2.5. Individual Risk Pricing

Objectives: Applications of the Aggregate class to individual risk pricing, including LEVs, ILFs, layering, and the insurance charge and savings (Table L, M), illustrated using problems from CAS Part 8.

Audience: Individual risk large account pricing, broker, or risk retention actuary.

Prerequisites: DecL, underwriting and insurance terminology, aggregate distributions, risk measures.

See also: Reinsurance Pricing, The Reinsurance Clauses. For other related examples see Published Problems and Examples, especially Bahnemann Monograph. Self-Insurance Plan Stop-Loss Insurance for theoretical background.

Contents:

The examples in this section are illustrative. aggregate gives the gross,

ceded, and net distributions and with those in hand, it is possible to answer

any reasonable question about a large account program.

2.5.1. Helpful References

2.5.2. Insurance Charge and Insurance Savings in Aggregate

Creating a custom table of insurance charges and savings, varying with account

size, specific occurrence limit, and entry ratio (aggregate limit) is very

easy using aggregate. We will make a custom function to illustrate one

solution.

First, we need a severity curve. This step is very important, and would be

customized to the state and hazard group distribution of expected losses. We

use a simple mixture of a lognormal for small claims and a Pareto for large

claims, with a mean of about 25 (work in 000s). Create it as an object in the

knowledge using build(). The parameters are selected judgmentally.

In [1]: from aggregate import build, qd

In [2]: mu, sigma, shape, scale, wt = \

...: -0.204573975, 1.409431871, 1.633490596, 57.96737143, 0.742942461

...:

In [3]: mean = wt * np.exp(mu + sigma**2 / 2) + (1 - wt) * scale / (shape - 1)

In [4]: build(f'sev IR:WC '

...: f'[exp({mu}) {scale}] * [lognorm pareto] [{sigma} {shape}] '

...: f'+ [0 {-scale}] wts [{wt} {1-wt}]');

...:

In [5]: print(f'Mean = {mean:.1f} in 000s')

Mean = 25.2 in 000s

Second, we will build the model for a large account with 350 expected claims and an occurrence limit of 100M. This model is used to set the update parameters. Assume a gamma mixed Poisson frequency distribution with a mixing CV of 25% throughout. The CV could be an input parameter in a production application.

In [6]: a01 = build('agg IR:Base '

...: '350 claims '

...: '100000 xs 0 '

...: 'sev sev.IR:WC '

...: 'mixed gamma 0.25 ',

...: update=False)

...:

In [7]: qd(a01)

E[X] CV(X) Skew(X)

X

Freq 350 0.25565 0.50012

Sev 24.947 10.172 177.37

Agg 8731.6 0.6008 7.3319

log2 = 0, bandwidth = na, validation: n/a, not updated.

In [8]: qd(a01.statistics.loc['sev', [0, 1, 'mixed']])

name 0 1 mixed

measure

ex1 2.2005 90.69 24.947

ex2 35.299 2.5281e+05 65013

ex3 4127.8 1.1293e+10 2.9029e+09

mean 2.2005 90.69 24.947

cv 2.508 5.4532 10.172

skew 23.299 92.803 177.37

Look at the aggregate_error_analysis to pick bs (see Estimating and Testing bs For Aggregate Objects). Use an expanded number of buckets log2=19 because the mixture

includes small mean lognormal and large mean Pareto components (some trial

and error not shown).

In [9]: err_anal = a01.aggregate_error_analysis(19)

In [10]: qd(err_anal, sparsify=False)

view agg est abs rel rel rel

stat m m m m h total

bs

0.0625 8731.6 8552.1 -179.54 -0.020562 0.0012526 -0.021815

0.1250 8731.6 8647.1 -84.529 -0.0096808 0.0025053 -0.012186

0.2500 8731.6 8731.1 -0.5447 -6.2382e-05 0.0050105 -0.0050729

0.5000 8731.6 8728.8 -2.798 -0.00032045 0.010021 -0.010342

1.0000 8731.6 8719.9 -11.715 -0.0013417 0.020042 -0.021384

2.0000 8731.6 8694.4 -37.172 -0.0042572 0.040084 -0.044341

4.0000 8731.6 8639.2 -92.465 -0.01059 0.080168 -0.090758

Select bs=1/4 as the most accurate from the displayed range (``

(‘rel’, ‘m’)``). Update and plot. The plot shows the impact of the occurrence

limit in the extreme right tail.

In [11]: a01.update(approximation='exact', log2=19, bs=1/4, normalize=False)

In [12]: qd(a01)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 350 0.25565 0.50012

Sev 24.947 24.946 -5.5033e-05 10.172 10.172 177.37 177.37

Agg 8731.6 8731.1 -6.2382e-05 0.6008 0.60063 7.3319 7.3121

log2 = 19, bandwidth = 1/4, validation: not unreasonable.

