tie exactly to what they report.

Subject business.

Lawyers and Errors and Omissions (E&O).

Lawyers

Severity curve: lognormal \(\mu=8,\ \sigma=2.5\)

Loss ratio 65%

Exposure

1M premium written with a 750K limit and 10K deductible

2M premium written with a 1M limit and 25K deductible

E&O

Severity curve: lognormal \(\mu=9,\ \sigma=3\)

Loss ratio 75%

Exposure

2M premium written with a 1.5M limit and 50K deductible

3M premium written with a 2M limit and 50K deductible

The total premium equals 8M, assumed split 7.2M for the first million and 800K for the second.

Cessions.

Layer 1: 500 xs 500

Margin plus (retro) rated with provisional rate 12.5% of the premium for the first million, a minimum of 7%, maximum of 18%, and a load (lcf) of 107.5%.

Profit commission of 15% after 20% expenses.

Brokerage: 10% of provisional.

Layer 2: 1M xs 1M

Cessions rated, 800K ceded premium

15% ceding commission

Profit commission 15% after 20%

Brokerage: 10% on gross.

Treaty pricing with these variable features follows the same pattern as Bear and Nemlick and is left as an exercise. This section works with the gross, ceded, and net severity distributions, accounting for the limit profile, and the gross, ceded, and net aggregate distributions.

2.6.9.1. Stochastic Model

Mata et al. assume a negative binomial (gamma mixed Poisson) frequency distribution with a variance to mean ratio of 2.0. When there are relatively few excess claims the resulting mixing CV is close to 0 and the negative binomial is close to a Poisson. We start using a Poisson frequency and then show the impact of moving to a negative binomial.

The basic stochastic model is as follows. Work in 000s. Using bs=1/2 results in a slightly better match to the mean and CV than the recommended bs=1/4.

In [188]: a19 = build('agg Re:MFV41 '

.....: '[1000 2000 2000 3000] premium at [.65 .65 .75 .75] lr '

.....: '[750 1000 1500 2000] xs [10 25 50 50] '

.....: 'sev [exp(8)/1000 exp(8)/1000 exp(9)/1000 exp(9)/1000] '

.....: '* lognorm [2.5 2.5 3 3] '

.....: 'poisson', bs=1/2)

.....:

In [189]: qd(a19)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 22.51 0.21077 0.21077

Sev 253.23 253.23 -9.8245e-07 1.7344 1.7344 2.5007 2.5007

Agg 5700 5700 -9.8245e-07 0.42198 0.42198 0.60601 0.60601

log2 = 16, bandwidth = 1/2, validation: not unreasonable.

The report_df dataframe shows the theoretic and empirical (i.e., modeled) statistics for each unit.

In [190]: qd(a19.report_df.iloc[:, [0,1,2,3,4,-2]])

