2.12. Working With Samples

Objectives: How to sample from aggregate and how to a build a Portfolio from a sample. Inducing correlation in a sample using the Iman-Conover algorithm and determining the worst-VaR rearrangement using the rearrangement algorithm.

Audience: Planning and strategy, ERM, capital modeling, risk management actuaries.

Prerequisites: DecL, aggregate distributions, risk measures.

See also: Using Samples and The Switcheroo Trick, The Iman-Conover Method, The Rearrangement Algorithm.

Contents:

Helpful References

2.12.1. Helpful References

2.12.2. Samples and Densities

Use case: make realistic marginal distributions with aggregate that reflect the underlying frequency and severity (rather than defaulting to a lognormal determined by a CV assumption) and then use a sample in your simulation model.

2.12.3. Samples from aggregate Object

The method sample() draws a sample from an Aggregate or Portfolio

class object. Both cases work by applying pandas.DataFrame.sample to the object’s density_df dataframe.

Examples.

A sample from an

Aggregate. Set up a simple lognormal distribution, modeled as an aggregate with trivial frequency.

In [1]: from aggregate import build, qd, set_seed In [2]: a01 = build('agg Samp:01 ' ...: '1 claim ' ...: 'sev lognorm 10 cv .4 ' ...: 'fixed' ...: , bs=1/512) ...: In [3]: qd(a01) E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X) X Freq 1 0 Sev 10 10 -6.1087e-11 0.4 0.4 1.264 1.264 Agg 10 10 -6.1087e-11 0.4 0.4 1.264 1.264 log2 = 16, bandwidth = 1/512, validation: not unreasonable.Apply

sample()and display the results.In [4]: set_seed(102) In [5]: df = a01.sample(10**5) In [6]: fc = lambda x: f'{x:8.2f}' In [7]: qd(df.head(), float_format=fc) loss 0 6.33 1 10.10 2 13.29 3 7.56 4 11.18The sample histogram and the computed pmf are close. The pmf is adjusted to the resolution of the histogram.

In [8]: fig, ax = plt.subplots(1, 1, figsize=(3.5, 2.45), constrained_layout=True) In [9]: xm = a01.q(0.999) In [10]: df.hist(bins=np.arange(xm), ec='w', lw=.25, density=True, ....: ax=ax, grid=False); ....: In [11]: (a01.density_df.loc[:xm, 'p_total'] / a01.bs).plot(ax=ax); In [12]: ax.set(title='Sample and aggregate pmf', ylabel='pmf');