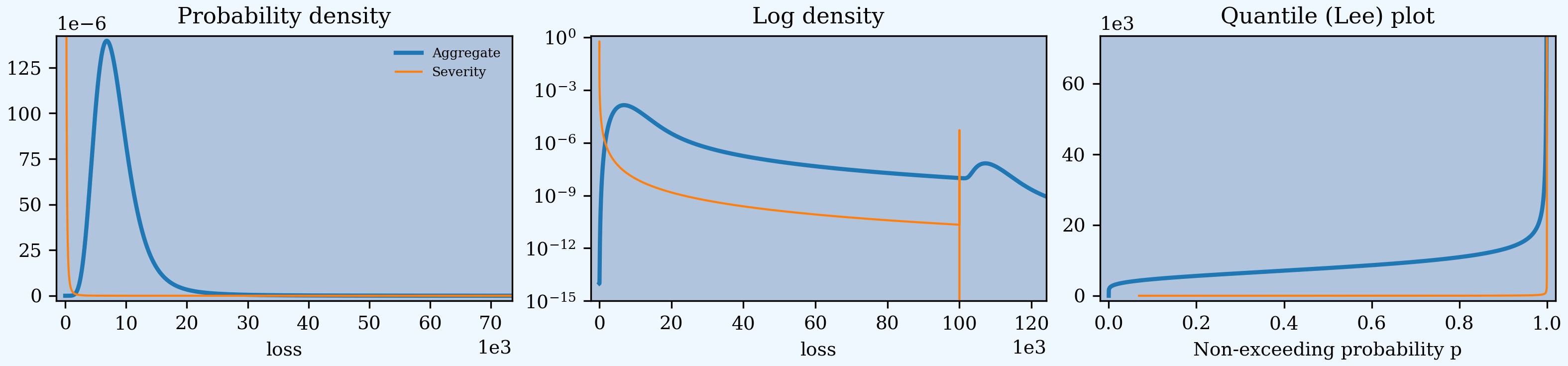

In [13]: a01.plot()

Third, create a custom function of account size and the occurrence limit, to

produce the Aggregate object and a small table of insurance savings

and charges. Account size is measured by the expected ground-up claim count.

It should be clear how to extend this function to include custom severity,

different mixing CVs, or produce factors for different entry ratios. The

answer is returned in a namedtuple.

In [14]: from collections import namedtuple

In [15]: def make_table(claims=360, occ_limit=100000):

....: """

....: Make a table of insurance charges and savings by entry ratio for

....: specified account size (expected claim count) and specific

....: occurrence limit.

....: """

....: a01 = build(f'agg IR:{claims}:{occ_limit} '

....: f'{claims} claims '

....: f'{occ_limit} xs 0 '

....: 'sev sev.IR:WC '

....: 'mixed gamma 0.25 '

....: , approximation='exact', log2=19, bs=1/4, normalize=False)

....: er_table = np.linspace(.1, 2., 20)

....: df = a01.density_df

....: ix = df.index.get_indexer(er_table * a01.est_m, method='nearest')

....: df = a01.density_df.iloc[ix][['loss', 'F', 'S', 'e', 'lev']]

....: df['er'] = er_table

....: df['charge'] = (df.e - df.lev) / a01.est_m

....: df['savings'] = (df.loss - df.lev) / a01.est_m

....: df['entry'] = df.loss / a01.est_m

....: df = df.set_index('entry')

....: df = df.drop(columns=['e', 'er'])

....: df.index = [f"{x:.2f}" for x in df.index]

....: df.index.name = 'r'

....: Table = namedtuple('Table', ['ob', 'table_df'])

....: return Table(a01, df)

....:

Finally, apply the new function to create some tables.

A small account with 25 expected claims, about 621K limited losses, and a low 50K occurrence limit. The output shows the usual

describediagnostics for the underlyingAggregateobject, followed by a small Table across different entry ratios. The Table is indexed by entry ratio(aggregate attachment as a proportion of limited losses) and showslossthe aggregate limit loss level in currency units; the cdf and sf at that loss level (the latter giving the probability the aggregate layer attaches); the limited expected value at the entry ratiolev; and the insurance charge(1 - lev / loss) and savings (r - lev / loss).