view 0 1 2 3 independent empirical

statistic

name Re:MFV41 Re:MFV41 Re:MFV41 Re:MFV41 Re:MFV41

limit 750 1000 1500 2000 1202.5

attachment 10 25 50 50 29.468

el 650 1300 1500 2250 5700

freq_m 6.4105 8.2296 3.416 4.4534 22.51

freq_cv 0.39496 0.34859 0.54105 0.47386 0.21077

freq_skew 0.39496 0.34859 0.54105 0.47386 0.21077

sev_m 101.4 157.97 439.1 505.23 253.23 253.23

sev_cv 1.7775 1.6113 1.2123 1.3296 1.7344 1.7344

sev_skew 2.5869 2.3057 1.1514 1.4005 2.5007 2.5007

agg_m 650 1300 1500 2250 5700 5700

agg_cv 0.80551 0.66106 0.85026 0.78834 0.42198 0.42198

agg_skew 1.1642 0.94224 1.04 0.98741 0.60601 0.60601

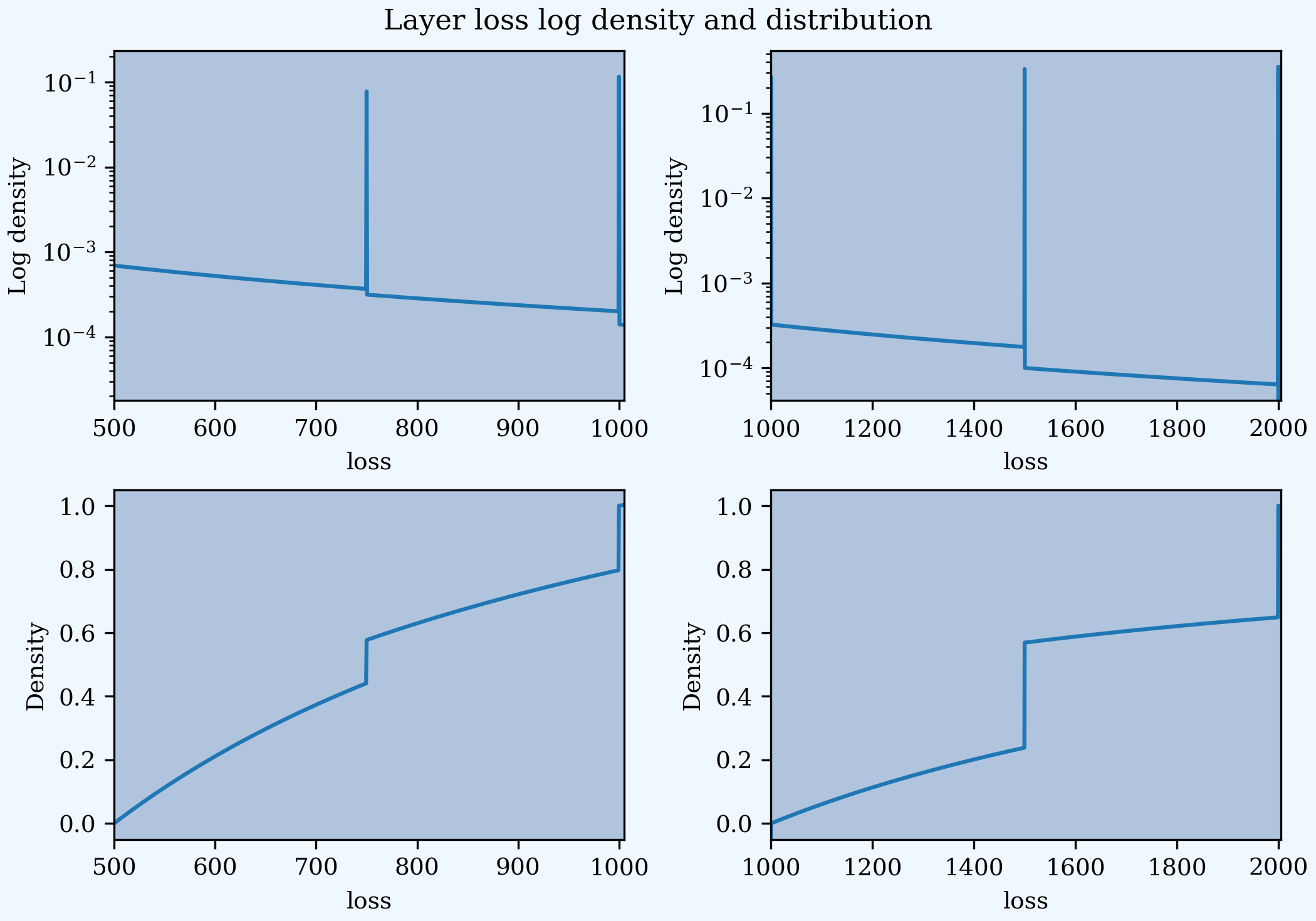

Mata et al. pay careful attention to the implied severity in each ceded layer, accounting for probability masses. They do this by considering losses in small intervals and weighting the underlying severity curves. aggregate automatically performs the same calculations to estimate the total layer severity. In this example, it uses a smaller bucket size of 0.5K compared to 2.5K in the original paper. The next plots reproduce [TODO Differences?!] Figures 2 and 3. The masses (spikes in density; jumps in distribution) occur when the lower limit unit has only limit losses.

In [191]: fig, axs = plt.subplots(2, 2, figsize=(2 * 3.5, 2 * 2.45), constrained_layout=True)

In [192]: ax0, ax1, ax2, ax3 = axs.flat

In [193]: (a19.density_df.p_sev / a19.sev.sf(500)).plot(xlim=[500, 1005], logy=True, ax=ax0);

In [194]: (a19.density_df.p_sev / a19.sev.sf(1000)).plot(xlim=[1000, 2005], logy=True, ax=ax1);

In [195]: ((a19.density_df.F_sev - a19.sev.cdf(500)) / (a19.sev.cdf(1000) - a19.sev.cdf(500))).plot(xlim=[500, 1005], ylim=[-0.05, 1.05], ax=ax2);

In [196]: ((a19.density_df.F_sev - a19.sev.cdf(1000)) / (a19.sev.cdf(2000) - a19.sev.cdf(1000))).plot(xlim=[1000, 2005], ylim=[-0.05, 1.05], ax=ax3);

In [197]: for ax, y in zip(axs.flat, ['Log density', 'Log density', 'Density', 'Density']):

.....: ax.set(ylabel=y);

.....:

In [198]: fig.suptitle('Layer loss log density and distribution');

Use an occurrence net of clause to apply the two excess of loss reinsurance layers. The estimated statistics refer to the net portfolio and reflect a pure exposure rating approach. Gross, ceded, and net expected losses are reported last.