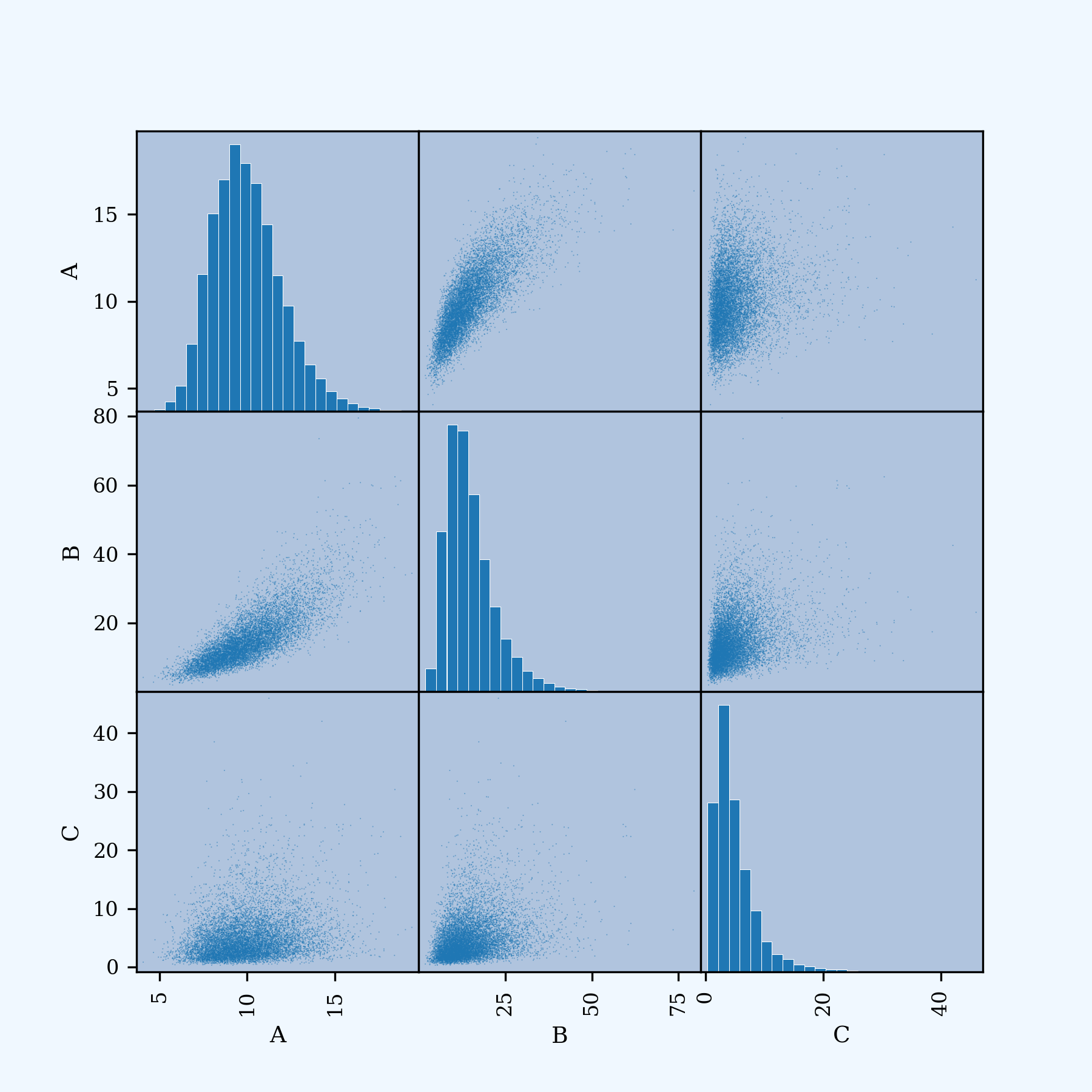

A sample from a

Portfolioproduces a multivariate distribution. Setup a simplePortfoliowith three lognormal marginals.

In [13]: from aggregate.utilities import qdp In [14]: from pandas.plotting import scatter_matrix In [15]: p02 = build('port Samp:02 ' ....: 'agg A 1 claim sev lognorm 10 cv .2 fixed ' ....: 'agg B 1 claim sev lognorm 15 cv .5 fixed ' ....: 'agg C 1 claim sev lognorm 5 cv .8 fixed ' ....: , bs=1/128) ....: In [16]: qd(p02) E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X) unit X A Freq 1 0 Sev 10 10 -2.2204e-16 0.2 0.2 0.608 0.608 Agg 10 10 -2.2204e-16 0.2 0.2 0.608 0.608 B Freq 1 0 Sev 15 15 -2.2282e-13 0.5 0.5 1.625 1.625 Agg 15 15 -2.2282e-13 0.5 0.5 1.625 1.625 C Freq 1 0 Sev 5 5 -2.3183e-10 0.8 0.8 2.912 2.912 Agg 5 5 -2.3183e-10 0.8 0.8 2.912 2.912 total Freq 3 0 Sev 10 10 -3.875e-11 0.64872 1.8077 Agg 30 30 -6.3166e-11 0.29107 0.29107 1.3168 1.3168 log2 = 16, bandwidth = 1/128, validation: not unreasonable.Apply

sample()to produce a sample with no correlation. Here are the first few values.In [17]: df = p02.sample(10**4) In [18]: qd(df.head(), float_format=fc) A B C total 0 9.45 21.07 4.86 35.38 1 11.73 20.10 8.34 40.16 2 10.93 12.06 3.05 26.05 3 7.24 6.34 1.79 15.37 4 8.28 13.30 13.87 35.45

qdp()prints the pandasdescribestatistics dataframe for a dataframe, and adds the CV.In [19]: qdp(df) Out[19]: A B C total count 10000.000000 10000.000000 10000.000000 10000.000000 mean 9.966709 15.052769 5.058216 30.077694 std 2.002445 7.583697 4.047945 8.889127 min 3.664062 2.117188 0.250000 11.726562 25% 8.539062 9.773438 2.484375 23.781250 50% 9.789062 13.351562 4.000000 28.507812 75% 11.187500 18.609375 6.257812 34.640625 max 21.078125 81.070312 45.562500 115.281250 cv 0.200913 0.503807 0.800271 0.295539The sample is independent, with correlations close to zero, as expected.

