2.3. A Ten Minute Guide to aggregate

Objectives: A whirlwind introduction—don’t expect to understand everything the first time, but you will see what you can achieve with the package. Follows the pandas model, a long 10 minutes.

Audience: A new user.

Prerequisites: Python programming; aggregate distributions. Read in conjunction with Student or Actuarial Student practice guides.

See also: API Reference, The Dec Language.

Contents:

-

-

Estimating Bucket Size for Discretization

Methods and Properties Common To Aggregate and Portfolio Classes

-

2.3.1. Principle Classes

The aggregate package makes working with aggregate probability distributions as straightforward as working with parametric distributions even though their densities rarely have closed-form expressions. It is built around five principal classes.

The

Underwriterclass keeps track of everything in itsknowledgedataframe, interprets Dec Language (DecL, pronounced like deckle, /ˈdɛk(ə)l/) programs, and acts as a helper.The

Severityclass models a size of loss distribution (a severity curve).The

Aggregateclass models a single unit of business, such as a line, business unit, geography, or operating division.The

Distortionclass provides a distortion function, the basis of a spectral risk measure.The

Portfolioclass models multiple units. It extends the functionality inAggregate, adding pricing, calibration, and allocation capabilities.

There is also a Frequency class that Aggregate derives from, but it is rarely used standalone, and a Bounds class for advanced users.

2.3.2. The Underwriter Class

The Underwriter class is an interface into the computational functionality of aggregate. It does two things:

Creates objects using the DecL language, and

Maintains a library of DecL object specifications called the knowledge. New objects are automatically added to the knowledge.

To get started, import build, a pre-configured Underwriter and qd(), a quick-display function. Import the usual suspects too, for good measure.

In [1]: from aggregate import build, qd

In [2]: import pandas as pd, numpy as np, matplotlib.pyplot as plt

Printing build reports its name, the number of objects in its knowledge, and other information about hyper-parameter default values. site_dir is where various outputs will be stored. default_dir is for internal package data. The build object loads an extensive test suite of DecL programs with over 130 entries.

In [3]: build

Out[3]:

underwriter Rory

version 0.30.1

knowledge 146 programs

update True

log2 16

debug False

validation_eps 0.0001

site dir ~/aggregate/databases

default dir ~/checkouts/readthedocs.org/user_builds/aggregate/checkouts/latest/aggregate/agg

help

build.knowledge list of all programs

build.qshow(pat) show programs matching pattern

build.show(pat) build and display matching pattern

2.3.2.1. Object Creation Using DecL and build()

The Underwriter class interprets DecL programs (The Dec Language). These allow severities, aggregates and portfolios to be created using standard insurance language.

For example, to build an Aggregate using DecL and report key statistics for frequency, severity, and aggregate, needs just two commands.

In [4]: a01 = build('agg TenM:01 100 claims 100 xs 0 sev lognorm 10 cv 1.25 poisson')

In [5]: qd(a01)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 100 0.1 0.1

Sev 9.918 9.918 2.8323e-10 1.1639 1.1639 3.4165 3.4165

Agg 991.8 991.8 -4.5177e-10 0.15345 0.15345 0.28923 0.28923

log2 = 16, bandwidth = 1/32, validation: not unreasonable.

DecL is supposed to be human-readable, so I hope you can guess the meaning of the DecL code (TenM:01 is just a label):

agg TenM:01 5 claims 1000 xs 0 sev lognorm 50 cv 4 poisson

The units are 1000s of USD, EUR, or GBP.

DecL is a custom language, created to describe aggregate distributions. Alternatives are to use positional arguments or key word arguments in function calls. The former are confusing because there are so many. The latter are verbose, because of the need to specify the parameter name. DecL is a concise, expressive, flexible, and powerful alternative.

2.3.2.2. Important: Formatting a DecL Program

Important

All DecL programs are one line long.

It is best to break a DecL program up to make it more readable. The fact that Python automatically concatenates strings between parenthesis makes this easy. The program above is always entered in the help as:

a01 = build('agg TenM:01 '

'100 claims '

'100 xs 0 '

'sev lognorm 10 cv 1.25 '

'poisson')

which Python makes equivalent to:

a01 = build('agg TenM:01 100 claims 100 xs 0 sev lognorm 10 cv 1.25 poisson')

as originally entered. Pay attention to spaces at the end of each line! Entering:

a01 = build('agg TenM:01'

'100 claims'

'100 xs 0'

'sev lognorm 10 cv 1.25'

'poisson')

produces:

a01 = build('agg TenM:01100 claims100 xs 0sev lognorm 10 cv 1.25poisson')

which results in syntax errors.

DecL includes a Python newline \. All programs in the help are entered so they can be cut and pasted.

2.3.2.3. Object Creation from the Knowledge Database

The knowledge dataframe is a database of DecL programs and a parsed

dictionaries to create objects. build loads an extensive library by

default. Users can create and load their own databases, allowing them to share common parameters for

severity (size of loss) curves,

aggregate distributions (e.g., industry losses in major classes of business, or total catastrophe losses from major perils), and

portfolios (e.g., an insurer’s reference portfolio or educational examples like Bodoff’s examples and Pricing Insurance Risk case studies).

It is indexed by object kind (severity, aggregate, portfolio) and name, and accessed as the read-only property build.knowledge. Here are the first five rows of the knowledge loaded by build.

In [6]: qd(build.knowledge.head(), justify="left", max_colwidth=60)

program \

kind name

agg A.Dice00 agg A.Dice00 dfreq [1:6] dsev [1] note{The roll of a...

A.Dice01 agg A.Dice01 dfreq [1] dsev [1:6] note{Same as previ...

A.Dice02 agg A.Dice02 dfreq [2] dsev [1:6] note{Sum of the ro...

A.Dice03 agg A.Dice03 dfreq [5] dsev [1:6] note{Sum of the ro...

A.Dice04 agg A.Dice04 dfreq [1:6] dsev [1:6] note{Sum of a di...

spec

kind name

agg A.Dice00 {'name': 'A.Dice00', 'freq_name': 'empirical', 'freq_a':...

A.Dice01 {'name': 'A.Dice01', 'freq_name': 'empirical', 'freq_a':...

A.Dice02 {'name': 'A.Dice02', 'freq_name': 'empirical', 'freq_a':...

A.Dice03 {'name': 'A.Dice03', 'freq_name': 'empirical', 'freq_a':...

A.Dice04 {'name': 'A.Dice04', 'freq_name': 'empirical', 'freq_a':...

A row in the knowledge can be accessed by name using build. This example models the roll of a single die.

In [7]: print(build['A.Dice00'])

kind agg

name A.Dice00

spec <class 'dict'>

program agg A.Dice00 dfreq [1:6] dsev [1] note{The roll of a single dice.}

object <class 'NoneType'>

The argument 'A.Dice00' is passed through to the underlying dataframe’s getitem.

A row in the knowledge can be created as a Python object using:

In [8]: aDice = build('A.Dice00')

In [9]: qd(aDice)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3.5 0.48795 0

Sev 1 1 0 0 0

Agg 3.5 3.5 4.4409e-16 0.48795 0.48795 0 4.85e-14

log2 = 4, bandwidth = 1, validation: not unreasonable.

The argument in this case is passed through to the method Underwriter.build(), which first looks for A.Dice00 in the knowledge. If it fails, it tries to interpret its argument as a DecL program.

The method build.qlist() (quick list) searches the knowledge using a regex (regular expression) applied to the names, and returning a dataframe of specifications. build.qshow() (quick show) just displays them.

In [10]: build.qshow('Dice')

program

name

A.Dice00 agg A.Dice00 dfreq [1:6] dsev [1] note{The roll of a single dice.}

A.Dice01 agg A.Dice01 dfreq [1] dsev [1:6] note{Same as previous example.}

A.Dice02 agg A.Dice02 dfreq [2] dsev [1:6] note{Sum of the rolls of two dice.}

A.Dice03 agg A.Dice03 dfreq [5] dsev [1:6] note{Sum of the rolls of five dice.}

A.Dice04 agg A.Dice04 dfreq [1:6] dsev [1:6] note{Sum of a dice roll of dice rolls}

A.Dice05 agg A.Dice05 dfreq [1:4] dsev [1:16] note{Something you can't do easily by hand}

The method build.show() also searches the knowledge using a regex applied to the names, but it creates and plots each match by default. Be careful not to create too many objects! Try running:

build.show('Dice')

Add argument return_df=True to return a list of created objects and a dataframe containing information about each.

2.3.2.4. Underwriter Behind the Scenes

This section should be skipped the first time through.

Each object has a kind property and a name property, and it can be manifest as a DecL program, a dictionary specification, or a Python class instance. The class can be updated or not updated. In detail:

kind equals sev for a

Severity, agg for aAggregate, port for aPortfolio, and distortion for aDistortion(dist could be distribution);name is assigned to the object by the user; it is different from the Python variable name holding the object;

spec is a (derived) dictionary specification;

program is the DecL program as a text string; and

object is the actual Python object, an instance of a class.

Underwriter.write() is a low-level creator function. It takes a DecL program or knowledge item name as input.

It searches the knowledge for the argument and returns it if it finds one object. It throws an error if the name is not unique. If the name is not in the knowledge it continues.

It calls

Underwriter.interpret_program()to pre-process the DecL and then lex and parse it one line at a time.It looks up occurrences of

sev.ID,agg.ID(IDis an object name) in the knowledge and replaces them with their definitions.It calls

Underwriter.factory()to create any objects and update them if requested.It returns a list of

Answerobjects, with kind, name, spec, program, and object attributes.

Underwriter.write_file() reads a file and passes it to Underwriter.write(). It is a convenience function.

The Underwriter.build() method wraps the

Underwriter.write() and provides sensible defaults to shield the user from its internal details. \(build\) takes the following steps:

It calls

write()withupdate=False.It then estimates sensible hyper-parameters and uses them to

update()the object’s discrete distribution. It tries to distinguish discrete output distributions from continuous or mixed ones.If the DecL program produces only one output, it strips it out of the answer returned by

writeand returns just that object.If the DecL program produces only one portfolio output (but possibly other non-portfolio objects), it returns just that.

Underwriter.interpret_program() interprets DecL programs and matches them with the parsed specs in an Answer(kind, name, spec, program, object=None) object. It adds the result to the knowledge.

Underwriter.factory() takes an Answer argument and updates it by creating the relevant object and updating it if build.update is True.

A set of methods called interpreter_xxx() run DecL programs through parser for debugging purposes, but do not create any output or add anything to the knowledge.

Underwriter.interpreter_line()works on one line.Underwriter.interpreter_file()works on each line in a file.Underwriter.interpreter_list()works on each item in a list.Underwriter._interpreter_work()does the actual parsing.

2.3.3. How aggregate Represents Distributions

A distribution is represented as a discrete numerical approximation. To “know or compute a distribution” means that we have a discrete stair-step approximation to the true distribution function that jumps (is supported) only on integer multiples of a fixed bandwidth or bucket size \(b\) (called bs in the code). The distribution is represented by \(b\) and a vector of probabilities \((p_0,p_1,\dots, p_{n-1})\) with the interpretation

All subsequent computations assume that this approximation is the distribution. For example, moments are estimated using

See Digital Representation of Distributions for more details.

2.3.4. The Severity Class

The Severity class derives from scipy.stats.rv_continuous, see scipy help. It contains a member stats.rv_continuous variable fz that is the ground-up unlimited severity and it adds support for limits and attachments. For example, the cdf function is coded:

def _cdf(self, x, *args):

if self.conditional:

return np.where(x >= self.limit, 1,

np.where(x < 0, 0,

(self.fz.cdf(x + self.attachment) -

(1 - self.pattach)) / self.pattach))

else:

return np.where(x < 0, 0,

np.where(x == 0, 1 - self.pattach,

np.where(x > self.limit, 1,

self.fz.cdf(x + self.attachment, *args))))

Severity can determine its shape parameter from a CV analytically for lognormal, gamma, inverse gamma, and inverse Gaussian distributions, and attempts to use a Newton-Raphson method to determine it for all other one-shape parameter distributions. (The CV is adjusted using the scale factor for zero parameter distributions.) Once the shape is known, it uses scaling to produce the required mean. Warning: The numerical methods are not always reliable.

Severity computes layer moments analytically for the lognormal, Pareto, and gamma, and uses numerical integration of the quantile function (isf) for all other distributions. These estimates can become unreliable for very thick tailed distributions. It uses self.fz.stats('mvs') and the object limit to determine if the requested moment actually exists before attempting numerical integration.

Severity has a plot() method that graphs the density, log density, cdf, and quantile (Lee) functions.

A Severity can be created using DecL using any of the following five forms.

sev NAME sev.BUILDIN_IDis a knowledge lookup forBUILTIN_IDsev NAME DISTNAME SHAPE1 <SHAPE2>whereDISTAMEis the name of anyscipy.statscontinuous random variable with zero, one, or two shape parameters, see the DecL/list of distributions.sev NAME SCALE * DISTNAME SHAPE1 <SHAPE2> + LOCsev NAME DISTNAME MEAN cv CVsev NAME SCALE * DISTNAME MEAN cv CV + LOCorsev NAME SCALE * DISTNAME MEAN cv CV - LOC

Either or both of SCALE and LOC can be present. In the mean and CV form, the mean refers to the unshifted, unscaled mean, but the CV refers to the shifted and scaled CV — because you usually want to control the overall CV.

Example.