In [199]: a19n = build('agg Re:MFV41n '

.....: '[1000 2000 2000 3000] premium at [.65 .65 .75 .75] lr '

.....: '[750 1000 1500 2000] xs [10 25 50 50] '

.....: 'sev [exp(8)/1000 exp(8)/1000 exp(9)/1000 exp(9)/1000] * lognorm [2.5 2.5 3 3] '

.....: 'occurrence net of 500 xs 500 and 1000 xs 1000 '

.....: 'poisson', bs=1/2)

.....:

In [200]: qd(a19n)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 22.51 0.21077 0.21077

Sev 253.23 153.57 -0.39356 1.7344 1.1741 2.5007 1.0678

Agg 5700 3456.7 -0.39356 0.42198 0.32507 0.60601 0.39439

log2 = 16, bandwidth = 1/2, validation: n/a, reinsurance.

In [201]: print(f'Gross expected loss {a19.est_m:,.1f}\n'

.....: f'Ceded expected loss {a19.est_m - a19n.est_m:,.1f}\n'

.....: f'Net expected loss {a19n.est_m:,.1f}')

.....:

Gross expected loss 5,700.0

Ceded expected loss 2,243.3

Net expected loss 3,456.7

The reinsurance_audit_df dataframe summarizes ground-up (unconditional) layer loss statistics for occurrence covers. Thus, ex reports the layer severity per ground-up claim. The subject (gross) row is the same for all layers and replicates the gross severity statistics shown above for a.

In [202]: qd(a19n.reinsurance_audit_df.stack(0), sparsify=False)

ex var sd cv skew

kind share limit attach

occ 1.0 500.0 500.0 ceded 57.296 22247 149.15 2.6032 2.427

occ 1.0 500.0 500.0 net 195.93 93447 305.69 1.5602 2.5723

occ 1.0 500.0 500.0 subject 253.23 1.929e+05 439.21 1.7344 2.5007

occ 1.0 1000.0 1000.0 ceded 42.365 31584 177.72 4.195 4.4786

occ 1.0 1000.0 1000.0 net 210.86 94455 307.34 1.4575 1.6901

occ 1.0 1000.0 1000.0 subject 253.23 1.929e+05 439.21 1.7344 2.5007

occ all inf gup ceded 99.66 91341 302.23 3.0326 3.4354

occ all inf gup net 153.57 32509 180.3 1.1741 1.0678

occ all inf gup subject 253.23 1.929e+05 439.21 1.7344 2.5007

The reinsurance_occ_layer_df dataframe summarizes aggregate losses.

In [203]: qd(a19n.reinsurance_occ_layer_df, sparsify=False)

stat ex ex ex cv cv cv en severity pct

view ceded net subject ceded net subject ceded ceded ceded

share limit attach

1.0 500.0 500.0 1289.7 4410.3 5700 2.6032 1.5602 1.7344 3.5198 366.41 0.22626

1.0 1000.0 1000.0 953.61 4746.4 5700 4.195 1.4575 1.7344 1.5175 628.41 0.1673

all inf gup 2243.3 3456.7 5700 3.0326 1.1741 1.7344 22.51 99.66 0.39356

The layer severities show above differ slightly from Mata et al. Table 3. The aggregate computation is closest to Method 3. The reported severities are 351.1 and 628.8.

The reinsurance_df dataframe provides the gross, ceded, and net severity and aggregate distributions:

Severity distributions:

p_sev_gross,p_sev_ceded,p_sev_netAggregate distribution:

p_agg_gross_occ,p_agg_ceded_occ,p_agg_net_occshow the aggregate distributions computed using gross, cede, and net severity (occurrence) distributions. These are the portfolio gross, ceded and net distributions.The columns

p_agg_gross,p_agg_ceded,p_agg_netare relevant only when there is areoccurrenceandaggregatereinsurance clauses. They report gross, ceded and net of the aggregate covers, using the severity requested in the occurrence clause. In this casep_agg_grossis the same asp_agg_net_occbecause the occurrence clause specifiednet of.

Here is an extract from the severity distributions. Ceded severity is at most 1500. The masses at 250, 500, 1000 and 1500 are evident.

In [204]: qd(a19n.reinsurance_df.loc[0:2000:250,

.....: ['p_sev_gross', 'p_sev_ceded', 'p_sev_net']])

.....:

p_sev_gross p_sev_ceded p_sev_net

loss

0.0 0.0059219 0.84369 0.0059219

125.0 0.00074474 7.6472e-05 0.00074474

250.0 0.00029874 0.012139 0.00029874

375.0 0.00016663 3.8634e-05 0.00016663

500.0 0.00010806 0.018065 0.15642

625.0 7.6472e-05 1.8367e-05 0

750.0 0.012139 1.5689e-05 0

875.0 3.8634e-05 1.3584e-05 0

1000.0 0.018065 0.022295 0

1125.0 1.8367e-05 5.9515e-06 0

1250.0 1.5689e-05 5.3056e-06 0

1375.0 1.3584e-05 4.7639e-06 0

1500.0 0.022295 0.023679 0

1625.0 5.9515e-06 0 0

1750.0 5.3056e-06 0 0

1875.0 4.7639e-06 0 0

2000.0 0.023679 0 0

Here is an extract from the aggregate distributions, followed by the density and distribution plots. The masses are caused by outcomes involving only limit losses.