In [20]: abc = ['A', 'B', 'C'] In [21]: qd(df[abc].corr()) A B C A 1 0.0058516 -0.0021565 B 0.0058516 1 0.015729 C -0.0021565 0.015729 1The scatterplot is consistent with independent marginals.

In [22]: scatter_matrix(df[abc], grid=False, ....: figsize=(6, 6), diagonal='hist', ....: hist_kwds={'density': True, 'bins': 25, 'lw': .25, 'ec': 'w'}, ....: s=1, marker='.'); ....:

Pass a correlation matrix to

sample()to draw a correlated sample. Correlation is induced using the Iman-Conover algorithm.

The function

random_corr_matrix()creates a random correlation matrix using vines. The second parameter controls the average correlation. This example includes high positive correlation.In [23]: from aggregate import random_corr_matrix In [24]: rcm = random_corr_matrix(3, .6, True) In [25]: rcm Out[25]: matrix([[1. , 0.80331094, 0.24377874], [0.80331094, 1. , 0.35448898], [0.24377874, 0.35448898, 1. ]])Re-sample with target correlation

rcm. The achieved correlation is reasonably close to the requestedrcm.In [26]: df2 = p02.sample(10**4, desired_correlation=rcm) In [27]: qd(df2.iloc[:, :3].corr('pearson')) A B C A 1 0.78513 0.22481 B 0.78513 1 0.31656 C 0.22481 0.31656 1The scatterplot now shows correlated marginals. The histograms are unchanged.

In [28]: df2['total'] = df2.sum(1) In [29]: scatter_matrix(df2[abc], grid=False, figsize=(6, 6), diagonal='hist', ....: hist_kwds={'density': True, 'bins': 25, 'lw': .25, 'ec': 'w'}, ....: s=1, marker='.'); ....:

The sample uses a different random state and produces a different draw. Comparing

qdpoutput is one way to see if 10000 simulations is adequate. In this case there is good agreement.In [30]: qdp(df2) Out[30]: A B C total count 10000.000000 10000.000000 10000.000000 10000.000000 mean 9.991469 14.969470 4.987341 29.948280 std 1.997495 7.389115 3.910557 10.902512 min 4.070312 1.984375 0.304688 8.242188 25% 8.570312 9.742188 2.414062 22.304688 50% 9.789062 13.406250 3.906250 27.867188 75% 11.179688 18.351562 6.273438 35.460938 max 19.398438 79.468750 45.937500 111.164062 cv 0.199920 0.493612 0.784097 0.364045

2.12.4. Applying the Iman-Conover Algorithm

The method sample() automatically applies the Iman-Conover algorithm (described in The Iman-Conover Method). It is also easy to apply Iman-Conover to a dataframe using the method aggregate.utilities.iman_conover(). It reorders the input dataframe to have the same rank correlation as a multivariate normal reference sample with the desired linear correlation. Optionally, a multivariate t-distribution can be used as the reference.

Examples.

Apply Iman-Conover to the sample df with target the correlation rcm, reusing the variables created in the previous section. The achieved correlation is close to that requested, as shown in the last two blocks.

In [31]: from aggregate import iman_conover

In [32]: import pandas as pd

In [33]: ans = iman_conover(df[abc], rcm, add_total=False)

In [34]: qd(pd.DataFrame(rcm, index=abc, columns=abc))

A B C

A 1 0.80331 0.24378

B 0.80331 1 0.35449

C 0.24378 0.35449 1

In [35]: qd(ans.corr())

A B C

A 1 0.78111 0.22247

B 0.78111 1 0.31237

C 0.22247 0.31237 1

Setting the argument dof uses a t-copula reference with dof degrees of freedom. The t-copula with low degrees of freedom can produce pinched multivariate distributions. Use with caution.

In [36]: ans = iman_conover(df[abc], rcm, dof=2, add_total=False)

In [37]: qd(ans.corr())

A B C

A 1 0.86152 0.51261

B 0.86152 1 0.49706

C 0.51261 0.49706 1

In [38]: scatter_matrix(ans, grid=False, figsize=(6, 6), diagonal='hist',

....: hist_kwds={'density': True, 'bins': 25, 'lw': .25, 'ec': 'w'},

....: s=1, marker='.');

....:

See WP REF for ways to apply Iman-Conover with different reference distributions.

Details. Creating the independent scores for Iman-Conover is quite time consuming. They are cached for a given sample size. Second and subsequent calls are far quicker (an order of magnitude) than the first call.