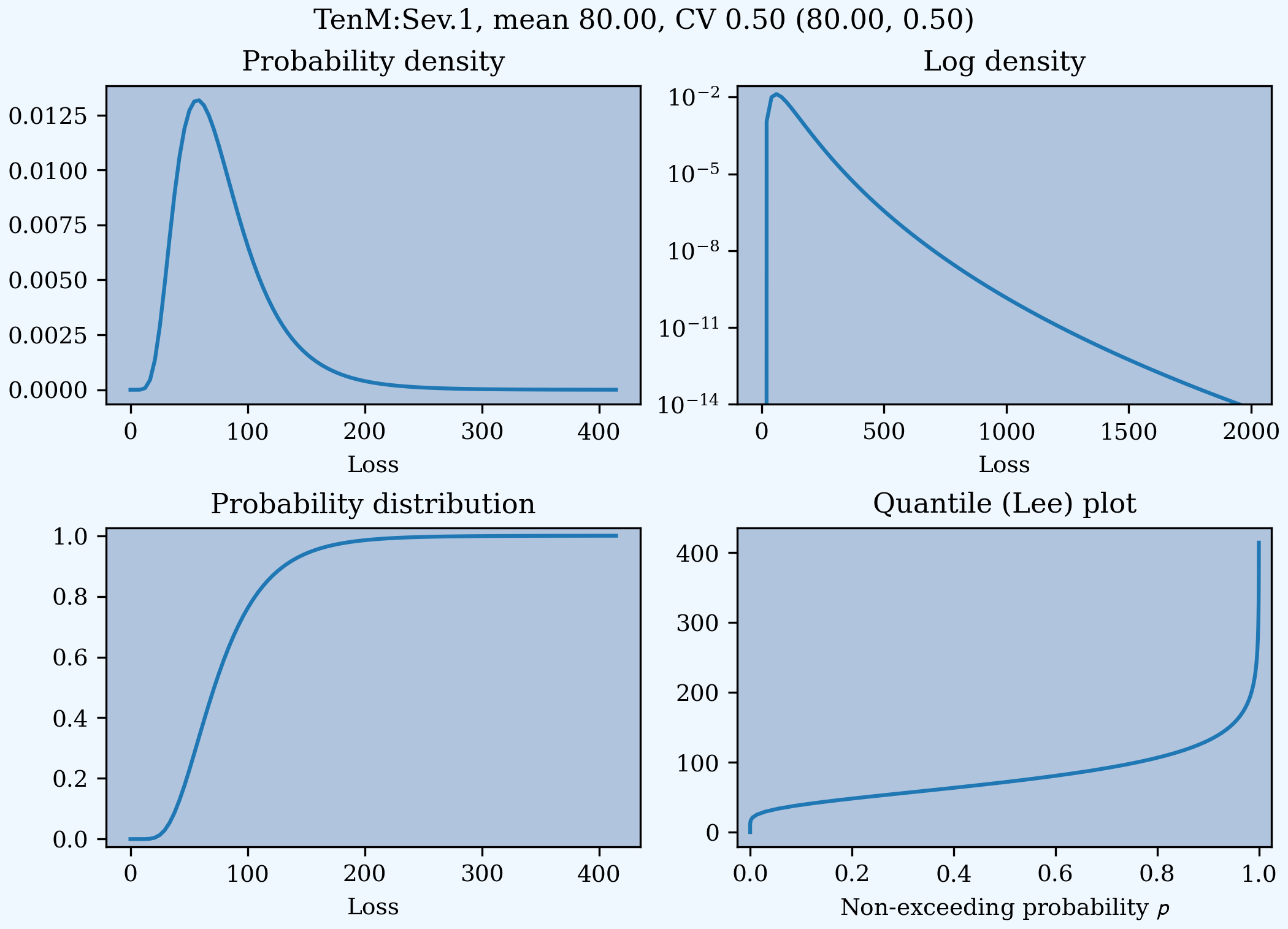

lognorm 80 cv 0.5 results in an unshifted lognormal with mean 80 and CV 0.5.

In [11]: s0 = build(f'sev TenM:Sev.1 '

....: 'lognorm 80 cv .5')

....:

In [12]: mf, vf = s0.fz.stats(); m, v = s0.stats()

In [13]: s0.plot(figsize=(2*3.5, 2*2.45+0.15), layout='AB\nCD');

In [14]: plt.gcf().suptitle(f'{s0.name}, mean {m:.2f}, CV {v**.5/m:.2f} ({mf:.2f}, {vf**.5/mf:.2f})');

In [15]: print(m,v,mf,vf)

80.00000000000004 1599.9999999999936 80.00000000000001 1600.0000000000002

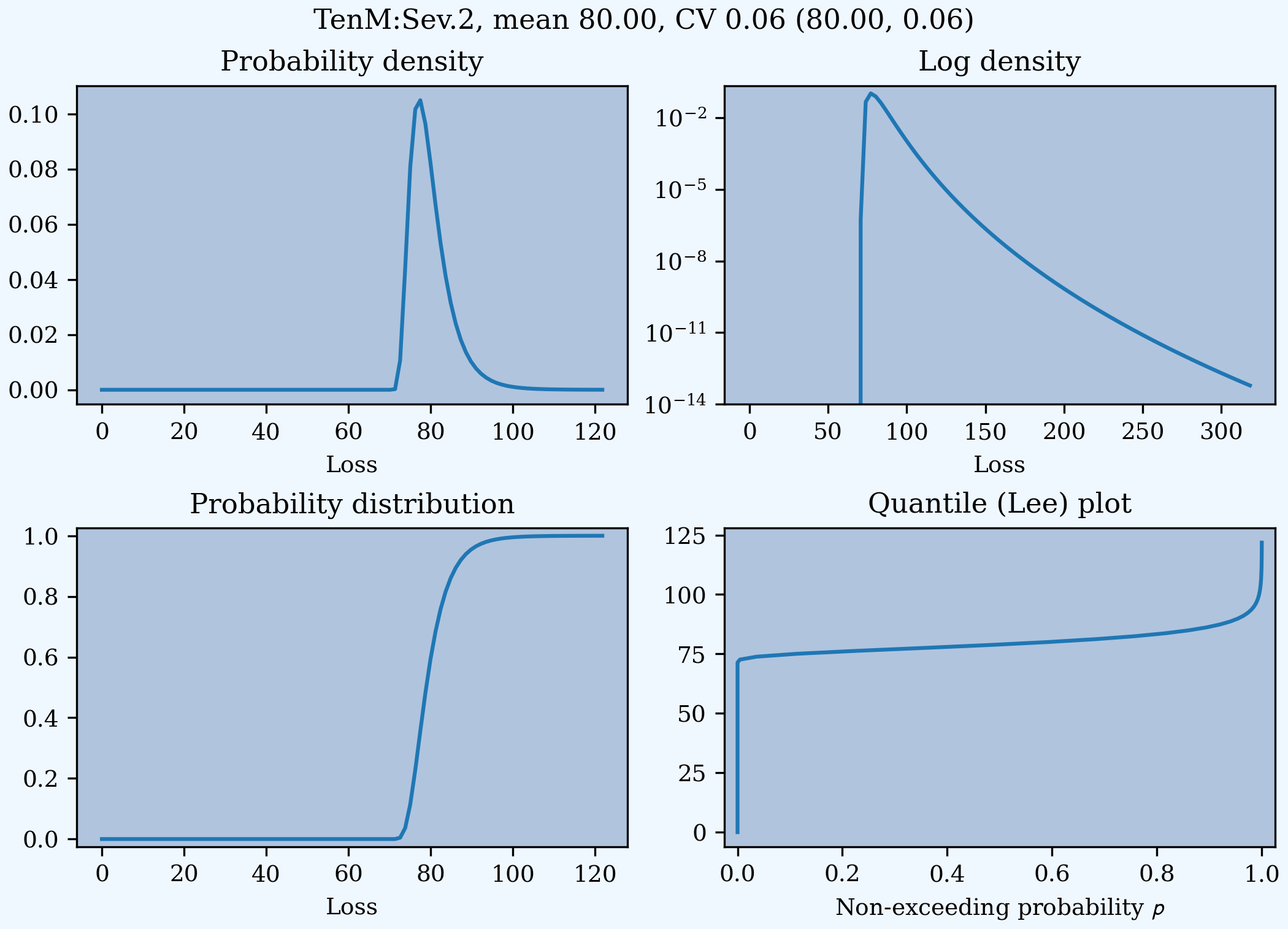

Combining scaling, shifts, and mean/cv entry like so 10 * lognorm 1 cv 0.5 + 70 results in a distribution with mean 10 * 1 + 70 = 80, a standard deviation of 10 * 0.5 = 5, and a cv of 5 / 80.

In [16]: s1 = build(f'sev TenM:Sev.2 '

....: '10 * lognorm 1 cv .5 + 70')

....:

In [17]: mf, vf = s1.fz.stats(); m, v = s1.stats()

In [18]: s1.plot(figsize=(2*3.5, 2*2.45+0.15), layout='AB\nCD');

In [19]: plt.gcf().suptitle(f'{s1.name}, mean {m:.2f}, CV {v**.5/m:.2f} ({mf:.2f}, {vf**.5/mf:.2f})');

In [20]: print(m,v,mf,vf)

80.00000002527862 25.000006201477845 80.0 25.000000000000004

Examples.