In [205]: qd(a19n.reinsurance_df.loc[3000:6000:500,

.....: ['p_agg_gross_occ', 'p_agg_ceded_occ', 'p_agg_net_occ']])

.....:

p_agg_gross_occ p_agg_ceded_occ p_agg_net_occ

loss

3000.0 5.6326e-05 0.0090335 0.00017503

3250.0 6.2846e-05 0.0024374 0.00017886

3500.0 6.8727e-05 0.0050447 0.00017401

3750.0 7.3779e-05 0.0013535 0.00016174

4000.0 7.7914e-05 0.0037091 0.00014418

4250.0 8.1081e-05 0.0010054 0.00012359

4500.0 8.328e-05 0.002359 0.00010216

4750.0 8.4511e-05 0.00063735 8.1596e-05

5000.0 8.4787e-05 0.0012892 6.3111e-05

5250.0 8.4135e-05 0.00034824 4.735e-05

5500.0 8.2634e-05 0.00080992 3.4517e-05

5750.0 8.0373e-05 0.00022017 2.4482e-05

6000.0 7.7463e-05 0.00045425 1.6918e-05

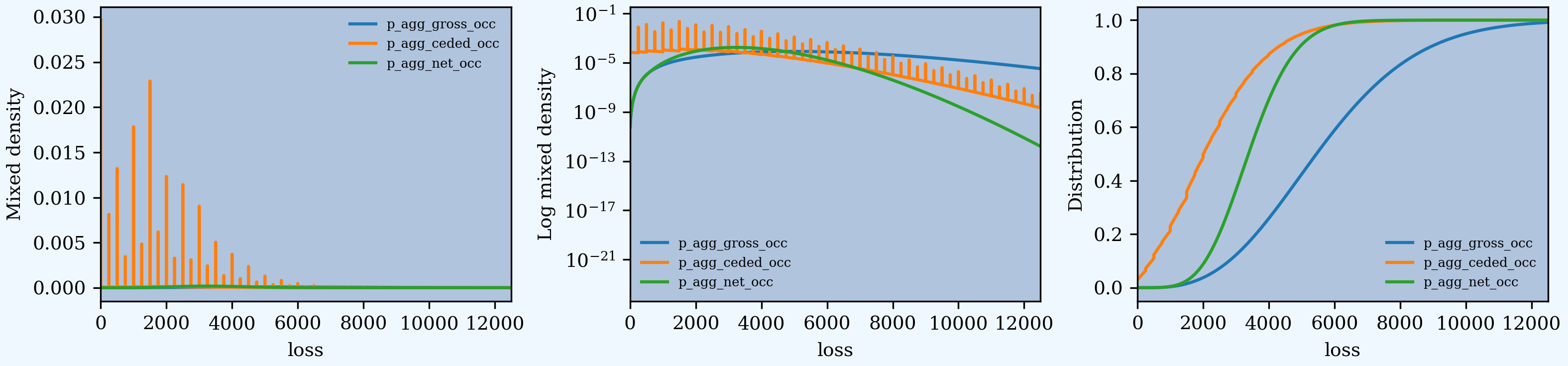

In [206]: fig, axs = plt.subplots(1, 3, figsize=(3 * 3.5, 2.45), constrained_layout=True)

In [207]: ax0, ax1, ax2 = axs.flat

In [208]: bit = a19n.reinsurance_df[['p_agg_gross_occ', 'p_agg_ceded_occ', 'p_agg_net_occ']]

In [209]: bit.plot(ax=ax0);

In [210]: bit.plot(logy=True, ax=ax1);

In [211]: bit.cumsum().plot(ax=ax2);

In [212]: for ax in axs.flat:

.....: ax.set(xlim=[0, 12500]);

.....:

In [213]: ax0.set(ylabel='Mixed density');

In [214]: ax1.set(ylabel='Log mixed density');

In [215]: ax2.set(ylabel='Distribution');