2.12.5. Applying the Re-Arrangement Algorithm

The method rearrangement_algorithm_max_VaR() implements the re-arrangement algorithm described in ../5_technical_guides/5_x_rearrangement_algorithm. It returns only the tail of the re-arrangement, since values below the requested percentile are irrelevant.

Apply to df and request 0.999-VaR. The marginals are the 10 largest values. The algorithm permutes them to balance large and small observations.

In [39]: from aggregate import rearrangement_algorithm_max_VaR

In [40]: ans = rearrangement_algorithm_max_VaR(df.iloc[:, :3], .999)

In [41]: qd(ans, float_format=fc)

A B C total

0 21.08 63.78 38.59 123.45

6 20.22 65.18 38.40 123.80

1 20.63 62.50 40.80 123.93

3 18.93 65.02 40.24 124.20

5 17.98 60.66 45.56 124.20

2 18.02 68.88 37.33 124.23

7 17.75 61.75 44.91 124.41

9 19.99 66.28 38.22 124.49

8 17.69 73.03 37.12 127.84

4 17.59 81.07 37.03 135.70

Here are the stand-alone sa VaRs by marginal, in total for df, in total for the correlated df2, and the re-arrangement solutions ra for a range of different percentiles. The column comon total shows VaR for the comonotonic sum of the marginals (which equals the largest TVaR and variance re-arrangement).

In [42]: ps = [9000, 9500, 9900, 9960, 9990, 9999]

In [43]: sa = pd.concat([df[c].sort_values().reset_index(drop=True).iloc[ps] for c in df]

....: +[df2.rename(columns={'total':'corr total'})['corr total'].\

....: sort_values().reset_index(drop=True).iloc[ps]], axis=1)

....:

In [44]: sa['comon total'] = sa[abc].sum(1)

In [45]: ra = pd.concat([rearrangement_algorithm_max_VaR(df.iloc[:, :3], p/10000).iloc[0] for p in ps],

....: axis=1, keys=ps).T

....:

In [46]: exhibit = pd.concat([sa, ra], axis=1, keys=['stand-alone', 're-arrangement'])

In [47]: exhibit.index = [f'{x/10000:.2%}' for x in exhibit.index]

In [48]: exhibit.index.name = 'percentile'

In [49]: qd(exhibit, float_format=fc)

stand-alone re-arrangement \

A B C total corr total comon total A B

percentile

90.00% 12.59 24.75 9.73 41.48 44.22 47.06 15.64 28.69

95.00% 13.55 29.21 12.68 46.48 50.43 55.44 16.42 32.19

99.00% 15.45 39.98 20.55 58.15 65.26 75.98 17.75 44.51

99.60% 16.36 47.62 26.58 68.00 73.50 90.56 17.59 59.56

99.90% 17.59 60.66 37.03 80.20 93.51 115.28 21.08 63.78

99.99% 21.08 81.07 45.56 115.28 111.16 147.71 21.08 81.07

C total

percentile

90.00% 12.70 57.02

95.00% 16.98 65.59

99.00% 26.37 88.62

99.60% 28.77 105.92

99.90% 38.59 123.45

99.99% 45.56 147.71

See also Worked Example.

2.12.6. Creating a Portfolio From a Sample

A Portfolio can be created from an existing sample by passing in a dataframe rather than a list of aggregates. This approach is useful when another model has created the sample, but the user wants to access other aggregate functionality. Each marginal in the sample is created as a dsev with the sampled outcomes. The p_total column used to set scenario probabilities if its is input, otherwise each scenario is treated as equally likely. The Portfolio ignores any the correlation structure of the sample; the marginals are treated as independent, but see Using Samples and the Switcheroo Trick for a way around this assumption.

Example.

Create a simple discrete sample from a three unit portfolio.

In [50]: sample = pd.DataFrame(

....: {'A': [20, 22, 24, 6, 5, 6, 7, 8, 21, 3],

....: 'B': [20, 18, 16, 14, 12, 10, 8, 6, 4, 2],

....: 'C': [0, 0, 0, 0, 0, 0, 0, 0, 20, 40]})

....:

In [51]: qd(sample)

A B C

0 20 20 0

1 22 18 0

2 24 16 0

3 6 14 0

4 5 12 0

5 6 10 0

6 7 8 0

7 8 6 0

8 21 4 20

9 3 2 40

Pass to Portfolio to create with these marginals. In this case, treat the marginals as discrete and update with bs=1.