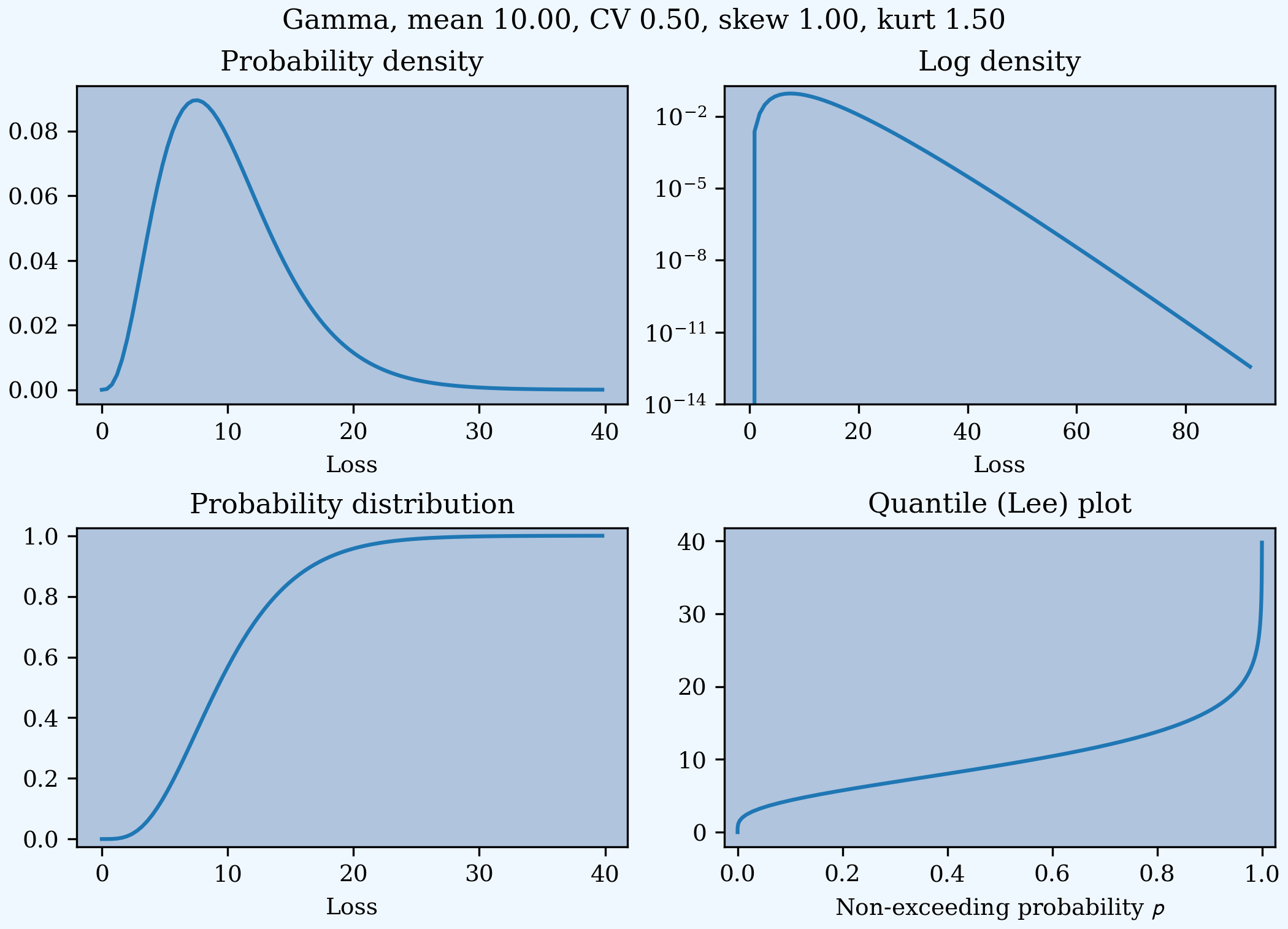

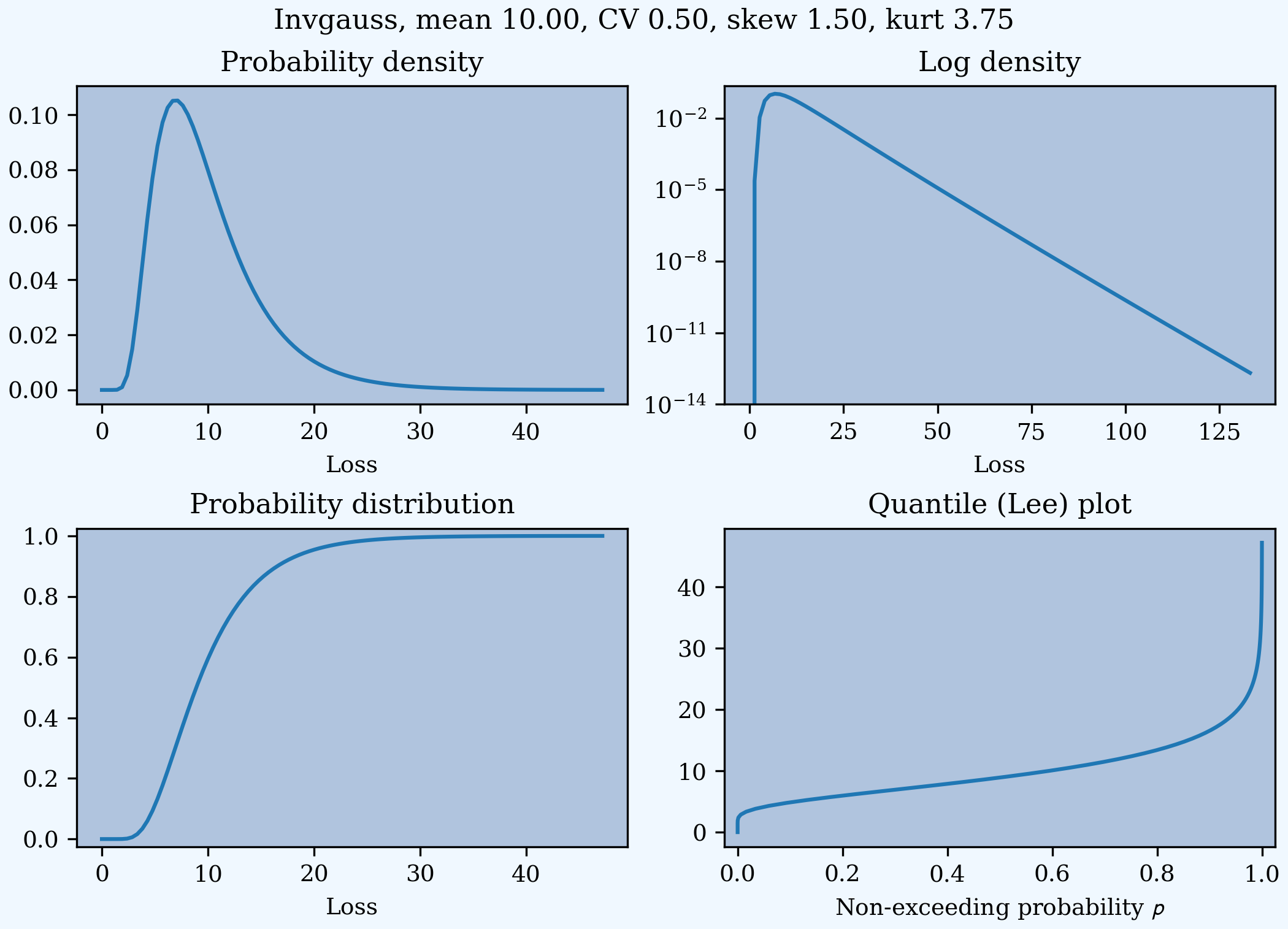

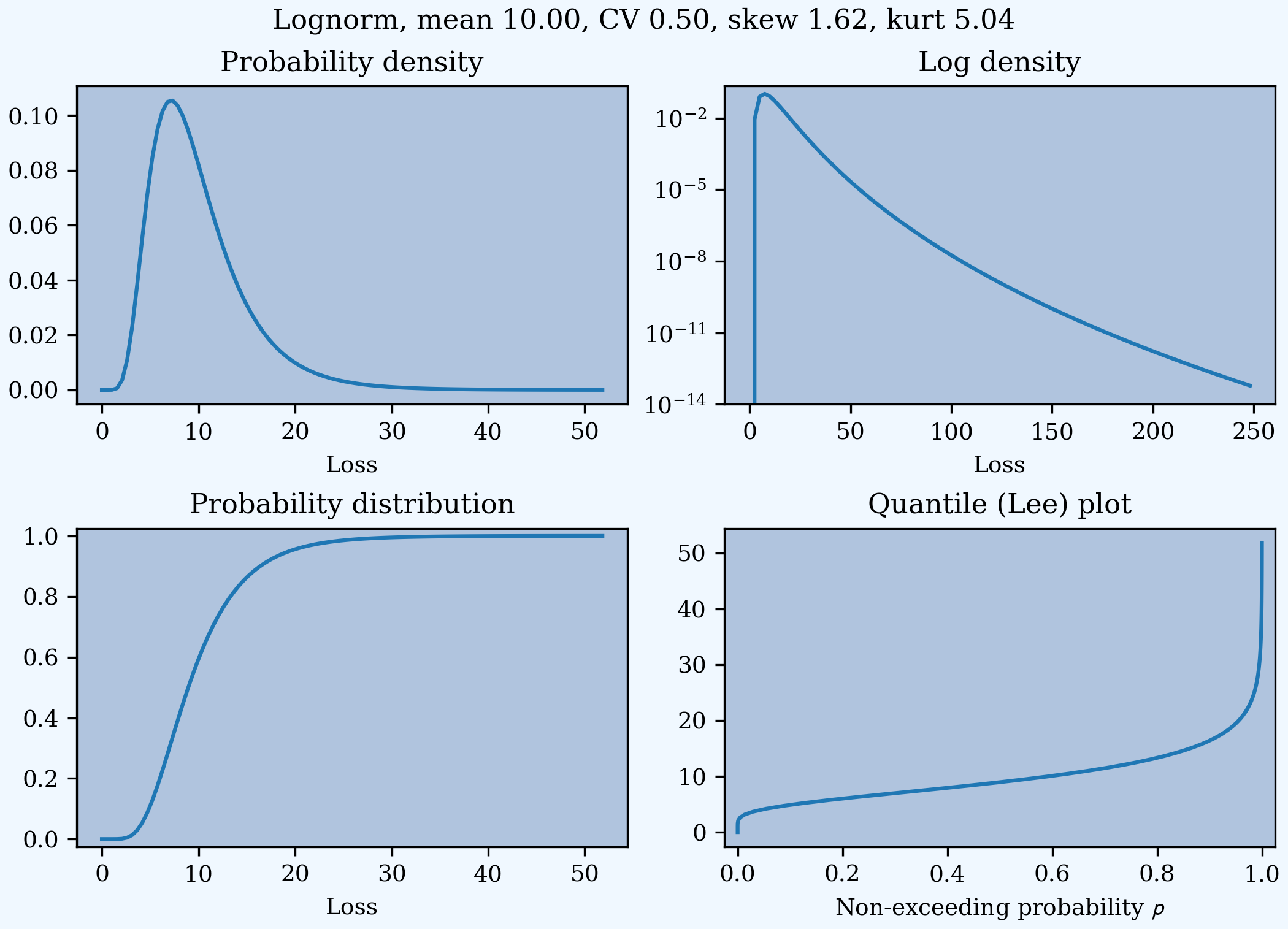

This example compares the shapes of gamma, inverse Gaussian, lognormal, and inverse gamma severities with the same mean and CV. First, a short function to create the examples.

In [21]: def plot_example(dist_name):

....: s = build(f'sev TenM:{dist_name.title()} '

....: f'{dist_name} 10 cv .5')

....: m, v, sk, k = s.fz.stats('mvsk')

....: s.plot(figsize=(2*3.5, 2*2.45+0.15), layout='AB\nCD')

....: plt.gcf().suptitle(f'{dist_name.title()}, mean {m:.2f}, '

....: f'CV {v**.5/m:.2f}, skew {sk:.2f}, kurt {k:.2f}')

....:

Execute on the desired distributions.

In [22]: plot_example('gamma')

In [23]: plot_example('invgauss')

In [24]: plot_example('lognorm')

In [25]: plot_example('invgamma')

Examples.

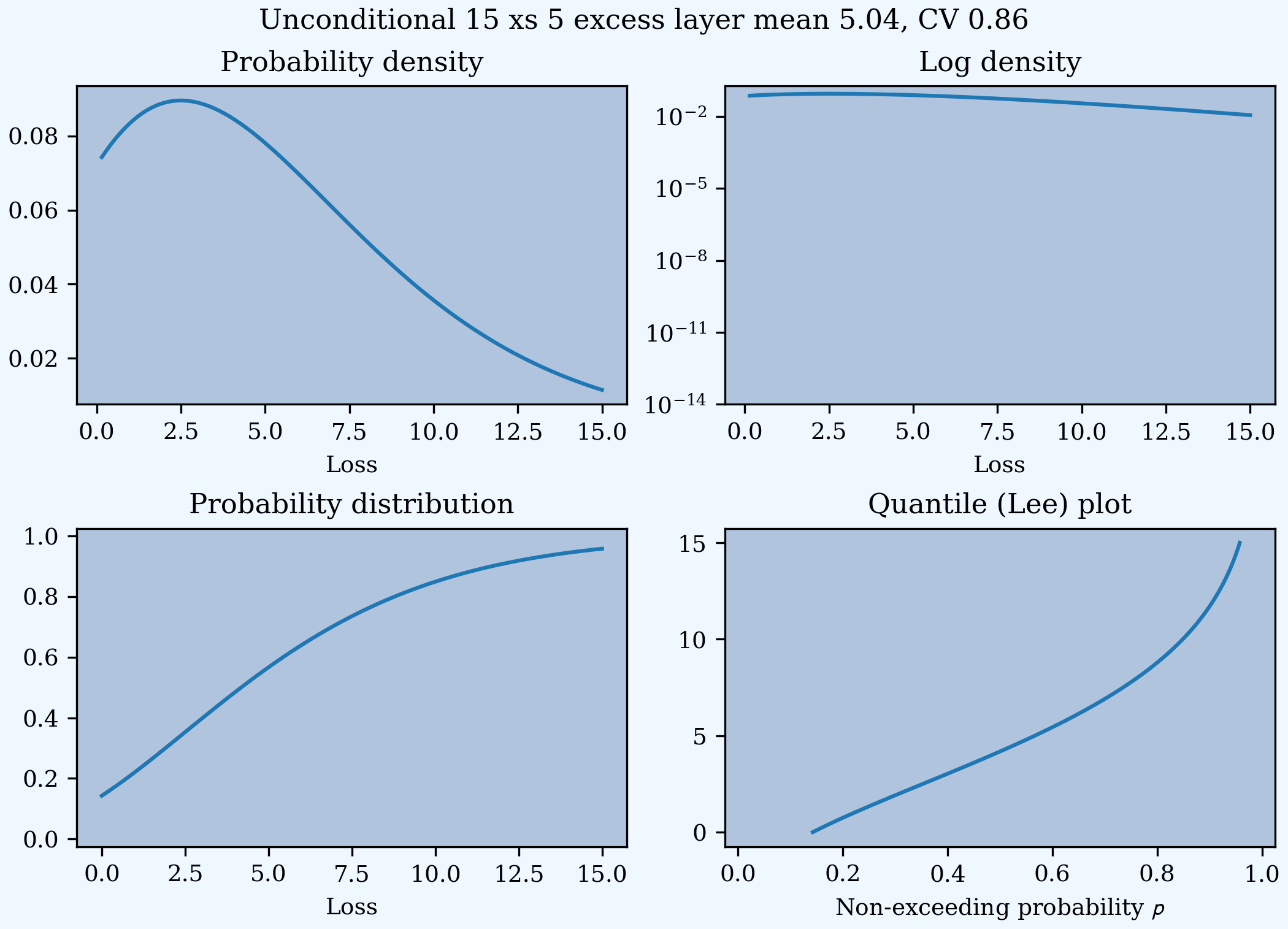

This example show the impact of adding a limit and attachment.

Limits and attachments determine exposure in DecL and they belong to the Aggregate specification. DecL cannot be used to set the limit and attachment of a Severity object. One way to apply them is to create an aggregate with a fixed frequency of one claim. By default, the severity is conditional on a loss to the layer.

In [26]: limit, attach = 15, 5

In [27]: s2 = build(f'agg TenM:SevLayer 1 claim {limit} xs {attach} sev gamma 10 cv .5 fixed')

In [28]: m, v, sk, k = s2.sevs[0].fz.stats('mvsk')

In [29]: s2.sevs[0].plot(n=401, figsize=(2*3.5, 2*2.45+0.3), layout='AB\nCD')

In [30]: plt.gcf().suptitle(f'Ground-up severity\nGround-up gamma mean {m:.2f}, CV {v**0.5/m:.2f}, skew {sk:.2f}, kurt {k:.2f}\n'

....: f'{limit} xs {attach} excess layer mean {s2.est_m:.2f}, CV {s2.est_cv:.2f}, skew {s2.est_skew:.2f}, kurt {k:.2f}');

....:

A Severity can be created directly using args and kwargs. Here is an example. It also shows the impact of making the severity unconditional (on a loss to the layer). Start by creating the conditional (default) severity and plotting it.

In [31]: from aggregate import Severity

In [32]: s3 = Severity('gamma', attach, limit, 10, 0.5)

In [33]: s3.plot(n=401, figsize=(2*3.5, 2*2.45+0.15), layout='AB\nCD')

In [34]: m, v = s3.stats()

In [35]: plt.gcf().suptitle(f'{limit} xs {attach} excess layer mean {m:.2f}, CV {v**.5/m:.2f}');

Next, create an unconditional version. The lower pdf is scaled down by the probability of attaching the layer, and the left end of the cdf shifted up by the probability of not attaching the layer. These probabilities are given by the underlying fz object’s sf and cdf.

In [36]: s4 = Severity('gamma', attach, limit, 10, 0.5, sev_conditional=False)

In [37]: s4.plot(figsize=(2*3.5, 2*2.45+0.15), layout='AB\nCD')

In [38]: m, v = s4.stats()

In [39]: plt.gcf().suptitle(f'Unconditional {limit} xs {attach} excess layer mean {m:.2f}, CV {v**.5/m:.2f}');

In [40]: print(f'Probability of attaching layer {s4.fz.cdf(attach):.3f}')

Probability of attaching layer 0.143

Although Severity accepts a weight argument, it does not actually support weighted severities. It models only one component. Aggregate handles weighted severities by creating a separate Severity for each component.

2.3.5. The Aggregate Class

2.3.5.1. Creating an Aggregate Distribution

Aggregate objects can be created in three ways:

Generally, they are created using DecL by

Underwriter.build(), as shown in Object Creation Using DecL and build().Objects in the knowledge can be created by name.

Advanced users and programmers can create

Aggregateobjects directly usingkwargs, see Aggregate Class.

Example.

This example uses build() to make an Aggregate with a Poisson frequency, mean 5, and gamma severity with mean 10 and CV 1 . It includes more discussion than the example above. The line breaks improve readability but are cosmetic.

In [41]: a02 = build('agg TenM:02 '

....: '5 claims '

....: 'sev gamma 10 cv 1 '

....: 'poisson')

....:

In [42]: qd(a02)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 5 0.44721 0.44721

Sev 10 10 -2.5431e-08 1 1 2 2

Agg 50 50 -2.5432e-08 0.63246 0.63246 0.94868 0.94868

log2 = 16, bandwidth = 1/128, validation: not unreasonable.

qd displays the dataframe a.describe. This example fails the aliasing validation test because the aggregate mean error is suspiciously greater than the severity. (Run with logger level 20 for more diagnostics.) However, it passes both the severity mean and aggregate mean tests.

2.3.5.2. Aggregate Quick Diagnostics

The quick display reports a set of quick diagnostics, showing

Exact

E[X]and estimatedEst E[X]frequency, severity, and aggregate statistics.Relative errors

Err E[X]for the means.Coefficient of variation

CV(X)and estimated CV,Est CV(X)Skewness

Skew(X)and estimated skewness,Est Skew(X)

The line below the table shows the (log to base 2) of the number of buckets used, log2 and the bucket size bs used in discretization.

These statistics make it easy to see if the numerical estimation is invalid. Look for a small error in the mean and close second (CV) and third (skew) moments.

The last item validation: not unreasonable shows the model did not fail any tests. The test should be interpreted like a null hypothesis; you expect it to be True and are worried when it is False.

In this case, the aggregate mean error is too high because the discretization bucket size bs is too small. Update with a larger bucket.

In [43]: a02.update(bs=1/128)

In [44]: qd(a02)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 5 0.44721 0.44721

Sev 10 10 -2.5431e-08 1 1 2 2

Agg 50 50 -2.5432e-08 0.63246 0.63246 0.94868 0.94868

log2 = 16, bandwidth = 1/128, validation: not unreasonable.

2.3.5.3. Aggregate Algorithm in Detail

Here’s the aggregate FFT convolution algorithm stripped down to bare essentials and coded in raw Python to show you what happens behind the curtain. The algorithm steps are:

Inputs

Severity distribution cdf. Use

scipy.stats.Frequency distribution probability generating function. For a Poisson with mean \(\lambda\) the PGF is \(\mathscr P(z) = \exp(\lambda(z - 1))\).

The bucket size \(b\). Use the value

simple.bs.The number of buckets \(n=2^{log_2}\). Use the default

log2=16found insimple.log2.A padding parameter, equal to 1 by default, from

simple.padding.

Discretize the severity cdf.

Apply the FFT to discrete severity with padding to size

2**(log2 + padding).Apply the frequency pgf to the FFT.

Apply the inverse FFT to create is a discretized version of the aggregate distribution and output it.