In [16]: tl = make_table(25, 50)

In [17]: fc = lambda x: f'{x:,.1f}' if abs(x) > 10 else f'{x:.3f}'

In [18]: qd(tl.ob)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 25 0.32016 0.51537

Sev 9.2527 9.2513 -0.00014797 1.7107 1.711 1.8407 1.8405

Agg 231.32 231.28 -0.00014797 0.46857 0.46862 0.65759 0.65759

log2 = 19, bandwidth = 1/4, validation: fails sev mean, agg mean.

In [19]: qd(tl.table_df, float_format=fc, col_space=8)

loss F S lev charge savings

r

0.10 23.2 0.005 0.995 23.2 0.900 0.000

0.20 46.2 0.017 0.983 46.0 0.801 0.001

0.30 69.5 0.041 0.959 68.6 0.703 0.004

0.40 92.5 0.081 0.919 90.2 0.610 0.010

0.50 115.8 0.135 0.865 111.0 0.520 0.021

0.60 138.8 0.205 0.795 130.1 0.438 0.037

0.70 162.0 0.284 0.716 147.7 0.361 0.062

0.80 185.0 0.370 0.630 163.2 0.294 0.094

0.90 208.2 0.459 0.541 176.8 0.236 0.136

1.00 231.2 0.544 0.456 188.3 0.186 0.186

1.10 254.5 0.625 0.375 197.9 0.144 0.245

1.20 277.5 0.696 0.304 205.7 0.110 0.310

1.30 300.8 0.760 0.240 212.0 0.083 0.384

1.40 323.8 0.813 0.187 216.9 0.062 0.462

1.50 347.0 0.857 0.143 220.8 0.045 0.546

1.60 370.0 0.892 0.108 223.7 0.033 0.633

1.70 393.2 0.920 0.080 225.8 0.024 0.724

1.80 416.2 0.941 0.059 227.4 0.017 0.816

1.90 439.5 0.958 0.042 228.6 0.012 0.912

2.00 462.5 0.970 0.030 229.4 0.008 1.008

The impact of increasing the occurrence limit to 250K:

In [20]: tl2 = make_table(25, 250)

In [21]: qd(tl2.ob)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 25 0.32016 0.51537

Sev 16.989 16.988 -8.0799e-05 2.5894 2.5897 3.852 3.852

Agg 424.73 424.69 -8.0799e-05 0.60885 0.60889 0.91444 0.91445

log2 = 19, bandwidth = 1/4, validation: not unreasonable.

In [22]: qd(tl2.table_df, float_format=fc, col_space=8)

loss F S lev charge savings

r

0.10 42.5 0.015 0.985 42.3 0.900 0.001

0.20 85.0 0.052 0.948 83.4 0.804 0.004

0.30 127.5 0.104 0.896 122.7 0.711 0.011

0.40 170.0 0.164 0.836 159.5 0.624 0.025

0.50 212.2 0.227 0.773 193.5 0.544 0.044

0.60 254.8 0.291 0.709 225.0 0.470 0.070

0.70 297.2 0.358 0.642 253.7 0.403 0.102

0.80 339.8 0.428 0.572 279.6 0.342 0.142

0.90 382.2 0.497 0.503 302.4 0.288 0.188

1.00 424.8 0.562 0.438 322.4 0.241 0.241

1.10 467.2 0.622 0.378 339.7 0.200 0.300

1.20 509.8 0.677 0.323 354.6 0.165 0.365

1.30 552.0 0.726 0.274 367.2 0.135 0.435

1.40 594.5 0.770 0.230 377.9 0.110 0.510

1.50 637.0 0.808 0.192 386.9 0.089 0.589

1.60 679.5 0.842 0.158 394.3 0.072 0.672

1.70 722.0 0.870 0.130 400.4 0.057 0.757

1.80 764.5 0.894 0.106 405.4 0.046 0.846

1.90 807.0 0.915 0.085 409.4 0.036 0.936

2.00 849.5 0.931 0.069 412.7 0.028 1.029

The impact of increasing the account size to 250 expected claims, still at 250K occurrence limit:

In [23]: tl3 = make_table(250, 250)

In [24]: qd(tl3.ob)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 250 0.25788 0.50024

Sev 16.989 16.988 -8.0799e-05 2.5894 2.5897 3.852 3.852

Agg 4247.3 4246.9 -8.0799e-05 0.30548 0.30549 0.52614 0.52615

log2 = 19, bandwidth = 1/4, validation: not unreasonable.