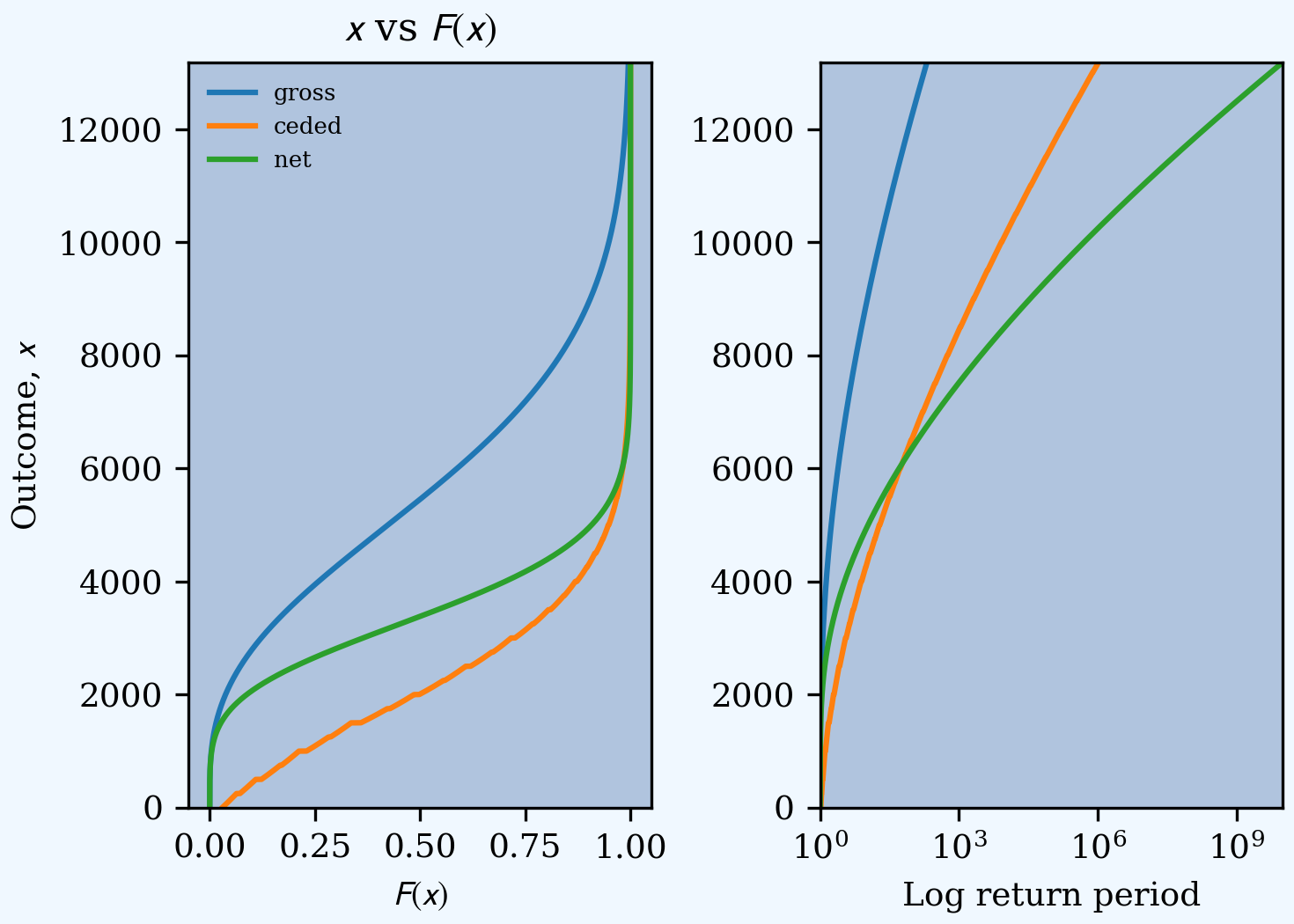

Any desired risk management evaluation can be computed from reinsurance_df, which contains the gross, ceded, and net distributions. For example, here is a tail return period plot and a dataframe of summary statistics.

In [216]: fig, axs = plt.subplots(1, 2, figsize=(2 * 2.45, 3.5), constrained_layout=True)

In [217]: ax0, ax1 = axs.flat

In [218]: for c in bit.columns:

.....: ax0.plot(bit[c].cumsum(), bit.index, label=c.split('_')[2])

.....: rp = 1 / (1 - bit[c].cumsum())

.....: ax1.plot(rp, bit.index, label=c)

.....:

In [219]: ax0.xaxis.set_major_locator(ticker.MultipleLocator(0.25))

In [220]: ax0.set(ylim=[0, a19n.q(1-1e-10)], title='$x$ vs $F(x)$', xlabel='$F(x)$', ylabel='Outcome, $x$');

In [221]: ax1.set(xscale='log', xlim=[1, 1e10], ylim=[0, a19n.q(1-1e-10)], xlabel='Log return period');

In [222]: ax0.legend(loc='upper left');

In [223]: df = pd.DataFrame({c.split('_')[2]: xsden_to_meancvskew(bit.index, bit[c]) for c in bit.columns},

.....: index=['mean', 'cv', 'skew'])

.....:

In [224]: qd(df)

gross ceded net

mean 5700 2243.3 3456.7

cv 0.42198 0.67304 0.32507

skew 0.60601 0.8053 0.39439

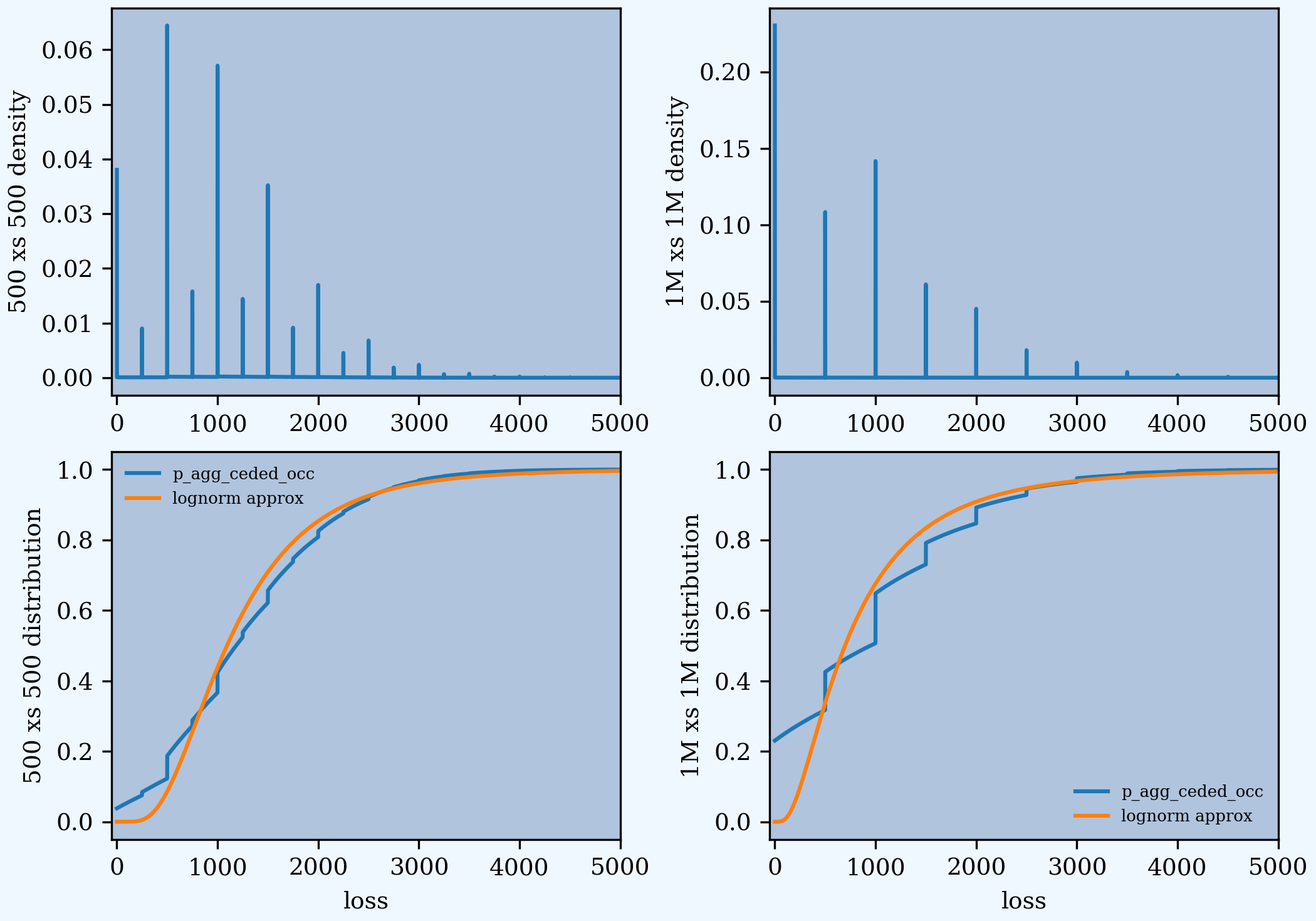

Mata Figures 4, 5, 6 and 7 show the aggregate mixed density and distribution functions for each layer. These plots are replicated below. Our model uses a gamma mixed Poisson frequency with a variance multiplier of 2.0, resulting in a lower variance multiplier for excess layers (see REF). The plots in Mata appear to use a variance multiplier of 2.0 for the excess layer, resulting in a more skewed distribution.