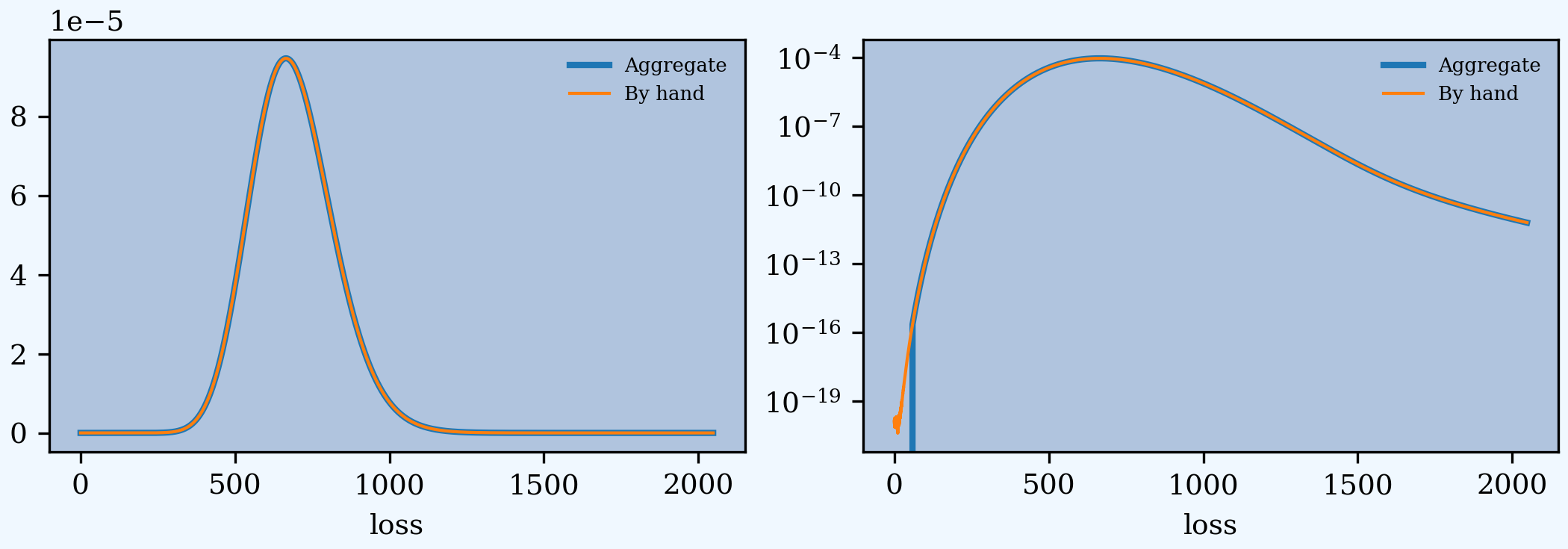

Let’s recreate the following simple example. The variable names for the means and shape are for clarity. sev_shape is \(\sigma\) for a lognormal.

In [45]: from aggregate import build, qd

In [46]: en = 50

In [47]: sev_scale = 10

In [48]: sev_shape = 0.8

In [49]: simple = build('agg Simple '

....: f'{en} claims '

....: f'sev {sev_scale} * lognorm {sev_shape} '

....: 'poisson')

....:

In [50]: qd(simple)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 50 0.14142 0.14142

Sev 13.771 13.771 -2.4063e-09 0.94683 0.94683 3.6893 3.6892

Agg 688.56 688.56 -9.4705e-09 0.19476 0.19476 0.36935 0.36933

log2 = 16, bandwidth = 1/32, validation: not unreasonable.

The next few lines of code implement the FFT convolution algorithm. Start by importing the probability distribution and FFT routines. rfft and irfft take the FFT and inverse FFT of real input.

In [51]: import numpy as np

In [52]: from scipy.fft import rfft, irfft

In [53]: import scipy.stats as ss

Pull parameters from simple to match calculations, step 1. n_pad is the length of the padded vector used in the convolution to manage aliasing.

In [54]: bs = simple.bs

In [55]: log2 = simple.log2

In [56]: padding = simple.padding

In [57]: n = 1 << log2

In [58]: n_pad = 1 << (log2 + padding)

In [59]: sev = ss.lognorm(sev_shape, scale=sev_scale)

Use the round method and the survival function to discretize, completing step 2.

In [60]: xs = np.arange(0, (n + 1) * bs, bs)

In [61]: discrete_sev = -np.diff(sev.sf(xs - bs / 2))

The next line of code carries out algorithm steps 3, 4, and 5!

All the magic happens here. The forward FFT adds padding, but the answer must be unpadded manually, with the final [:n].

In [62]: agg = irfft( np.exp( en * (rfft(discrete_sev, n_pad) - 1) ) )[:n]

Plots to compare the two approaches. They are spot on!

In [63]: import matplotlib.pyplot as plt

In [64]: fig, axs = plt.subplots(1, 2, figsize=(2 * 3.5, 2.45),

....: constrained_layout=True); \

....: ax0, ax1 = axs.flat; \

....: simple.density_df.p_total.plot(lw=2, label='Aggregate', ax=ax0); \

....: ax0.plot(xs[:-1], agg, lw=1, label='By hand'); \

....: ax0.legend(); \

....: simple.density_df.p_total.plot(lw=2, label='Aggregate', ax=ax1); \

....: ax1.plot(xs[:-1], agg, lw=1, label='By hand'); \

....: ax1.legend();

....:

In [65]: ax1.set(yscale='log');

The very slight difference for small loss values arises because build removes numerical fuzz, setting values below machine epsilon (about 2e-16) to zero, explaining why the blue aggregate line drops off vertically on the left.

2.3.5.4. Basic Probability Functions

An Aggregate object acts like a discrete probability distribution. There are properties for the aggregate and severity mean, standard deviation, coefficient of variation, and skewness, both computed exactly and numerically estimated.

In [66]: print(a02.agg_m, a02.agg_sd, a02.agg_cv, a02.agg_skew)

50.0 31.622776601683793 0.6324555320336759 0.9486832980505139

In [67]: print(a02.est_m, a02.est_sd, a02.est_cv, a02.est_skew)

49.9999987284203 31.622777003581923 0.6324555561559914 0.9486832857144013

In [68]: print(a02.sev_m, a02.sev_sd, a02.sev_cv, a02.sev_skew)

10.0 10.0 1.0 2.0

In [69]: print(a02.est_sev_m, a02.est_sev_sd, a02.est_sev_cv, a02.est_sev_skew)

9.99999974568674 10.000000508623474 1.0000000762936754 1.9999996947979108

They have probability mass, cumulative distribution, survival, and quantile (inverse of distribution) functions.

In [70]: a02.pmf(60), a02.cdf(50), a02.sf(60), a02.q(a02.cdf(60)), a02.q(0.5)

Out[70]:

(np.float64(7.923645058165983e-05),

np.float64(0.5639640504996987),

np.float64(0.3244107518264777),

np.float64(60.0),

np.float64(44.90625))

The pdf, cdf, and sf for the underlying severity are also available.

In [71]: a02.sev.pdf(60), a02.sev.cdf(50), a02.sev.sf(60)

Out[71]:

(np.float64(0.00024787521766663585),

np.float64(0.9932620530009145),

np.float64(0.002478752176666357))

Note

Aggregate and Portfolio objects need to be updated after they have been created. Updating builds out discrete numerical approximations, analogous to simulation. By default, build() handles updating automatically.

Warning

Always use bucket sizes that have an exact binary representation (integers, 1/2, 1/4, 1/8, etc.) Never use 0.1 or 0.2 or other numbers that do not have an exact float representation, see REF.

2.3.5.5. Mixtures

An Aggregate can have a mixed severity. The mixture can include different distributions, parameters, shifts, and locations.

In [72]: a03 = build('agg TenM:03 '

....: '25 claims '

....: 'sev [gamma lognorm invgamma] [5 10 10] cv [0.5 0.75 1.5] '

....: '+ [0 10 20] wts [.5 .25 .25] '

....: 'mixed gamma 0.5'

....: , bs=1/16)

....:

In [73]: qd(a03)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 25 0.53852 1.0028

Sev 15 14.999 -3.7467e-05 0.90907 0.89065 inf 9.9075

Agg 375 374.99 -3.8034e-05 0.56838 0.5672 inf 1.0698

log2 = 16, bandwidth = 1/16, validation: fails sev cv, agg cv.

An Aggregate can model multiple units at once, and allow them to share mixing variables. This induces correlation between the components, see the report dataframe. All parts of the specification can vary, including limits and attachments (not shown). This case differentiated from a mixed severity by having no weights.

In [74]: a04 = build('agg TenM:04 '

....: '[500 250 100] premium at [.8 .7 .5] lr '

....: 'sev [gamma lognorm invgamma] [5 10 10] cv [0.5 0.75 1.5] '

....: 'mixed gamma 0.5'

....: , bs=1/8)

....:

In [75]: qd(a04)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 102.5 0.50966 1.0002

Sev 6.0976 6.0975 -6.5732e-06 0.89437 0.87819 inf 43.583

Agg 625 625 -6.6355e-06 0.51726 0.51699 inf 1.0208

log2 = 16, bandwidth = 1/8, validation: fails sev cv.

2.3.5.6. Accessing Severity in an Aggregate

The attribute Aggregate.sevs is an array of the Severity

objects. Usually, it contains only one distribution but when severity is a

mixture it contains one for each mixture component. It can be iterated over.

Each Severity object wraps a scipy.stats continuous random

variable called fz that represents ground-up severity. The args are its

shape variable(s) and kwds its scale and location variables. This is

most interesting when the object has a mixed severity.

In [76]: for s in a03.sevs:

....: print(s.sev_name, s.fz.args, s.fz.kwds)

....:

gamma (np.float64(4.0),) {'scale': np.float64(1.25), 'loc': np.float64(0.0)}

lognorm (np.float64(0.6680472308365776),) {'scale': np.float64(8.0), 'loc': np.float64(10.0)}

invgamma (np.float64(2.4444444444444446),) {'scale': np.float64(14.444444444444446), 'loc': np.float64(20.0)}

The property a03.sev is a namedtuple exposing the exact weighted pdf,

cdf, and sf of the underlying Severity objects.

In [77]: a03.sev.pdf(20), a03.sev.cdf(20), a03.sev.sf(20)

Out[77]:

(np.float64(0.014150102336136361),

np.float64(0.657658211871339),

np.float64(0.342341788128661))

The component weights are proportional to a03.en and a03.sev.cdf is computed as

In [78]: (np.array([s.cdf(20) for s in a03.sevs]) * a03.en).sum() / a03.en.sum()

Out[78]: np.float64(0.6576582118713391)

The following are equal using the defaut discretization method.

In [79]: a03.density_df.loc[20, 'F_sev'], a03.sev.cdf(20 + a03.bs/2)

Out[79]: (np.float64(0.658099359833043), np.float64(0.6580993598330431))

2.3.5.7. Reinsurance

Aggregate objects can apply per occurrence and aggregate reinsurance using clauses

occurrence net of [limit] xs ]attach]occurrence net of [pct] so [limit] xs [attach], wheresostands for “share of”occurrence ceded to [limit] xs ]attach]and so forth.

Examples.

Gross distribution: a triangular aggregate created as the sum of two uniform distribution on 1, 2,…, 10.

In [80]: a05g = build('agg TenM:05g dfreq [2] dsev [1:10]')

In [81]: qd(a05g)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2 0

Sev 5.5 5.5 0 0.52223 0.52223 0 0

Agg 11 11 -3.3307e-16 0.36927 0.36927 0 -6.1064e-14

log2 = 6, bandwidth = 1, validation: not unreasonable.

Apply 3 xs 7 occurrence reinsurance to cap individual losses at 7. a05no is the net of occurrence distribution.

In [82]: a05no = build('agg TenM:05no dfreq [2] dsev [1:10] '

....: 'occurrence net of 3 xs 7')

....:

In [83]: qd(a05no)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2 0

Sev 5.5 4.9 -0.10909 0.52223 0.44197 0 -0.52103

Agg 11 9.8 -0.10909 0.36927 0.31252 0 -0.36842

log2 = 6, bandwidth = 1, validation: n/a, reinsurance.

Warning

The describe dataframe always reports gross analytic statistics (E[X], CV(X), Skew(X)) and the requested net or ceded estimated statistics (Est E[X], Est CV(X), Est Skew(X)). Look at the gross portfolio first to check computational accuracy. Net and ceded “error” report the difference to analytic gross.

Add an aggregate 4 xs 8 reinsurance cover on the net of occurrence distribution. a05n is the final net distribution.

In [84]: a05n = build('agg TenM:05n dfreq [2] dsev [1:10] '

....: 'occurrence net of 3 xs 7 '

....: 'aggregate net of 4 xs 8')

....:

In [85]: qd(a05n)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2 0

Sev 5.5 4.9 -0.10909 0.52223 0.44197 0 -0.52103

Agg 11 7.84 -0.28727 0.36927 0.20781 0 -1.2676

log2 = 6, bandwidth = 1, validation: n/a, reinsurance.

See The plot() Method for plots of the different distributions.

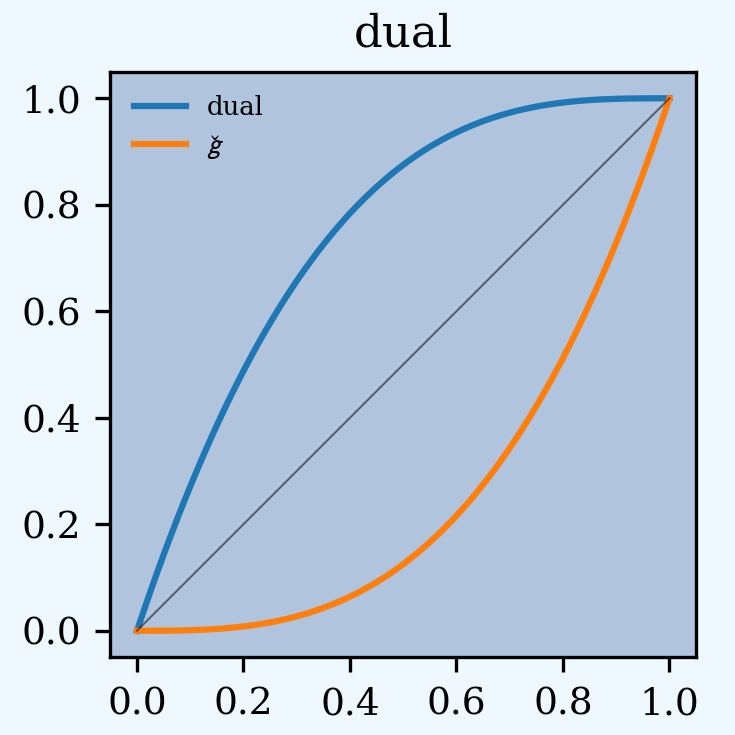

2.3.6. The Distortion Class

See Distortions and Spectral Risk Measures and PIR Chapter 10.5 for more information about distortions.

A Distortion can be created using DecL.

It object has methods for g, the distortion function, along with its dual g_dual(s)=1-g(1-s) and inverse g_inv. The plot() method shows g (above the diagonal) and g_inv (below).

In [86]: d06 = build('distortion TenM:06 dual 3')

In [87]: qd(d06.g(.2), d06.g_inv(.2), d06.g_dual(0.2),

....: d06.g(.8), d06.g_inv(.992), d06)

....:

0.488

0.071682

0.008

0.992

0.8

dual

In [88]: d06.plot();

The Distortion class can create distortions from a number of parametric families.

In [89]: from aggregate import Distortion

In [90]: Distortion.available_distortions(False, False)

Out[90]:

('ph',

'wang',

'cll',

'lep',

'ly',

'clin',

'dual',

'ccoc',

'tvar',

'bitvar',

'wtdtvar',

'convex',

'tt',

'beta')

Run the command:

Distortion.test()

for graphs of samples from each available family. tt is not a distortion because it is not concave. It is included for historical reasons.

2.3.7. The Portfolio Class

A Portfolio object models a portfolio (book, block) of units (accounts, lines, business units, regions, profit centers), each represented as an Aggregate. It uses FFTs to convolve (add) the unit distributions. By default, all the units are assumed to be independent, though there are ways to adjust this. REF. The independence assumption is not as bad as it may appear; its effect can be ameliorated by selecting units carefully and sharing mixing variables appropriately (see REF for further discussion).

Portfolio objects have all of the attributes and methods of a Aggregate and add methods for pricing and allocation to units.