In [25]: qd(tl3.table_df, float_format=fc, col_space=8)

loss F S lev charge savings

r

0.10 424.8 0.000 1.000 424.7 0.900 0.000

0.20 849.5 0.000 1.000 849.5 0.800 0.000

0.30 1,274.0 0.001 0.999 1,273.7 0.700 0.000

0.40 1,698.8 0.009 0.991 1,696.7 0.600 0.000

0.50 2,123.5 0.031 0.969 2,113.8 0.502 0.002

0.60 2,548.2 0.080 0.920 2,516.2 0.408 0.008

0.70 2,972.8 0.161 0.839 2,890.8 0.319 0.019

0.80 3,397.5 0.272 0.728 3,224.5 0.241 0.041

0.90 3,822.2 0.402 0.598 3,506.5 0.174 0.074

1.00 4,247.0 0.535 0.465 3,732.1 0.121 0.121

1.10 4,671.8 0.657 0.343 3,903.0 0.081 0.181

1.20 5,096.2 0.760 0.240 4,025.9 0.052 0.252

1.30 5,521.0 0.840 0.160 4,110.1 0.032 0.332

1.40 5,945.8 0.898 0.102 4,165.1 0.019 0.419

1.50 6,370.5 0.937 0.063 4,199.6 0.011 0.511

1.60 6,795.0 0.963 0.037 4,220.4 0.006 0.606

1.70 7,219.8 0.979 0.021 4,232.5 0.003 0.703

1.80 7,644.5 0.988 0.012 4,239.3 0.002 0.802

1.90 8,069.2 0.994 0.006 4,243.0 0.001 0.901

2.00 8,494.0 0.997 0.003 4,244.9 0.000 1.000

Finally, increase the occurrence limit to 10M:

In [26]: tl4 = make_table(250, 10000)

In [27]: qd(tl4.ob)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 250 0.25788 0.50024

Sev 24.26 24.258 -5.6594e-05 6.2915 6.2918 33.759 33.759

Agg 6064.9 6064.6 -5.6594e-05 0.47416 0.47418 1.6385 1.6386

log2 = 19, bandwidth = 1/4, validation: not unreasonable.

In [28]: qd(tl4.table_df, float_format=fc, col_space=8)

loss F S lev charge savings

r

0.10 606.5 0.000 1.000 606.5 0.900 0.000

0.20 1,213.0 0.001 0.999 1,212.9 0.800 0.000

0.30 1,819.2 0.008 0.992 1,817.1 0.700 0.000

0.40 2,425.8 0.033 0.967 2,412.5 0.602 0.002

0.50 3,032.2 0.086 0.914 2,984.7 0.508 0.008

0.60 3,638.8 0.168 0.832 3,515.7 0.420 0.020

0.70 4,245.2 0.272 0.728 3,989.4 0.342 0.042

0.80 4,851.8 0.385 0.615 4,396.7 0.275 0.075

0.90 5,458.0 0.496 0.504 4,735.5 0.219 0.119

1.00 6,064.5 0.595 0.405 5,010.4 0.174 0.174

1.10 6,671.0 0.680 0.320 5,229.3 0.138 0.238

1.20 7,277.5 0.750 0.250 5,401.4 0.109 0.309

1.30 7,884.0 0.805 0.195 5,535.8 0.087 0.387

1.40 8,490.5 0.847 0.153 5,640.8 0.070 0.470

1.50 9,096.8 0.880 0.120 5,723.1 0.056 0.556

1.60 9,703.2 0.905 0.095 5,788.1 0.046 0.646

1.70 10,309.8 0.924 0.076 5,839.8 0.037 0.737

1.80 10,916.2 0.938 0.062 5,881.6 0.030 0.830

1.90 11,522.8 0.949 0.051 5,915.7 0.025 0.925

2.00 12,129.0 0.958 0.042 5,943.8 0.020 1.020

These Tables all behave as expected. The insurance charge decreases with increasing expected losses (claim count) and decreasing occurrence limit.

2.5.3. Summary of Objects Created by DecL

Objects created by build() in this guide.

In [29]: from aggregate import pprint_ex

In [30]: for n, r in build.qlist('^IR:').iterrows():

....: pprint_ex(r.program, split=20)

....:

agg IR:250:10000

250 claims 10000 xs 0

sev

sev.IR:WC

mixed gamma 0.25

agg IR:250:250

250 claims 250 xs 0

sev

sev.IR:WC

mixed gamma 0.25

agg IR:25:250

25 claims 250 xs 0

sev

sev.IR:WC

mixed gamma 0.25

agg IR:25:50

25 claims 50 xs 0

sev

sev.IR:WC

mixed gamma 0.25

agg IR:Base

350 claims 100000 xs 0

sev

sev.IR:WC

mixed gamma 0.25

sev IR:WC [exp(-0.204573975) 57.96737143] * [lognorm pareto] [1.409431871 1.633490596] + [0 -57.96737143]

wts [0.742942461 0.25705753899999995]