In [52]: from aggregate import Portfolio

In [53]: p03 = Portfolio('Samp:03', sample)

In [54]: p03.update(bs=1, log2=8)

In [55]: qd(p03)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

A Freq 1 0

Sev 12.2 12.2 0 0.65142 0.65142 0.37792 0.37792

Agg 12.2 12.2 0 0.65142 0.65142 0.37792 0.37792

B Freq 1 0

Sev 11 11 0 0.52223 0.52223 0 0

Agg 11 11 0 0.52223 0.52223 0 0

C Freq 1 0

Sev 6 6 -3.3307e-16 2.1344 2.1344 1.9198 1.9198

Agg 6 6 -3.3307e-16 2.1344 2.1344 1.9198 1.9198

total Freq 3 0

Sev 9.7333 9.7333 0 0.99572 1.0775

Agg 29.2 29.2 -3.3307e-16 0.55238 0.55238 1.0061 1.0061

log2 = 8, bandwidth = 1, validation: not unreasonable.

The univariate statistics for each marginal are the same as the sample input, but because they added independently, the totals differ. The sample has negative correlation and a lower CV.

In [56]: sample['total'] = sample.sum(1)

In [57]: qdp(sample)

Out[57]:

A B C total

count 10.000000 10.000000 10.000000 10.000000

mean 12.200000 11.000000 6.000000 29.200000

std 7.947327 5.744563 12.806248 12.998461

min 3.000000 2.000000 0.000000 14.000000

25% 6.000000 6.500000 0.000000 16.250000

50% 7.500000 11.000000 0.000000 30.000000

75% 20.750000 15.500000 0.000000 40.000000

max 24.000000 20.000000 40.000000 45.000000

cv 0.651420 0.522233 2.134375 0.445153

The Portfolio total is a convolution of the input marginals and includes all possible combinations added independently. The figure plots the distribution functions.

In [58]: ax = p03.density_df.filter(regex='p_[ABCt]').cumsum().plot(

....: drawstyle='steps-post', lw=1, figsize=(3.5, 2.45))

....:

In [59]: ax.plot(np.hstack((0, sample.total.sort_values())), np.linspace(0, 1, 11),

....: drawstyle='steps-post', lw=2, label='dependent');

....:

In [60]: ax.set(xlim=[-2, 90]);

In [61]: ax.legend(loc='lower right');

2.12.7. Using Samples and the Switcheroo Trick

Portfolio objects created from a sample ignore the dependency structure; the aggregate convolution algorithm always assumes independence. It is highly desirable to retain the sample’s dependency structure. Many calculations rely only on \(\mathsf E[X_i\mid X]\) and not the input densities per se. Thus, we reflect dependency if we alter the values \(\mathsf E[X_i\mid X]\) based on a sample and recompute everything that depends on them. The method Portfolio.add_exa_sample() implements this idea.

Example.

sample was chosen to have lots of ties - different ways of obtaining the same total outcome.

In [62]: qd(sample)

A B C total

0 20 20 0 40

1 22 18 0 40

2 24 16 0 40

3 6 14 0 20

4 5 12 0 17

5 6 10 0 16

6 7 8 0 15

7 8 6 0 14

8 21 4 20 45

9 3 2 40 45

Apply add_exa_sample to the sample dataframe and look at the outcomes with positive probability. When a total outcome can occur in multiple ways, exeqa_i gives the average value of unit i.

The function is applied to a copy of the original Portfolio object because it invalidates various internal states. The output dataframe is indexed by total loss. Notice that rows sum to the correct total.

In [63]: p03sw = Portfolio('Samp:03sw', sample)

In [64]: p03sw.update(bs=1, log2=8)

In [65]: df = p03sw.add_exa_sample(sample)

In [66]: qd(df.query('p_total > 0').filter(regex='p_total|exeqa_[ABC]'))

p_total exeqa_A exeqa_B exeqa_C

14.0 0.1 8 6 0

15.0 0.1 7 8 0

16.0 0.1 6 10 0

17.0 0.1 5 12 0

20.0 0.1 6 14 0

40.0 0.3 22 18 0

45.0 0.2 12 3 30

Swap the density_df dataframe — the switcheroo trick.

In [67]: p03sw.density_df = df

See the function Portfolio.create_from_sample for a single step create from sample, update, add exa calc, and switcheroo.