The DecL for a portfolio is simply:

port NAME AGG1 <AGG2> <AGG3> ...

where AGG1 is an aggregate specification. Portfolios can have one or more units. The DecL can be split over multiple lines if each aggregate begins on a new line and is indented by a tab (like a Python function).

Example.

Here is a three-unit portfolio built using a DecL program. The line breaks and horizontal spacing are cosmetic since Python just concatenates the input.

In [91]: p07 = build('port TenM:07 '

....: 'agg A '

....: '100 claims '

....: '10000 xs 0 '

....: 'sev lognorm 100 cv 1.25 '

....: 'poisson '

....: 'agg B '

....: '150 claims '

....: '2500 xs 5 '

....: 'sev lognorm 50 cv 0.9 '

....: 'mixed gamma .6 '

....: 'agg Cat '

....: '2 claims '

....: '1e5 xs 0 '

....: 'sev 500 * pareto 1.8 - 500 '

....: 'poisson'

....: , approximation='exact', padding=2)

....:

In [92]: qd(p07)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

A Freq 100 0.1 0.1

Sev 100 100 -1.1973e-08 1.2498 1.2498 5.6619 5.6617

Agg 10000 10000 -1.1973e-08 0.16006 0.16007 0.4082 0.40819

B Freq 150 0.60553 1.2001

Sev 45.213 45.212 -1.2825e-05 0.99517 0.99528 3.4345 3.4335

Agg 6781.9 6781.8 -1.2825e-05 0.61096 0.61096 1.2009 1.2009

Cat Freq 2 0.70711 0.70711

Sev 616.02 616.02 -9.7399e-07 3.1331 3.1331 23.278 23.278

Agg 1232 1232 -4.3508e-06 2.3256 2.3254 14.837 14.828

total Freq 252 0.36266 1.1783

Sev 71.484 71.483 -4.9016e-06 2.7998 172.51

Agg 18014 18013 -2.6963e-05 0.29343 0.29322 2.9528 2.925

log2 = 16, bandwidth = 2, validation: not unreasonable.

The portfolio units are called A, B and Cat. Printing using qd shows p07.describe, which concatenates each unit’s describe and adds the same statistics for the total.

Unit A has 100 (expected) claims, each pulled from a lognormal distribution with mean of 30 and coefficient of variation 1.25 within the layer 100 xs 0 (i.e., losses are limited at 100). The frequency distribution is Poisson.

Unit B is similar.

The Cat unit is has expected frequency of 2 claims from the indicated limit, with severity given by a Pareto distribution with shape parameter 1.8, scale 500, shifted left by 500. This corresponds to the usual Pareto with survival function \(S(x) = (500 / (500 + x))^{1.8} = (1 + x / 500)^{-1.8}\) for \(x \ge 0\).

The portfolio total (i.e., the sum of the units) is computed using FFTs to convolve (add) the unit’s aggregate distributions. All computations use the same discretization bucket size; here the bucket-size bs=2. See For Portfolio Objects.

A Portfolio object acts like a discrete probability distribution, the same as an Aggregate. There are properties for the mean, standard deviation, coefficient of variation, and skewness, both computed exactly and numerically estimated.

In [93]: print(p07.agg_m, p07.agg_sd, p07.agg_cv, p07.agg_skew)

18013.930242377224 5285.799078302742 0.2934284194055587 2.952768695357267

In [94]: print(p07.est_m, p07.est_sd, p07.est_cv, p07.est_skew)

18013.444535982344 5281.917148506572 0.29322082947299716 2.924970410288626

They have probability mass, cumulative distribution, survival, and quantile (inverse of distribution) functions.

In [95]: p07.pmf(12000), p07.cdf(11000), p07.sf(12000), p07.q(p07.cdf(12000)), p07.q(0.5)

Out[95]:

(np.float64(9.808446441348987e-05),

np.float64(0.031240713459622396),

np.float64(0.9300376004823764),

np.float64(12000.0),

np.float64(17176.0))

The names of the units in a Portfolio are in a list called p07.unit_names or p07.unit_names_ex including total.

The Aggregate objects in the Portfolio can be iterated over.

In [96]: for u in p07:

....: print(u.name, u.agg_m, u.est_m)

....:

A 9999.982520635807 9999.982400908266

B 6781.90965866976 6781.8226809277885

Cat 1232.038063071656 1232.0327026844775

2.3.8. Estimating Bucket Size for Discretization

Selecting an appropriate bucket size bs is critical to obtaining accurate results. This is a hard problem that may have hindered broad adoption of FFT-based methods.

See Numerical Methods and FFT Convolution for further discussion.

2.3.8.1. Hyper-parameters log2 and bs

The hyper-parameters log2 and bs control numerical calculations.

log2 equals the log to base 2 of the number of buckets used and bs

equals the bucket size. These values are printed by qd.

2.3.8.2. Estimating and Testing bs For Aggregate Objects

For an Aggregate, recommend_bucket() uses a shifted lognormal

method of moments fit and takes the recommend_p percentile as the

right-hand end of the discretization. By default recommend_p=0.999, but

for thick tailed distributions it may be necessary to use a value closer to

1. recommend_bucket() also considers any limits: ideally limits are

multiples of the bucket size.

The recommended value of bs should rounded up to a binary fraction

(denominator is a power of 2) using utilities.round_bucket().

Aggregate also includes two functions for assessing bs,

one based on the overall error and one based on looking at each severity

component.

Aggregate.aggregate_error_analysis() updates the object at a range of

different bs values and reports the total absolute (strictly, signed

absolute error) and relative error as well as an upper bound bs/2 on

the absolute value of the discretization error. log2 must be input and,

optionally, the log base 2 of the smallest bucket to model. It then models

six doublings of the input bucket. If no bucket is input, it models three

doublings up and down from the rounded recommend_bucket() suggestion.

The output table shows:

The actual

(agg, m)and estimated(est, m)means, from thedescribedataframe.The implied absolute

(abs, m)and relative(rel, m)errors in the mean.(rel, h)shows the maximum relative severity discretization error, which equalsbs / 2divided by the average severity.(rel, total), equal to the sum of(rel, h)andrel m.

Thick tailed distributions can favor a large bucket size without regard to the impact on discretization; accounting for the impact of bs / 2 is a countervailing force.

In [97]: qd(a04.aggregate_error_analysis(16), sparsify=False, col_space=9)

view agg est abs rel rel rel

stat m m m m h total

bs

0.03125 625 624.71 -0.28786 -0.00046057 0.0025625 -0.0030231

0.06250 625 624.99 -0.011699 -1.8718e-05 0.005125 -0.0051437

0.12500 625 625 -0.0041472 -6.6355e-06 0.01025 -0.010257

0.25000 625 625 -0.0015133 -2.4212e-06 0.0205 -0.020502

0.50000 625 625 -0.00050174 -8.0278e-07 0.041 -0.041001

1.00000 625 625 0.0026758 4.2813e-06 0.082 0.082004

2.00000 625 625.14 0.13828 0.00022125 0.164 0.16422

Aggregate.severity_error_analysis() performs a detailed error analysis of each severity component. It reports:

The name, limit, attachment, and truncation point for each severity component.

Sthe probability the component (or total losses) exceed the truncation.sum_pthe sum of discrete probabilities, which can be \(<1\) ifnormalize=False.wtthe weight of the component andenthe corresponding claim count.agg_meanandagg_wtthe aggregate mean contribution from the component (sums to the overall mean), and the each component’s proportion of the total. The loss weight can differ drastically from the count weight.meanandest_meanthe analytic and estimated severity by component and the correspondingabsandrelerror.trunc_errorthe truncation error by component (tail integral) and relative truncation error.The

h_errorbased onbs / 2by component, a (conservative) upper bound on discretization error and the relative error compared to the component mean.h2_adjandrel_h2_adjestimate a second order adjustment to the numerical mean. They give a better idea of the discretization error.

In [98]: qd(a04.severity_error_analysis(), line_width=75)

name limit attachment trunc S sum_p wt en \

0 gamma inf 0 8192 0 1 0.78049 80

1 lognorm inf 0 8192 1.5989e-25 1 0.17073 17.5

2 invgamma inf 0 8192 5.9297e-08 1 0.04878 5

3 total inf 0 8192 8.6388e-08 1 1 102.5

agg_mean agg_wt mean est_mean abs rel \

0 400 0.64 5 5 1.5997e-10 3.1994e-11

1 175 0.28 10 10 -1.6449e-12 -1.6449e-13

2 50 0.08 10 9.9992 -0.00082165 -8.2165e-05

3 625 1 6.0976 6.0975 -4.008e-05 -6.5732e-06

trunc_error rel_trunc_error h_error rel_h_error h2_adj \

0 -0 -0 0.0625 0.0125 5.1607e-09

1 -8.8373e-23 -8.8373e-24 0.0625 0.00625 1.0915e-14

2 -0.00033646 -3.3646e-05 0.0625 0.00625 1.1514e-14

3 -1.6408e-05 -2.6909e-06 0.0625 0.01025 4.0279e-09

rel_h2_adj

0 1.0321e-09

1 1.0915e-15

2 1.1514e-15

3 6.6058e-10

Generally there is either discretization or truncation error. Look for one of them to dominate. Discretization error is solved with a smaller bucket; truncation with a larger. When the two conflict, add more buckets by increasing log2.

2.3.8.3. Estimating and Testing bs For Portfolio Objects

For a Portfolio, the right hand end of the distribution is estimated using the square root of sum of squares (proxy independent sum) of the right hand ends of each unit.

The method port.recommend_bucket() suggests a reasonable bucket size.

In [99]: print(p07.recommend_bucket().iloc[:, [0,3,6,10]])

bs10 bs13 bs16 bs20

line

A 18.545709 2.318214 0.289777 0.018111

B 43.766975 5.470872 0.683859 0.042741

Cat 143.204295 17.900537 2.237567 0.139848

total 205.516978 25.689622 3.211203 0.2007

In [100]: p07.best_bucket(16)

Out[100]: 2

The column bsN corresponds to discretizing with 2**N buckets. The rows show suggested bucket sizes by unit and in total. For example with N=16 (i.e., 65,536 buckets) the suggestion is 2.19. It is best the bucket size is a divisor of any limits or attachment points. best_bucket() takes this into account and suggests 2.

To test bs, run the tests above on each unit.

2.3.9. Methods and Properties Common To Aggregate and Portfolio Classes

Aggregate and Portfolio both have the following methods and properties. See Aggregate Class and Portfolio Class for full lists.

infoanddescribeare dataframes with statistics and other information; they are printed with the object.density_dfa dataframe containing estimated probability distributions and other expected value information.The

statisticsdataframe shows analytically computed mean, variance, CV, and sknewness for each unit and in total.report_dfare dataframe with information to test if the numerical approximations appear valid. Numerically estimated statistics are prefacedest_orempirical.log2andbshyper-parameters that control numerical calculations.speca dictionary containing thekwargsneeded to recreate each object. For example, ifais anAggregateobject, thenAggregate(**a.spec)creates a new copy.spec_exa dictionary that appends hyper-parameters tospecincludinglog2andbs.programthe DecL program used to create the object. Blank if the object has been created directly. (A given object can often be created in different ways by DecL, so there is no obvious reverse mapping from thespec.)renamera dictionary used to rename columns of member dataframes to be more human readable.update()a method to run the numerical calculation of probability distributions.recommend_bucket()to recommend the value ofbs.Common statistical functions including pmf, cdf, sf, the quantile function (value at risk) and tail value at risk.

Statistical functions: pdf, cdf, sf, quantile, value at risk, tail value at risk, and so on.

plot()method to visualize the underlying distributions. Plots the pmf and log pmf functions and the quantile function. All the data is contained indensity_dfand the plots are created usingpandasstandard plotting commands.price()to apply a distortion (spectral) risk measure pricing rule with a variety of capital standards.snap()to round an input number to the index ofdensity_df.approximate()to create an analytic approximation.sample()pulls samples, see Samples from aggregate Object.

2.3.9.1. The info Dataframe

The info dataframe contains information about the frequency and severity stochastic models, how the object was computed, and any reinsurance applied (none in this case).

In [101]: print(a05n.info)

aggregate object name TenM:05n

claim count 2.00

frequency distribution empirical

severity distribution dhistogram, unlimited.

bs 1

log2 6

padding 1

sev_calc discrete

normalize True

approximation exact

validation_eps 0.0001

reinsurance occurrence and aggregate

occurrence reinsurance net of 100% share of 3 xs 7 per occurrence

aggregate reinsurance net of 100% share of 4 xs 8 in the aggregate.

validation n/a, reinsurance

In [102]: print(p07.info)

portfolio object name TenM:07

aggregate objects 3

bs 2

log2 16

padding 2

sev_calc discrete

normalize True

last update 2026-05-18T14:27:53

hash 3ca40f0204cf4b8b

2.3.9.2. The describe Dataframe

The describe dataframe contains gross analytic and estimated (net or ceded) statistics. When there is no reinsurance, comparison of analytic and estimated moments provides a test of computational accuracy (first case). It should always be reviewed after updating. When there is reinsurance, empirical is net (second case).

In [103]: qd(a05g.describe)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Err CV(X) Skew(X) Est Skew(X)

X

Freq 2 NaN NaN 0 NaN NaN NaN NaN

Sev 5.5 5.5 0 0.52223 0.52223 0 0 0

Agg 11 11 -3.3307e-16 0.36927 0.36927 0 0 -6.1064e-14

In [104]: with pd.option_context('display.max_columns', 15):

.....: print(a05n.describe)

.....:

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Err CV(X) Skew(X) Est Skew(X)

X

Freq 2.0 NaN NaN 0.000000 NaN NaN NaN NaN

Sev 5.5 4.90 -0.109091 0.522233 0.441968 -0.153697 0.0 -0.521027

Agg 11.0 7.84 -0.287273 0.369274 0.207810 -0.437247 0.0 -1.267573

In [105]: qd(p07.describe)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Err CV(X) Skew(X) Est Skew(X)

unit X

A Freq 100 NaN NaN 0.1 NaN NaN 0.1 NaN

Sev 100 100 -1.1973e-08 1.2498 1.2498 1.0689e-05 5.6619 5.6617

Agg 10000 10000 -1.1973e-08 0.16006 0.16007 6.5169e-06 0.4082 0.40819

B Freq 150 NaN NaN 0.60553 NaN NaN 1.2001 NaN

Sev 45.213 45.212 -1.2825e-05 0.99517 0.99528 0.00010815 3.4345 3.4335

Agg 6781.9 6781.8 -1.2825e-05 0.61096 0.61096 1.913e-06 1.2009 1.2009

Cat Freq 2 NaN NaN 0.70711 NaN NaN 0.70711 NaN

Sev 616.02 616.02 -9.7399e-07 3.1331 3.1331 1.118e-06 23.278 23.278

Agg 1232 1232 -4.3508e-06 2.3256 2.3254 -7.109e-05 14.837 14.828

total Freq 252 NaN NaN 0.36266 NaN NaN 1.1783 NaN

Sev 71.484 71.483 -4.9016e-06 2.7998 NaN NaN 172.51 NaN

Agg 18014 18013 -2.6963e-05 0.29343 0.29322 -0.00070746 2.9528 2.925

Printing the object using qd add log2, bs, and validation information.