In [225]: from aggregate import lognorm_approx

In [226]: vm = 2.0; c = (vm - 1) / a19.n; cv = c**0.5

In [227]: a20 = build('agg Re:MFV41n1 '

.....: '[1000 2000 2000 3000] premium at [.65 .65 .75 .75] lr '

.....: '[750 1000 1500 2000] xs [10 25 50 50] '

.....: 'sev [exp(8)/1000 exp(8)/1000 exp(9)/1000 exp(9)/1000] * lognorm [2.5 2.5 3 3] '

.....: 'occurrence net of 500 xs 500 '

.....: f'mixed gamma {cv}', bs=1/2)

.....:

In [228]: a21 = build('agg Re:MFV41n2 '

.....: '[1000 2000 2000 3000] premium at [.65 .65 .75 .75] lr '

.....: '[750 1000 1500 2000] xs [10 25 50 50] '

.....: 'sev [exp(8)/1000 exp(8)/1000 exp(9)/1000 exp(9)/1000] * lognorm [2.5 2.5 3 3] '

.....: 'occurrence net of 1000 xs 1000 '

.....: f'mixed gamma {cv}', bs=1/2)

.....:

In [229]: qd(a20)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 22.51 0.29808 0.44712

Sev 253.23 195.93 -0.22626 1.7344 1.5602 2.5007 2.5723

Agg 5700 4410.3 -0.22626 0.4717 0.44384 0.69763 0.68565

log2 = 16, bandwidth = 1/2, validation: n/a, reinsurance.

In [230]: qd(a21)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 22.51 0.29808 0.44712

Sev 253.23 210.86 -0.1673 1.7344 1.4575 2.5007 1.6901

Agg 5700 4746.4 -0.1673 0.4717 0.42805 0.69763 0.60342

log2 = 16, bandwidth = 1/2, validation: n/a, reinsurance.

In [231]: fig, axs = plt.subplots(2, 2, figsize=(2 * 3.5, 2 * 2.45), constrained_layout=True); \

.....: ax0, ax1, ax2, ax3 = axs.flat; \

.....: a20.reinsurance_df.p_agg_ceded_occ.plot(ax=ax0); \

.....: a20.reinsurance_df.p_agg_ceded_occ.cumsum().plot(ax=ax2); \

.....: a21.reinsurance_df.p_agg_ceded_occ.plot(ax=ax1); \

.....: a21.reinsurance_df.p_agg_ceded_occ.cumsum().plot(ax=ax3); \

.....: xs = np.linspace(0, 5000, 501); \

.....: fz = lognorm_approx(a20.reinsurance_df.p_agg_ceded_occ); \

.....: ax2.plot(xs, fz.cdf(xs), label='lognorm approx'); \

.....: fz = lognorm_approx(a21.reinsurance_df.p_agg_ceded_occ); \

.....: ax3.plot(xs, fz.cdf(xs), label='lognorm approx'); \

.....: ax2.legend(); \

.....: ax3.legend(); \

.....: ax0.set(xlim=[-50, 5000], xlabel=None, ylabel='500 xs 500 density'); \

.....: ax2.set(xlim=[-50, 5000], ylabel='500 xs 500 distribution'); \

.....: ax1.set(xlim=[-50, 5000], xlabel=None, ylabel='1M xs 1M density');

.....:

In [232]: ax3.set(xlim=[-50, 5000], ylabel='1M xs 1M distribution');

2.6.10. Summary of Objects Created by DecL

Objects created by build() in this guide.

In [233]: from aggregate import pprint_ex

In [234]: for n, r in build.qlist('^(Re):').iterrows():

.....: pprint_ex(r.program, split=20)

.....:

agg Re:01

dfreq [1 2 3 4 5 6]

dsev [1 2 3 4 5 6]

agg Re:02

dfreq [1:6]

dsev [1:6]

occurrence net of 1 xs 4 and 1 xs 5

agg Re:03

agg.Re:01

aggregate ceded to 6 xs 24 and 6 xs 30

agg Re:04

dfreq [1:6]

dsev [1:6]

occurrence net of 1 xs 4 and 1 xs 5

aggregate net of 4 xs 12 and 4 xs 16

agg Re:05

dfreq [1:6]

dsev [1:6]

occurrence net of 0.5 so 2 xs 2 and 2 xs 4

aggregate net of 1 po 4 xs 10

agg Re:06

agg.Re:01

aggregate ceded to tower [0 1 2 5 10 20 36]

agg Re:07 [10000 5000 2500 1500] premium at [0.75 0.75 0.7 0.65] lr [ 1000 2000 5000 10000] xs [ 0 0 100 250]

sev lognorm 50 cv 10

occurrence ceded to tower [0 250 500 1000 2000 5000 10000]

poisson

agg Re:08 [ 2.975 3.325 4.375 5.25 15.75 28. 31.5 42. 87.5 175. ] premium at [0.55 0.55 0.55 0.55 0.55 0.55 0.55 0.55 0.55 0.55] lr [ 850 950 1250 1500 4500 8000 9000 12000 25000 50000] xs [ 10 10 20 20 50 100 500 1000 5000 5000]

sev [ 850 950 1250 1500 4500 8000 9000 12000 25000 50000] * beta 0.4253774182673055 1.093686593600036 !