Most Portfolio spectral functions depend only on marginal conditional expectations. Applying these functions through p03sw reflects dependencies. Calibrate some distortions to a 15% return. The maximum loss is only 45, so use a 1-VaR, no default capital standard.

In [68]: p03sw.calibrate_distortions(ROEs=[0.15], Ps=[1], strict='ordered');

In [69]: qd(p03sw.distortion_df)

S L P PQ Q COC param std_param error

a LR method

45.0 0.934075 ccoc 0 29.2 31.261 2.2753 13.739 0.15 0.15 0.13043 0

ph 0 29.2 31.261 2.2753 13.739 0.15 0.80913 0.1055 4.1444e-09

wang 0 29.2 31.261 2.2753 13.739 0.15 0.18223 0.10253 -1.6102e-07

dual 0 29.2 31.261 2.2753 13.739 0.15 1.228 0.10234 -9.8354e-08

tvar 0 29.2 31.261 2.2753 13.739 0.15 0.12059 0.12059 5.935e-06

Apply the PH and dual to the independent and dependent portfolios. Asset level 45 is the 0.861 percentile of the independent.

In [70]: d1 = p03sw.dists['ph']; d2 = p03sw.dists['dual']

In [71]: for d in [d1, d2]:

....: print(d.name)

....: print('='*74)

....: pr = p03.price(1, d)

....: pr45 = p03.price(.861, d)

....: prsw = p03sw.price(1, d)

....: a = pd.concat((pr.df, pr45.df, prsw.df), keys=['pr', 'pr45', 'prsw'])

....: qd(a, float_format=lambda x: f'{x:7.3f}')

....:

ph

==========================================================================

statistic L P M Q a LR PQ COC

distortion unit

pr ph A 12.200 12.944 0.744 13.129 26.073 0.943 0.986 0.057

B 11.000 11.376 0.376 9.544 20.919 0.967 1.192 0.039

C 6.000 8.400 2.400 28.608 37.008 0.714 0.294 0.084

total 29.200 32.719 3.519 51.281 84.000 0.892 0.638 0.069

pr45 ph A 11.675 12.059 0.384 3.624 15.682 0.968 3.328 0.106

B 10.578 10.674 0.096 2.160 12.834 0.991 4.941 0.045

C 4.803 6.457 1.654 10.027 16.484 0.744 0.644 0.165

total 27.055 29.189 2.134 15.811 45.000 0.927 1.846 0.135

prsw ph A 12.200 12.571 0.371 3.371 15.942 0.970 3.729 0.110

B 11.000 10.532 -0.468 -0.187 10.345 1.044 -56.386 2.507

C 6.000 8.158 2.158 10.555 18.713 0.736 0.773 0.204

total 29.200 31.261 2.061 13.739 45.000 0.934 2.275 0.150

dual

==========================================================================

statistic L P M Q a LR PQ COC

distortion unit

pr dual A 12.200 13.061 0.861 15.011 28.071 0.934 0.870 0.057

B 11.000 11.523 0.523 11.590 23.113 0.955 0.994 0.045

C 6.000 7.171 1.171 25.645 32.816 0.837 0.280 0.046

total 29.200 31.754 2.554 52.246 84.000 0.920 0.608 0.049

pr45 dual A 11.675 12.422 0.747 5.480 17.902 0.940 2.267 0.136

B 10.578 11.009 0.432 4.186 15.195 0.961 2.630 0.103

C 4.803 5.716 0.914 6.187 11.903 0.840 0.924 0.148

total 27.055 29.148 2.093 15.852 45.000 0.928 1.839 0.132

prsw dual A 12.200 12.874 0.674 4.947 17.821 0.948 2.602 0.136

B 11.000 11.197 0.197 2.644 13.840 0.982 4.235 0.074

C 6.000 7.191 1.191 6.148 13.339 0.834 1.170 0.194

total 29.200 31.261 2.061 13.739 45.000 0.934 2.275 0.150

2.12.8. Summary of Objects Created by DecL

Objects created by build() in this guide. Objects created directly by class constructors are not entered into the knowledge database.

In [72]: from aggregate import pprint_ex

In [73]: for n, r in build.qlist('^Samp:').iterrows():

....: pprint_ex(r.program, split=20)

....:

agg Samp:01

1 claim

sev lognorm 10 cv .4

fixed

port Samp:02

agg A

1 claim

sev lognorm 10 cv .2

fixed

agg B

1 claim

sev lognorm 15 cv .5

fixed

agg C

1 claim

sev lognorm 5 cv .8

fixed