2.3.9.3. The density_df Dataframe

The density_df dataframe contains a wealth of information. It has 2**log2 rows and is indexed by the outcomes, all multiples of bs. Columns containing p are the probability mass function, of the aggregate or severity.

the aggregate and severity pmf (called

pand duplicated asp_totalfor consistency withPortfolioobjects), log pmf, cdf and sfthe aggregate lev (duplicated as

exa)exlea(less than or equal toa) which equals \(\mathsf E[X\mid X\le a]\) as a function oflossexgta(greater than) which equals \(\mathsf E[X\mid X > a]\)

In an Aggregate, p and p_total are identical, the latter included for consistency with Portfolio output. F and S are the cdf and sf (survival function). lev and exa are identical and equal the limited expected value at the loss level. Here are the first five rows.

In [106]: print(a05g.density_df.shape)

(64, 17)

In [107]: print(a05g.density_df.columns)

Index(['loss', 'p_total', 'p', 'p_sev', 'log_p', 'log_p_sev', 'F', 'F_sev', 'S', 'S_sev', 'lev', 'exa', 'exlea', 'e',

'epd', 'exgta', 'exeqa'],

dtype='object')

In [108]: with pd.option_context('display.max_columns', a05g.density_df.shape[1]):

.....: print(a05g.density_df.head())

.....:

loss p_total p p_sev log_p log_p_sev F F_sev S S_sev lev exa exlea e epd \

loss

0.0 0.0 0.00 0.00 0.0 -inf -inf 0.00 0.0 1.00 1.0 0.00 0.00 NaN 11.0 1.000000

1.0 1.0 0.00 0.00 0.1 -inf -2.302585 0.00 0.1 1.00 0.9 1.00 1.00 NaN 11.0 0.909091

2.0 2.0 0.01 0.01 0.1 -4.605170 -2.302585 0.01 0.2 0.99 0.8 2.00 2.00 2.000000 11.0 0.818182

3.0 3.0 0.02 0.02 0.1 -3.912023 -2.302585 0.03 0.3 0.97 0.7 2.99 2.99 2.666667 11.0 0.728182

4.0 4.0 0.03 0.03 0.1 -3.506558 -2.302585 0.06 0.4 0.94 0.6 3.96 3.96 3.333333 11.0 0.640000

exgta exeqa

loss

0.0 11.000000 0.0

1.0 11.000000 1.0

2.0 11.090909 2.0

3.0 11.257732 3.0

4.0 11.489362 4.0

The Portfolio version is more exhaustive. It includes a variety of columns for each unit, suffixed _unit, and for the complement of each unit (sum of everything but that unit) suffixed _ημ_unit. The totals are suffixed _total. The most important columns are exeqa_unit, Conditional Expected Values. All the column names and a subset of density_df are shown next.

In [109]: print(p07.density_df.shape)

(65536, 46)

In [110]: print(p07.density_df.columns)

Index(['loss', 'p_A', 'p_B', 'p_Cat', 'p_total', 'F', 'S', 'exa_total', 'lev_total', 'exlea_total', 'e_total',

'exgta_total', 'exeqa_total', 'exeqa_A', 'lev_A', 'exlea_A', 'e_A', 'exgta_A', 'exi_x_A', 'exi_xlea_A',

'exi_xgta_A', 'exi_xeqa_A', 'exa_A', 'exeqa_B', 'lev_B', 'exlea_B', 'e_B', 'exgta_B', 'exi_x_B', 'exi_xlea_B',

'exi_xgta_B', 'exi_xeqa_B', 'exa_B', 'exeqa_Cat', 'lev_Cat', 'exlea_Cat', 'e_Cat', 'exgta_Cat', 'exi_x_Cat',

'exi_xlea_Cat', 'exi_xgta_Cat', 'exi_xeqa_Cat', 'exa_Cat', 'exi_xlea_sum', 'exi_xgta_sum', 'exi_xeqa_sum'],

dtype='object')

In [111]: with pd.option_context('display.max_columns', p07.density_df.shape[1]):

.....: print(p07.density_df.filter(regex=r'[aipex012]_A').head())

.....:

p_A exeqa_A exlea_A e_A exgta_A exi_x_A exi_xlea_A exi_xgta_A exi_xeqa_A exa_A

0.0 0.0 0.0 0.0 9999.982401 9999.982401 0.585913 0.0 0.585913 0.0 0.000000

2.0 0.0 0.0 0.0 9999.982401 9999.982401 0.585913 NaN 0.585913 0.0 1.171827

4.0 0.0 0.0 0.0 9999.982401 9999.982401 0.585913 NaN 0.585913 0.0 2.343653

6.0 0.0 0.0 0.0 9999.982401 9999.982401 0.585913 NaN 0.585913 0.0 3.515480

8.0 0.0 0.0 0.0 9999.982401 9999.982401 0.585913 NaN 0.585913 0.0 4.687306

2.3.9.4. The statistics Series and Dataframe

The statistics dataframe shows analytically computed mean, variance, CV, and sknewness. It is indexed by

severity name, limit and attachment,

freq1, freq2, freq3non-central frequency moments,sev1, sev2, sev3non-central severity moments, andthe mean, cv and skew(ness).

It applies to the gross outcome when there is reinsurance, so the results for a05g and a05no are the same.

In [112]: oco = ['display.width', 150, 'display.max_columns', 15,

.....: 'display.float_format', lambda x: f'{x:.5g}']

.....:

In [113]: with pd.option_context(*oco):

.....: print(a05g.statistics)

.....: print('\n')

.....: print(p07.statistics)

.....:

name TenM:05g

component measure

limit inf

attachment None

sevcv param 0

el 11

prem 0

lr 0

freq ex1 2

ex2 4

ex3 8

mean 2

cv 0

skew NaN

sev ex1 5.5

ex2 38.5

ex3 302.5

mean 5.5

cv 0.52223

skew 0

agg ex1 11

ex2 137.5

ex3 1875.5

mean 11

cv 0.36927

skew 0

mix cv [2.0]

wt 1

A B Cat total

component measure

freq ex1 100 150 2 252

ex2 10100 30750 6 71856

ex3 1.0301e+06 7.9868e+06 22 2.3216e+07

mean 100 150 2 252

cv 0.1 0.60553 0.70711 0.36266

skew 0.1 1.2001 0.70711 1.1783

sev ex1 100 45.213 616.02 71.484

ex2 25621 4068.7 4.1047e+06 45166

ex3 1.674e+07 6.7987e+05 1.7449e+11 1.3919e+09

mean 100 45.213 616.02 71.484

cv 1.2498 0.99517 3.1331 2.7998

skew 5.6619 3.4345 23.278 172.51

agg ex1 10000 6781.9 1232 18014

ex2 1.0256e+08 6.3163e+07 9.7273e+06 3.5244e+08

ex3 1.0785e+12 7.4665e+11 3.8119e+11 7.7915e+12

mean 10000 6781.9 1232 18014

cv 0.16006 0.61096 2.3256 0.29343

skew 0.4082 1.2009 14.837 2.9528

limit 10000 2500 1e+05 1e+05

P99.9e 15944 27628 41971 56972

2.3.9.5. The report_df Dataframe

The report_df dataframe combines information from statistics with

estimated moments to test if the numerical approximations appear valid. It

is an expanded version of describe. Numerically estimated statistics are

prefaced est or empirical.

In [114]: with pd.option_context(*oco):

.....: print(a05g.report_df)

.....: print('\n')

.....: print(p07.report_df)

.....:

view 0 independent mixed empirical error

statistic

name TenM:05g TenM:05g TenM:05g

limit inf inf inf

attachment 0 0

el 11 11 11

freq_m 2 2 2

freq_cv 0 0 0

freq_skew

sev_m 5.5 5.5 5.5 5.5 0

sev_cv 0.52223 0.52223 0.52223 0.52223 0

sev_skew 0 0 0 0

agg_m 11 11 11 11 -3.3307e-16

agg_cv 0.36927 0.36927 0.36927 0.36927 0

agg_skew 0 0 0 -6.1064e-14 -inf

unit A B Cat total

statistic

freq_m 100 150 2 252

freq_cv 0.1 0.60553 0.70711 0.36266

freq_skew 0.1 1.2001 0.70711 1.1783

sev_m 100 45.213 616.02 71.484

sev_cv 1.2498 0.99517 3.1331 2.7998

sev_skew 5.6619 3.4345 23.278 172.51

agg_m 10000 6781.9 1232 18014

agg_emp_m 10000 6781.8 1232 18013

agg_m_err -1.1973e-08 -1.2825e-05 -2.7692e-05 -2.6963e-05

agg_cv 0.16006 0.61096 2.3256 0.29343

agg_emp_cv 0.16007 0.61096 2.3249 0.29322

agg_cv_err 6.5168e-06 1.9129e-06 -0.00027305 -0.00070746

agg_skew 0.4082 1.2009 14.837 2.9528

agg_emp_skew 0.40819 1.2009 14.818 2.925

agg_skew_err -1.3542e-05 1.6688e-08 -0.0012766 -0.0094143

agg_emp_kurt 0.40604 2.1621 381.65 33.187

P99.0_emp 14206 19834 10246 33586

P99.6_emp 14956 22626 16610 38304

The report_df provides extra information when there is a mixed severity.

In [115]: with pd.option_context(*oco):

.....: print(a03.report_df)

.....:

view 0 1 2 independent mixed empirical error

statistic

name TenM:03 TenM:03 TenM:03 TenM:03 TenM:03

limit inf inf inf inf inf

attachment 0 0

el 62.5 125 187.5 375 375

freq_m 12.5 6.25 6.25 25 25

freq_cv 0.57446 0.64031 0.64031 0.36572 0.53852

freq_skew 1.0097 1.0307 1.0307 0.66199 1.0028

sev_m 5 20 30 15 15 14.999 -3.7467e-05

sev_cv 0.5 0.375 0.50002 0.90907 0.90907 0.89065 -0.020261

sev_skew 1 2.6716 inf inf inf 9.9075 -1

agg_m 62.5 125 187.5 375 375 374.99 -3.8034e-05

agg_cv 0.59161 0.65765 0.67082 0.41265 0.56838 0.5672 -0.0020722

agg_skew 1.0238 1.0613 inf inf inf 1.0698 -1

The dataframe shows statistics for each mixture component, columns 0,1,2,

their sum if they are added independently and their sum if there is a shared

mixing variable, as there is here. The common mixing induces correlation

between the mix components, acting to increases the CV and skewness, often

dramatically.

2.3.9.6. The spec and spec_ex Dictionaries

The spec dictionary contains the input information needed to create each

object. For example, if a is an Aggregate, then Aggregate

(**a.spec) creates a new copy. spec_ex appends meta-information to

spec about hyper-parameters.

In [116]: from pprint import pprint

In [117]: pprint(a05n.spec)

{'agg_kind': 'net of',

'agg_reins': [(1.0, 4.0, 8.0)],

'exp_attachment': None,

'exp_el': 0,

'exp_en': -1,

'exp_limit': inf,

'exp_lr': 0,

'exp_premium': 0,

'freq_a': array([2.]),

'freq_b': array([1.]),

'freq_name': 'empirical',

'freq_p0': nan,

'freq_zm': False,

'name': 'TenM:05n',

'note': '',

'occ_kind': 'net of',

'occ_reins': [(1.0, 3.0, 7.0)],

'sev_a': nan,

'sev_b': 0,

'sev_conditional': True,

'sev_cv': 0,

'sev_lb': 0,

'sev_loc': 0,

'sev_mean': 0,

'sev_name': 'dhistogram',

'sev_pick_attachments': None,

'sev_pick_losses': None,

'sev_ps': array([0.1, 0.1, 0.1, 0.1, 0.1, 0.1, 0.1, 0.1, 0.1, 0.1]),

'sev_scale': 0,

'sev_ub': inf,

'sev_wt': 1,

'sev_xs': array([ 1., 2., 3., 4., 5., 6., 7., 8., 9., 10.])}

2.3.9.7. The DecL Program

The program property returns the DecL program used to create the object.

It is blank if the object was not created using DecL. The helper function pprint_ex() pretty prints a program.

In [118]: from aggregate import pprint_ex

In [119]: pprint_ex(a05n.program, split=20)

agg TenM:05n

dfreq [2]

dsev [1:10]

occurrence net of 3 xs 7

aggregate net of 4 xs 8

Out[119]: 'agg TenM:05n\n dfreq [2]\n dsev [1:10]\n occurrence net of 3 xs 7\n aggregate net of 4 xs 8'

In [120]: pprint_ex(p07.program, split=20)

port TenM:07

agg A

100 claims 10000 xs 0

sev lognorm 100 cv 1.25

poisson

agg B

150 claims 2500 xs 5

sev lognorm 50 cv 0.9

mixed gamma .6

agg Cat

2 claims 1e5 xs 0

sev 500 * pareto 1.8 - 500

poisson

Out[120]: 'port TenM:07\n agg A\n 100 claims 10000 xs 0\n sev lognorm 100 cv 1.25\n poisson\n agg B\n 150 claims 2500 xs 5\n sev lognorm 50 cv 0.9\n mixed gamma .6\n agg Cat\n 2 claims 1e5 xs 0\n sev 500 * pareto 1.8 - 500\n poisson'

2.3.9.8. The update() Method

After an Aggregate or a Portfolio object has been created it needs to be updated to populate its density_df dataframe. build() automatically updates the objects it creates with default hyper-parameter values. Sometimes it is necessary to re-update with different hyper-parameters. The update() method takes arguments log2=13, bs=0, and recommend_p=0.999. The first two control the number and size of buckets. When bs==0 it is estimated using the method recommend_bucket(). If bs!=0 then recommend_p is ignored.

Further control over updating is available, as described in REF.

2.3.9.9. Statistical Functions

Aggregate and Portfolio objects include basic mean, CV, standard deviation, variance, and skewness statistics as attributes. Those prefixed agg are based on exact calculations:

agg_m,agg_cv,agg_sd,agg_var, andagg_skew

and prefixed est are based on the estimated numerical statistics:

est_m,est_cv,est_sd,est_var, andest_skew.

In addition, Aggregate has similar series prefixed sev and

est_sev for the exact and estimated numerical severity. These attributes

are just conveniences; they are all available in (or derivable from)

report_df.

Aggregate and Portfolio objects act like scipy.stats (continuous) frozen random variable objects and include the following statistical functions.

pmf()the probability mass functionpdf()the probability density function—broadly interpreted—defined as the pmf divided bybscdf()the cumulative distribution functionsf()the survival functionq()the quantile function (left inverse cdf), also known as value at risktvar()tail value at risk functionvar_dict()a dictionary of tail statistics by unit and in total

We aren’t picky about whether the density is technically a density when the aggregate is actually mixed or discrete.

The discrete output (density_df.p_*) is interpreted as the distribution, so none of the statistical functions is interpolated.

For example:

In [121]: qd(a05g.pmf(2), a05g.pmf(2.2), a05g.pmf(3), a05g.cdf(2), a05g.cdf(2.2))

0.01

0

0.02

0.01

0.01

In [122]: print(1 - a05g.cdf(2), a05g.sf(2))

0.99 0.99

In [123]: print(a05g.q(a05g.cdf(2)))

2.0

The last line illustrates that q() and cdf() are inverses. The var_dict() function computes tail statistics for all units, return in a dictionary.