occurrence ceded to tower [0 1000 5000 10000 20000 inf]

mixed gamma 2

agg Re:09 [ 2.975 3.325 4.375 5.25 15.75 28. 31.5 42. 87.5 175. ] premium at [0.55 0.55 0.55 0.55 0.55 0.55 0.55 0.55 0.55 0.55] lr [ 850 950 1250 1500 4500 8000 9000 12000 25000 50000] xs [ 10 10 20 20 50 100 500 1000 5000 5000]

sev [ 850 950 1250 1500 4500 8000 9000 12000 25000 50000] * beta 0.4253774182673055 1.093686593600036 !

occurrence ceded to 4000 xs 1000 and 5000 xs 5000

mixed gamma 2

agg Re:BN1 [9000 3000] exposure at [0.04 0.03] rate 160 xs 0

sev 40 * pareto [0.9 0.95] - 40

mixed gamma 0.08357551150546018

agg Re:BN1a [9000 3000] exposure at [0.04 0.03] rate 160 xs 0

sev 40 * pareto [0.9 0.95] - 40

mixed gamma 0.08357551150546018

aggregate net of 360 xs 0

agg Re:BN1c [9000 3000] exposure at [0.04 0.03] rate 160 xs 0

sev 40 * pareto [0.9 0.95] - 40

mixed gamma 0.05**.5

aggregate net of 360 xs 0

agg Re:BN1p [9000 3000] exposure at [0.04 0.03] rate 160 xs 0

sev 40 * pareto [0.9 0.95] - 40

poisson

aggregate net of 360 xs 0

agg Re:BN2 [2000 2000 2000] exposure at [.1 .14 .21] rate 700 xs 0

sev 300 * pareto [1.5 1.3 1.1] - 300

mixed gamma 0.07

agg Re:BN2a [2000 2000 2000] exposure at [.1 .14 .21] rate 700 xs 0

sev 300 * pareto [1.5 1.3 1.1] - 300

mixed gamma 0.07

aggregate ceded to 2800 xs 0

agg Re:BN2p [2000 2000 2000] exposure at [.1 .14 .21] rate 700 xs 0

sev 300 * pareto [1.5 1.3 1.1] - 300

poisson

agg Re:BN3 [4500 4500 1000] exposure at [.032 .038 .035] rate 400 xs 0

sev 100 * pareto 1.1 - 100

poisson

agg Re:BN3lc [4500 4500 1000] exposure at [.032 .038 .035] rate 400 xs 0

sev 100 * pareto 1.1 - 100

poisson

aggregate net of 350 xs 350

agg Re:BN4 [9000 3000] exposure at [0.04 0.03] rate 160 xs 0

sev 40 * pareto [0.9 0.95] - 40

poisson

agg Re:BN5

25000 exposure at 0.1 rate 900 xs 0

sev 100 * pareto 1.05 - 100

mixed gamma 0.095

agg Re:BN6c [6000 6000 6000] exposure at [.1 .14 .21] rate 700 xs 0

sev 300 * pareto [1.5 1.3 1.1] - 300

mixed gamma 0.1**.5

agg Re:BN6p [6000 6000 6000] exposure at [.1 .14 .21] rate 700 xs 0

sev 300 * pareto [1.5 1.3 1.1] - 300

poisson

agg Re:MFV41 [1000 2000 2000 3000] premium at [.65 .65 .75 .75] lr [750 1000 1500 2000] xs [10 25 50 50]

sev [exp(8)/1000 exp(8)/1000 exp(9)/1000 exp(9)/1000] * lognorm [2.5 2.5 3 3]

poisson

agg Re:MFV41n [1000 2000 2000 3000] premium at [.65 .65 .75 .75] lr [750 1000 1500 2000] xs [10 25 50 50]

sev [exp(8)/1000 exp(8)/1000 exp(9)/1000 exp(9)/1000] * lognorm [2.5 2.5 3 3]

occurrence net of 500 xs 500 and 1000 xs 1000

poisson

agg Re:MFV41n1 [1000 2000 2000 3000] premium at [.65 .65 .75 .75] lr [750 1000 1500 2000] xs [10 25 50 50]

sev [exp(8)/1000 exp(8)/1000 exp(9)/1000 exp(9)/1000] * lognorm [2.5 2.5 3 3]

occurrence net of 500 xs 500

mixed gamma 0.21077377162538105

agg Re:MFV41n2 [1000 2000 2000 3000] premium at [.65 .65 .75 .75] lr [750 1000 1500 2000] xs [10 25 50 50]

sev [exp(8)/1000 exp(8)/1000 exp(9)/1000 exp(9)/1000] * lognorm [2.5 2.5 3 3]

occurrence net of 1000 xs 1000

mixed gamma 0.21077377162538105