In [124]: p07.var_dict(0.99), p07.var_dict(0.99, kind='tvar')

Out[124]:

({'A': np.float64(14206.0),

'B': np.float64(19834.0),

'Cat': np.float64(10246.0),

'total': np.float64(33586.0)},

{'A': np.float64(15025.781065020969),

'B': np.float64(22845.877658808236),

'Cat': np.float64(20360.451246691864),

'total': np.float64(41763.10848598601)})

2.3.9.10. The plot() Method

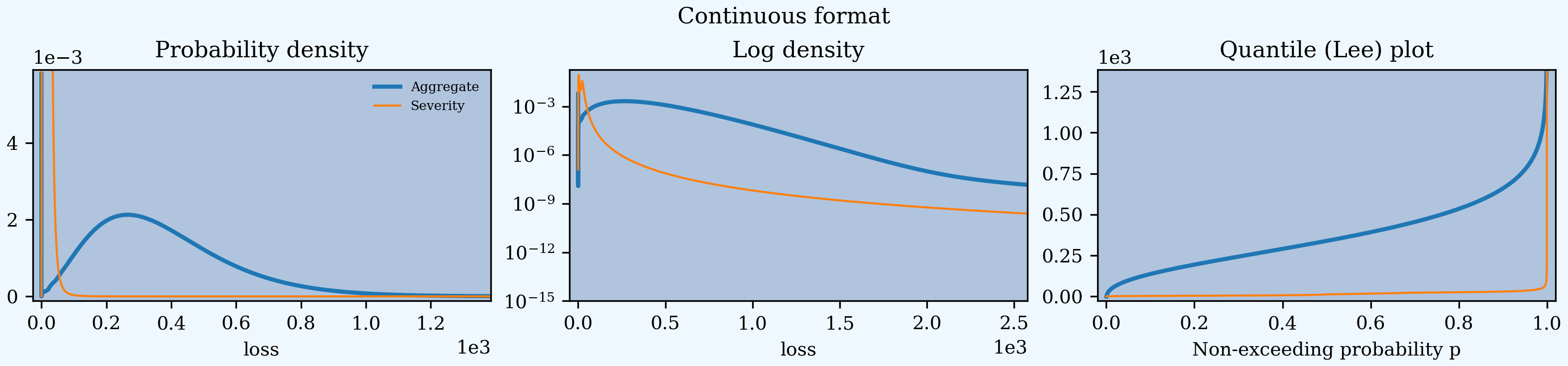

The plot() method provides basic visualization. There are three plots: the pdf/pmf for severity and the aggregate on the left. The middle plot shows log density for continuous distributions and the distribution function for discrete ones (selected when bs==1 and the mean is < 100). The right plot shows the quantile (or VaR or Lee) plot.

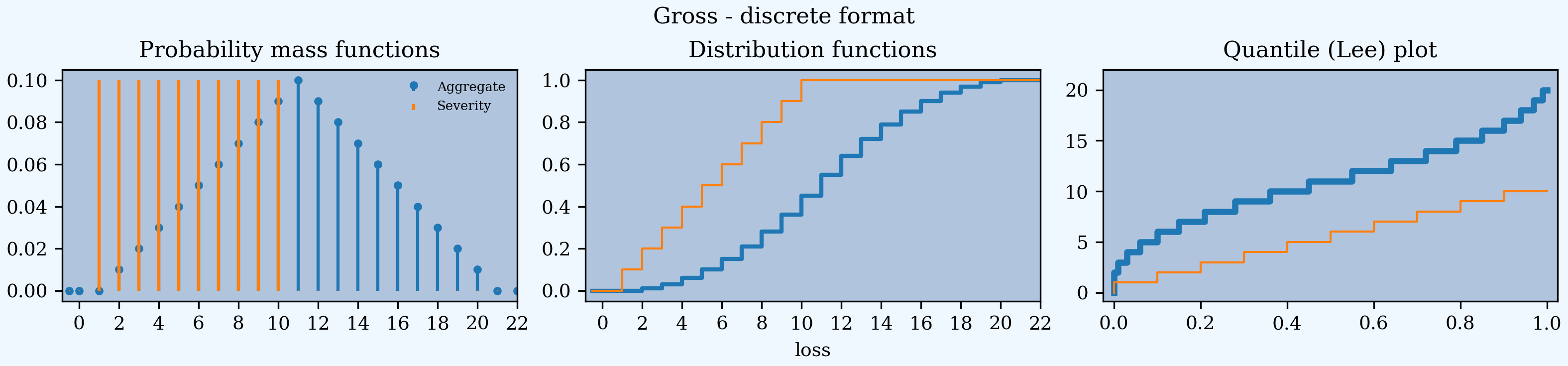

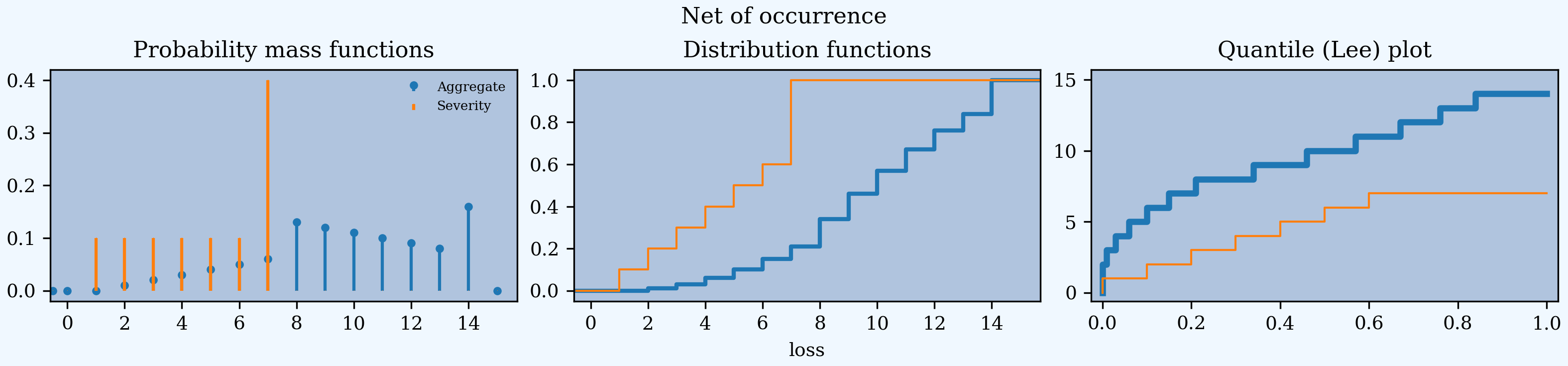

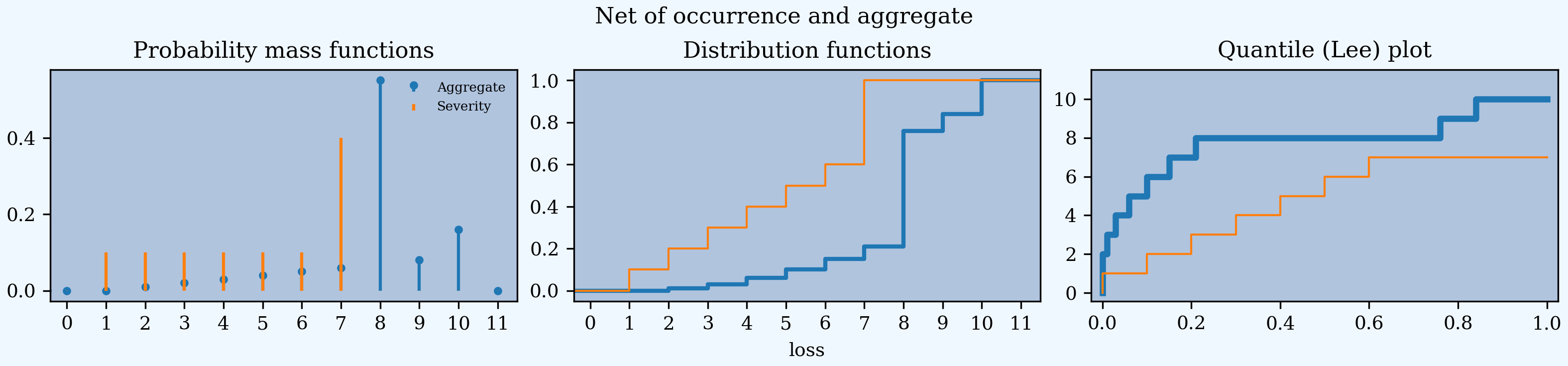

The reinsurance examples below show the discrete output format. The plots show the

gross, net of occurrence, and net severity and aggregate pmf (left) and cdf

(middle), and the quantile (Lee) plot (right). The property a05g.figure

returns the last figure made by the object as a convenience. You could also

use plt.gcf().

In [125]: a05g.plot()

In [126]: a05g.figure.suptitle('Gross - discrete format');

In [127]: a05no.plot()

In [128]: a05no.figure.suptitle('Net of occurrence');

In [129]: a05n.plot()

In [130]: a05n.figure.suptitle('Net of occurrence and aggregate');

Continuous distributions substitute the log density for the distribution in the middle.

In [131]: a03.plot()

In [132]: a03.figure.suptitle('Continuous format');

A Portfolio object plots the density and log density of each unit and

the total.

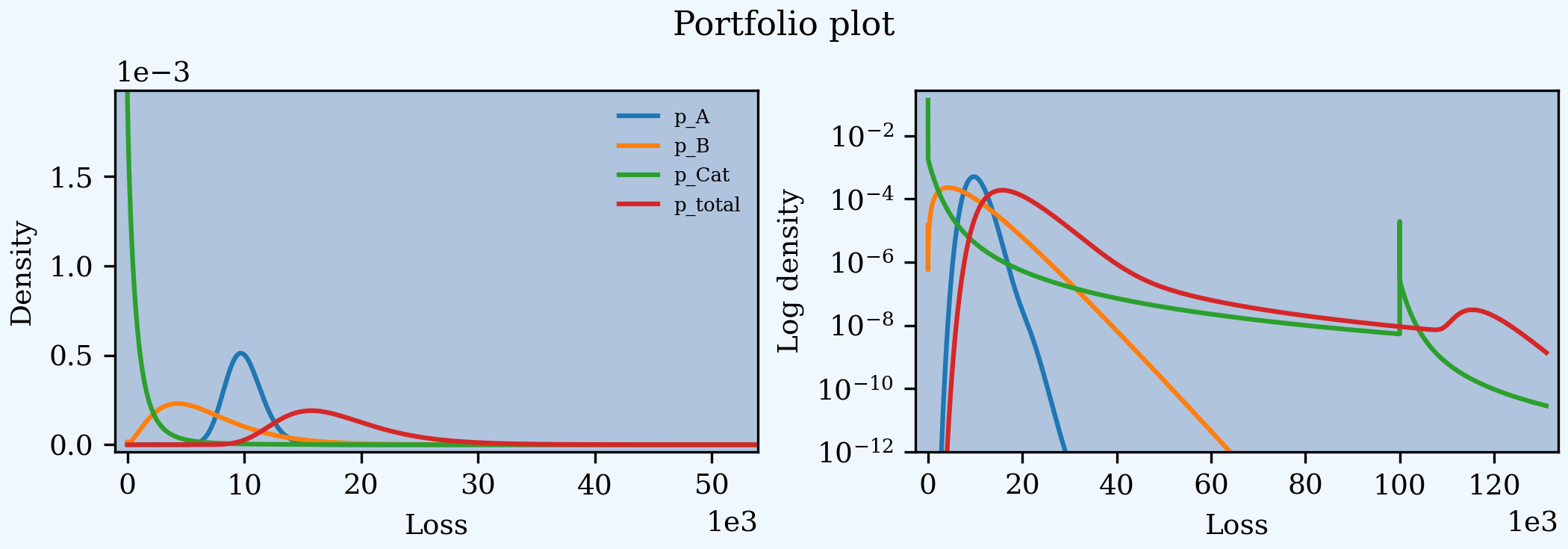

In [133]: p07.plot()

In [134]: p07.figure.suptitle('Portfolio plot');

2.3.9.11. The price() Method

The price() method computes the risk adjusted expected value (technical price net of expenses) of losses limited by capital at a specified VaR threshold. Suppose the 99.9%ile outcome is used to specify regulatory assets \(a\).

In [135]: qd(a03.q(0.999))

1358

The risk adjustment is specified by a spectral risk measure corresponding to an input distortion. Distortions can be built using DecL, see The Distortion Class. price() applies to \(X\wedge a\).

It returns expected limited losses L, the risk adjusted premium P, the margin M = P - L, the capital Q = a - P, the loss ratio, leverage as premium to capital PQ, and return on capital ROE.

In [136]: qd(a03.price(0.999, d06).T)

line TenM:03

statistic

L 374.82

P 558.25

M 183.43

Q 799.75

a 1358

LR 0.67142

PQ 0.69802

ROE 0.22936

When price() is applied to a Portfolio, it returns the total premium and its (lifted) natural allocation to each unit, see PIR Chapter 14, along with all the other statistics in a dataframe. Losses are allocated by equal priority in default.

In [137]: qd(p07.price(0.999, d06).df.T)

distortion dual

unit A B Cat total

statistic

L 9997.3 6779.8 1212.4 17990

P 10448 9874.5 1913.8 22236

M 450.25 3094.7 701.35 4246.2

Q 7656.6 10203 12817 30662

a 18104 20078 14731 52898

LR 0.9569 0.68659 0.63352 0.80904

PQ 1.3645 0.96781 0.14932 0.72519

COC 0.058806 0.30332 0.054721 0.13848

The ROE varies by unit, reflecting different consumption and cost of capital by layer. The less risky unit A runs at a higher loss ratio (cheaper insurance) but higher ROE than unit B because it consumes more expensive, equity-like lower layer capital but less capital overall (higher leverage).

2.3.9.12. The snap() Method

snap() rounds an input number to the index of density_df. It selects the nearest element.

2.3.9.13. The approximate() Method

The approximate() method creates an analytic approximation fit using moment matching. Normal, lognormal, gamma, shifted lognormal, and shifted gamma distributions can be fit, the last two requiring three moments. To fit all five and return a dictionary call with argument "all".

In [138]: fzs = a03.approximate('all')

In [139]: d = pd.DataFrame({k: fz.stats('mvs') for k, fz in fzs.items()},

.....: index=pd.Index(['mean', 'var', 'skew'], name='stat'),

.....: dtype=float)

.....:

In [140]: qd(d)

norm gamma lognorm sgamma slognorm

stat

mean 374.99 374.99 374.99 374.99 374.99

var 45238 45238 45238 45238 45238

skew 0 1.1344 1.8841 1.0698 1.0698

2.3.10. Additional Portfolio Methods

2.3.10.1. Conditional Expected Values

A Portfolio object’s density_df includes a slew of values to allocate capital (please don’t) or margin (please do). These all rely on what Mildenhall and Major [2022] call the \(\kappa\) function, defined for a sum \(X=\sum_i X_i\) as the conditional expectation

Notice that \(\sum_i \kappa_i(x)=x\), hinting at its allocation application.

See PIR Chapter 14.3 for an explanation of why \(\kappa\) is so useful. In short, it shows which units contribute to bad overall outcomes. It is in density_df as the columns exeqa_unit, read as the “expected value given X eq(uals) a”.

Here are some \(\kappa\) values and graph for p07. Looking the log density plot on the right shows that unit B dominates for moderately large events, but Cat dominates for the largest events.

In [141]: fig, axs = plt.subplots(1, 2, figsize=(2 * 3.5, 2.45)); \

.....: ax0, ax1 = axs.flat; \

.....: lm = [-1000, 65000]; \

.....: bit = p07.density_df.filter(regex='exeqa_[ABCt]').rename(

.....: columns=lambda x: x.replace('exeqa_', '')).sort_index(axis=1); \

.....: bit.index.name = 'Loss'; \

.....: bit.plot(xlim=lm, ylim=lm, ax=ax0); \

.....: ax0.set(title=r'$E[X_i\mid X]$', aspect='equal'); \

.....: ax0.axhline(bit['B'].max(), lw=.5, c='C7');

.....:

In [142]: p07.density_df.filter(regex='p_[ABCt]').rename(

.....: columns=lambda x: x.replace('p_', '')).plot(ax=ax1, xlim=lm, logy=True);

.....:

In [143]: ax1.set(title='Log density');

In [144]: bit['Pct A'] = bit['A'] / bit.index

In [145]: qd(bit.loc[:lm[1]:1024])

A B Cat total Pct A

Loss

0.0 0 0 0 0 NaN

2048.0 0 0 0 2048 0

4096.0 3729.8 307.48 58.741 4096 0.91059

6144.0 5419.3 602.16 122.54 6144 0.88205

8192.0 6911.6 1062.4 217.99 8192 0.8437

10240.0 8133.9 1757.5 348.62 10240 0.79432

12288.0 9041.7 2735.6 510.69 12288 0.73582

14336.0 9655.4 3986.6 694.09 14336 0.6735

16384.0 10048 5445.7 890.17 16384 0.61329

18432.0 10299 7035.3 1098 18432 0.55874

20480.0 10464 8692.1 1324.3 20480 0.51092

22528.0 10576 10370 1582.2 22528 0.46946

... ... ... ... ... ...

40960.0 10622 17734 12604 40960 0.25932

43008.0 10551 16531 15926 43008 0.24532

45056.0 10477 15060 19519 45056 0.23253

47104.0 10408 13547 23149 47104 0.22096

49152.0 10349 12178 26625 49152 0.21055

51200.0 10301 11051 29847 51200 0.20119

53248.0 10264 10185 32799 53248 0.19276

55296.0 10236 9545.6 35515 55296 0.18511

57344.0 10214 9085.2 38045 57344 0.17812

59392.0 10197 8755.1 40440 59392 0.17169

61440.0 10184 8516 42740 61440 0.16575

63488.0 10172 8339.2 44976 63488 0.16023

The thin horizontal line at the maximum value of exeqa_B (left plot) shows that \(\kappa_B\) is not increasing. Unit B contributes more to moderately bad outcomes than Cat, but in the tail Cat dominates.

Using filter(regex=...) to select columns from density_df is a helpful idiom. The total column is labeled _total. Using upper case for unit names makes them easier to select.

2.3.10.2. Calibrate Distortions

The calibrate_distortions() method calibrates distortions to achieve requested pricing for the total loss. Pricing can be requested by loss ratio or return on capital (ROE). Asset levels can be specified in monetary terms, or as a probability of non-exceedance. To calibrate the usual suspects (constant cost of capital, proportional hazard, dual, Wang, and TVaR) to achieve a 15% return with a 99.6% capital level run:

In [146]: p07.calibrate_distortions(Ps=[0.996], ROEs=[0.15], strict='ordered');

In [147]: qd(p07.distortion_df)

S L P PQ Q COC param std_param error

a LR method

38304.0 0.871293 ccoc 0.0039991 17962 20615 1.1654 17689 0.15 0.15 0.13043 0

ph 0.0039991 17962 20615 1.1654 17689 0.15 0.61919 0.23518 1.095e-09

wang 0.0039991 17962 20615 1.1654 17689 0.15 0.51526 0.2844 4.7105e-06

dual 0.0039991 17962 20615 1.1654 17689 0.15 2.0031 0.33402 -2.794e-09

tvar 0.0039991 17962 20615 1.1654 17689 0.15 0.37271 0.37271 9.7863e-06

In [148]: pprint(p07.dists)

{'ccoc': ccoc, 'dual': dual, 'ph': ph, 'tvar': tvar, 'wang': wang}

The answer is returned in the dist_ans dataframe. The requested distortions are all single parameter, returned in the param column. The last column gives the error in achieved premium. The attribute p07.dists is a dictionary with keys distortion types and values Distortion objects. See PIR REF for more discussion.

2.3.10.3. Analyze Distortions

The analyze_distortions() method applies the distortions in p07.dists at a given capital level and summarizes the implied (lifted) natural allocations across units. Optionally, it applies a number of traditional (bullshit) pricing methods. The answer dataframe includes premium, margin, expected loss, return, loss ratio and leverage statistics for each unit and method. Here is a snippet, again at the 99.6% capital level.

In [149]: ans = p07.analyze_distortions(p=0.996)

In [150]: print(ans.comp_df.xs('LR', axis=0, level=1).

.....: to_string(float_format=lambda x: f'{x:.1%}'))

.....:

line A B Cat total

Method

Dist ccoc 109.8% 103.8% 24.0% 87.1%

Dist dual 96.9% 77.8% 75.4% 87.1%

Dist ph 99.0% 80.6% 56.4% 87.1%

Dist tvar 96.3% 77.8% 77.8% 87.1%

Dist wang 97.7% 78.6% 67.7% 87.1%

EL 87.1% 87.1% 87.1% 87.1%

EPD 96.0% 78.3% 10.3% 58.6%

EqRiskEPD 99.7% 90.7% 38.4% 87.1%

EqRiskTVaR 95.7% 83.5% 58.0% 87.1%

EqRiskVaR 95.5% 82.7% 61.0% 87.1%

MerPer 97.9% 88.9% 66.0% 91.5%

ScaledEPD 107.9% 99.5% 26.3% 87.1%

ScaledTVaR 99.0% 85.3% 46.3% 87.1%

ScaledVaR 99.3% 84.9% 46.5% 87.1%

TVaR 94.3% 78.0% 38.0% 80.1%

VaR 93.9% 76.6% 37.3% 79.2%

coTVaR 99.1% 83.5% 49.3% 87.1%

covar 97.6% 80.6% 60.5% 87.1%

2.3.10.4. Twelve Plot

The twelve_plot() method produces a detailed analysis of the behavior of a two unit portfolio. To run it, build the portfolio and calibrate some distortions. Then apply one of the distortions (to compute an augmented version of density_df with pricing information). We give two examples.

First, the case of a thin-tailed and a thick-tailed unit. Here, the thick tailed line benefits from pooling at low capital levels, resulting in negative margins to the thin-tail line in compensation. At moderate to high capital levels the total margin for both lines is positive. Assets are 12.5. The argument efficient=False in apply_distortion() includes extra columns in density_df that are needed to compute the plot.

In [151]: p09 = build('port TenM:09 '

.....: 'agg X1 1 claim sev gamma 1 cv 0.25 fixed '

.....: 'agg X2 1 claim sev 0.7 * lognorm 1 cv 1.25 + 0.3 fixed'

.....: , bs=1/1024)

.....:

In [152]: qd(p09)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

X1 Freq 1 0

Sev 1 1 -5.5511e-16 0.25 0.25 0.5 0.5

Agg 1 1 -5.5511e-16 0.25 0.25 0.5 0.5

X2 Freq 1 0

Sev 1 0.99999 -1.0796e-05 0.875 0.87452 5.7031 5.603

Agg 1 0.99999 -1.0796e-05 0.875 0.87452 5.7031 5.603

total Freq 2 0

Sev 1 0.99999 -5.398e-06 0.64348 7.1845

Agg 2 2 -5.8107e-06 0.45501 0.45476 5.0802 4.9869

log2 = 16, bandwidth = 1/1024, validation: fails sev skew, agg skew.

In [153]: print(f'Asset P value {p09.cdf(12.5):.5g}')

Asset P value 0.99958

In [154]: p09.calibrate_distortions(ROEs=[0.1], As=[12.5], strict='ordered');

In [155]: qd(p09.distortion_df)

S L P PQ Q COC param std_param error

a LR method

12.5 0.676722 ccoc 0.00041558 1.9985 2.9531 0.30933 9.5469 0.1 0.1 0.090909 0

ph 0.00041558 1.9985 2.9531 0.30933 9.5469 0.1 0.51152 0.32317 1.998e-08

wang 0.00041558 1.9985 2.9531 0.30933 9.5469 0.1 0.88394 0.46806 1.6577e-06

dual 0.00041558 1.9985 2.9531 0.30933 9.5469 0.1 4.4902 0.63572 -2.0466e-10

tvar 0.00041558 1.9985 2.9531 0.30933 9.5469 0.1 0.71207 0.71207 6.2397e-06

In [156]: p09.apply_distortion('dual', efficient=False);

In [157]: fig, axs = plt.subplots(4, 3, figsize=(3 * 3.5, 4 * 2.45), constrained_layout=True)

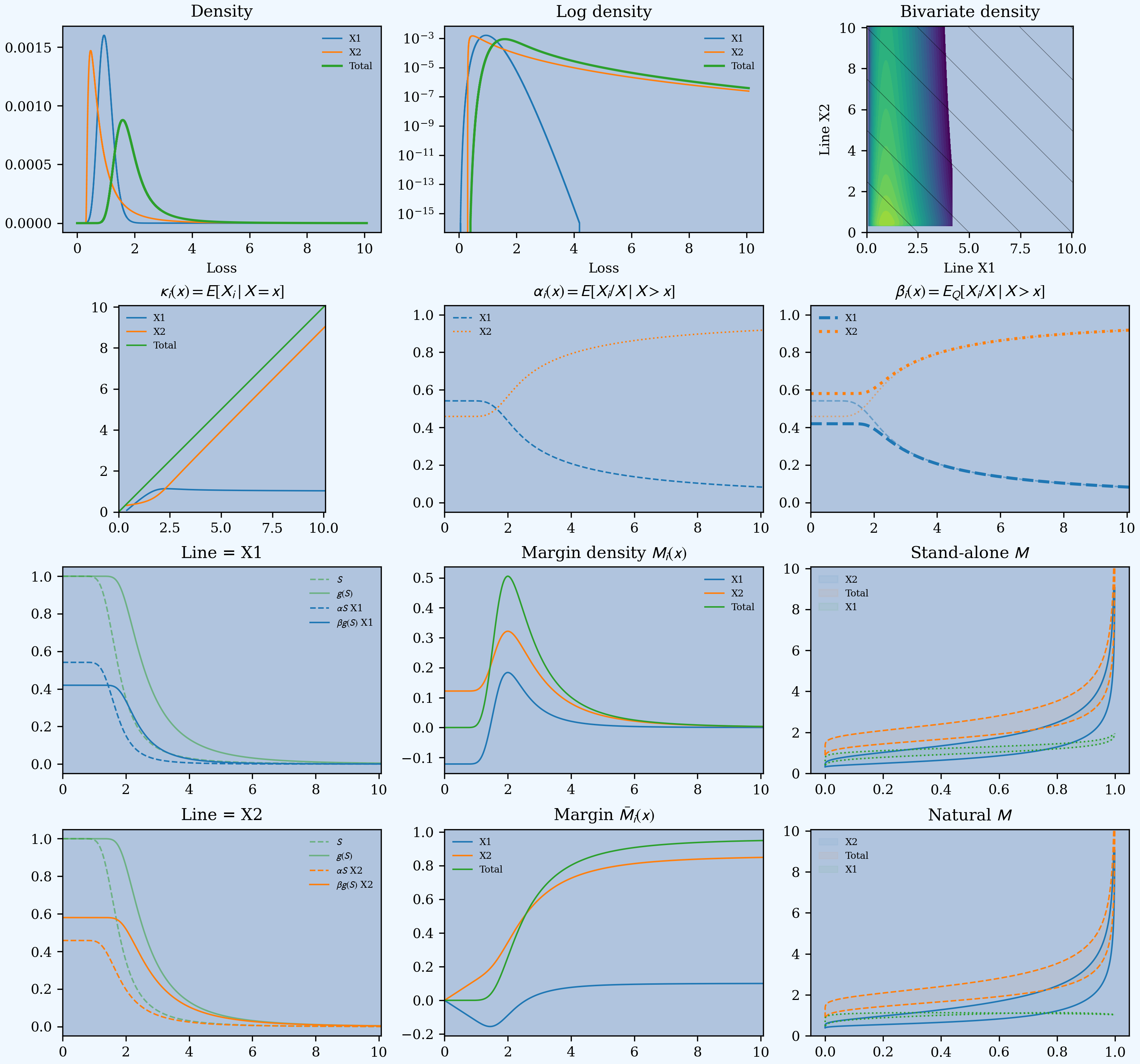

In [158]: p09.twelve_plot(fig, axs, p=0.999, p2=0.999)

There is a lot of information here. We refer to the charts as \((r,c)\) for row \(r=1,2,3,4\) and column \(c=1,2,3\), starting at the top left. The horizontal axis shows the asset level in all charts except \((3,3)\) and \((4,3)\), where it shows probability, and \((1,3)\) where it shows loss. Blue represents the thin tailed unit, orange thick tailed and green total. When both dashed and solid lines appear on the same plot, the solid represent risk-adjusted and dashed represent non-risk-adjusted functions. Here is the key.

\((1,1)\) shows density for \(X_1, X_2\) and \(X=X_1+X_2\); the two units are independent. Both units have mean 1.

\((1,2)\): log density; comparing tail thickness.

\((1,3)\): the bivariate log-density. This plot illustrates where \((X_1, X_2)\) lives. The diagonal lines show \(X=k\) for different \(k\). These show that large values of \(X\) correspond to large values of \(X_2\), with \(X_1\) about average.

\((2,1)\): the form of \(\kappa_i\) is clear from looking at \((1,3)\). \(\kappa_1\) peaks above 1.0 around \(x=2\) and hereafter it declines to 1.0. \(\kappa_2\) is monotonically increasing.

\((2,2)\): The \(\alpha_i\) functions. For small \(x\) the expected proportion of losses is approximately 50/50, since the means are equal. As \(x\) increases \(X_2\) dominates. The two functions sum to 1.

\((2,3)\): The thicker lines are \(\beta_i\) and the thinner lines \(\alpha_i\) from \((2,2)\). Since \(\alpha_1\) decreases \(\beta_1(x)\le \alpha_1(x)\). This can lead to \(X_1\) having a negative margin in low asset layers. \(X_2\) is the opposite.

\((3,1)\): illustrates premium and margin determination by asset layer for \(X_1\). For low asset layers \(\alpha_1(x) S(x)>\beta_1(x) g(S(x))\) (dashed above solid) corresponding to a negative margin. Beyond about \(x=1.38\) the lines cross and the margin is positive.

\((4,1)\): shows the same thing for \(X_2\). Since \(\alpha_2\) is increasing, \(\beta_2(x)>\alpha_2(x)\) for all \(x\) and so all layers get a positive margin. The solid line \(\beta_2 gS\) is above the dashed \(\alpha_2 S\) line.