2.13.5. Loss Models Book

Examples from the text Klugman et al. [2019], Loss Models: from data to decisions. The Loss models book is used as a text for several actuarial society exams and many college courses. KPW is shorthand for Loss Models.

2.13.5.1. Contents

2.13.5.2. Method of Moments Approximations, Examples 9.3 and 9.4

The observed mean (and standard deviation) of the number of claims and the individual losses over the past 10 months are 6.7 (2.3) and 179,247 (52,141), respectively. Determine the mean and standard deviation of aggregate claims per month.

In [1]: from aggregate import build, qd, mv, MomentAggregator, round_bucket

In [2]: import scipy.stats as ss

In [3]: import pandas as pd

In [4]: import numpy as np

In [5]: import matplotlib.pyplot as plt

In [6]: moms = MomentAggregator.agg_from_fs2(6.7, 2.3**2, 179247, 52141**2)

In [7]: moms

Out[7]:

ex 1.200955e+06

var 1.881802e+11

sd 4.337974e+05

cv 3.612104e-01

dtype: float64

Using normal and lognormal distributions as approximating distributions for aggregate claims, calculate the probability that claims will exceed 140% of expected costs.

In [8]: fzn = ss.norm(loc=moms.ex, scale=moms.sd)

In [9]: sigma = np.sqrt(np.log(moms.cv**2 + 1))

In [10]: fzl = ss.lognorm(sigma, scale=moms.ex*np.exp(-sigma**2/2))

In [11]: fzn.sf(1.4 * moms.ex), fzl.sf(1.4 * moms.ex)

Out[11]: (0.1340631332467369, 0.1279965072394511)

Notes.

How to make the lognormal…

2.13.5.3. Group Dental Insurance, Examples 9.5, 9.6

Under a group dental insurance plan covering employees and their families, the premium for each married employee is the same regardless of the number of family members. The insurance company has compiled statistics showing that the annual cost of dental care per person for the benefits provided by the plan has the distribution (given in units of 25) on the left.

Furthermore, the distribution of the number of persons per insurance certificate (i.e. per employee) receiving dental care in any year has the distribution on the right.

Determine the mean and standard deviation of total payments per employee.

In [12]: kpw_9_5 = build('agg KPW.95 '

....: 'dfreq [0:8] [0.05, 0.1, 0.15, 0.2, 0.25, 0.15, 0.06, 0.03, 0.01] '

....: 'dsev [1:10] [0.15, 0.2, 0.25, 0.125, 0.075, 0.05, 0.05, 0.05, 0.025, 0.025]')

....:

In [13]: qd(kpw_9_5)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3.4 0.50602 0.063622

Sev 3.7 3.7 0 0.62572 0.62572 1.0074 1.0074

Agg 12.58 12.58 -4.4409e-16 0.60927 0.60927 0.52196 0.52196

log2 = 8, bandwidth = 1, validation: not unreasonable.

In [14]: mv(kpw_9_5)

mean = 12.58

variance = 58.7464

std dev = 7.66462

The probability distributions are in the density_df dataframe.

In [15]: with pd.option_context('display.max_rows', 360, 'display.max_columns', 10,

....: 'display.width', 150,

....: 'display.float_format', lambda x: f'{x:.5g}'):

....: print(kpw_9_5.density_df.query('p > 0')[['p', 'F', 'S']])

....:

p F S

loss

0 0.05 0.05 0.95

1 0.015 0.065 0.935

2 0.023375 0.088375 0.91163

3 0.034675 0.12305 0.87695

4 0.032577 0.15563 0.84437

5 0.035786 0.19141 0.80859

6 0.039808 0.23122 0.76878

7 0.043562 0.27478 0.72522

8 0.047518 0.3223 0.6777

9 0.049034 0.37133 0.62867

10 0.051898 0.42323 0.57677

11 0.051379 0.47461 0.52539

12 0.051187 0.5258 0.4742

13 0.050305 0.5761 0.4239

14 0.048182 0.62429 0.37571

15 0.045759 0.67004 0.32996

16 0.042809 0.71285 0.28715

17 0.039378 0.75223 0.24777

18 0.035746 0.78798 0.21202

19 0.031968 0.81995 0.18005

20 0.028324 0.84827 0.15173

21 0.024788 0.87306 0.12694

22 0.021491 0.89455 0.10545

23 0.018458 0.91301 0.086993

24 0.015692 0.9287 0.0713

25 0.013234 0.94193 0.058066

26 0.011076 0.95301 0.04699

27 0.0092013 0.96221 0.037789

28 0.0075941 0.96981 0.030195

29 0.0062231 0.97603 0.023972

30 0.0050662 0.98109 0.018906

31 0.0040954 0.98519 0.01481

32 0.003288 0.98848 0.011522

33 0.0026221 0.9911 0.0089001

34 0.002076 0.99318 0.0068241

35 0.001632 0.99481 0.0051921

36 0.0012732 0.99608 0.0039189

37 0.00098531 0.99707 0.0029336

38 0.00075628 0.99782 0.0021773

39 0.00057544 0.9984 0.0016019

40 0.000434 0.99883 0.0011679

41 0.00032431 0.99916 0.00084357

42 0.00024008 0.9994 0.00060349

43 0.000176 0.99957 0.00042749

44 0.00012773 0.9997 0.00029976

45 9.1748e-05 0.99979 0.00020801

46 6.52e-05 0.99986 0.00014281

47 4.5831e-05 0.9999 9.6977e-05

48 3.1858e-05 0.99993 6.5119e-05

49 2.1894e-05 0.99996 4.3225e-05

50 1.4871e-05 0.99997 2.8353e-05

51 9.9806e-06 0.99998 1.8373e-05

52 6.6161e-06 0.99999 1.1757e-05

53 4.3305e-06 0.99999 7.4261e-06

54 2.7976e-06 1 4.6285e-06

55 1.7833e-06 1 2.8452e-06

56 1.1211e-06 1 1.7241e-06

57 6.9482e-07 1 1.0292e-06

58 4.2428e-07 1 6.0496e-07

59 2.5511e-07 1 3.4985e-07

60 1.5095e-07 1 1.989e-07

61 8.7827e-08 1 1.1107e-07

62 5.0209e-08 1 6.086e-08

63 2.8179e-08 1 3.2681e-08

64 1.5508e-08 1 1.7173e-08

65 8.3573e-09 1 8.8161e-09

66 4.4032e-09 1 4.4129e-09

67 2.2637e-09 1 2.1492e-09

68 1.1334e-09 1 1.0158e-09

69 5.5143e-10 1 4.6435e-10

70 2.6002e-10 1 2.0433e-10

71 1.1836e-10 1 8.5974e-11

72 5.1711e-11 1 3.4264e-11

73 2.1497e-11 1 1.2767e-11

74 8.3923e-12 1 4.3749e-12

75 3.0273e-12 1 1.3476e-12

76 9.8572e-13 1 3.6182e-13

77 2.8076e-13 1 8.1046e-14

78 6.7141e-14 1 1.3878e-14

79 1.221e-14 1 1.6653e-15

80 1.5255e-15 1 1.1102e-16

Aggregate stop loss premiums can be computed as tail integrals of the survival function. Multiply by the units, 25.

In [16]: (kpw_9_5.density_df.S[::-1].cumsum()[::-1] * 25)[:8]

Out[16]:

loss

0.0 314.500000

1.0 290.750000

2.0 267.375000

3.0 244.584375

4.0 222.660625

5.0 201.551289

6.0 181.336613

7.0 162.117133

8.0 143.986712

Name: S, dtype: float64

Exercise 9.19. An insurance portfolio produces N = 0, 1, 3 claims with probabilities 0.5, 0.4, 0.1. Individual claim amounts are 1 or 10 with probability 0.9, 0.1. Individual claim amounts and N are mutually independent. Calculate the probability that the ratio of aggregate claims to expected claims will exceed 3.0.

In [17]: kpw_9_19 = build('agg KPW.9.19 dfreq [0 1 3] [.5 .4 .1] '

....: 'dsev [1 10] [.9 .1]')

....:

In [18]: qd(kpw_9_19)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.7 1.2857 1.4486

Sev 1.9 1.9 0 1.4211 1.4211 2.6667 2.6667

Agg 1.33 1.33 -9.992e-16 2.1302 2.1302 3.414 3.414

log2 = 6, bandwidth = 1, validation: not unreasonable.

In [19]: m = kpw_9_19.agg_m

In [20]: print(f'mean {m:.5g}\nprobability {kpw_9_19.sf(3 * m):.4g}')

mean 1.33

probability 0.0671

Exercise 9.23. An individual loss distribution is normal with mean = 100 and variance = 9. The distribution for the number of claims has outcomes 0, 1, 2, 3 with probabilities 0.5, 0.2, 0.2, 0.1. Determine the probability that aggregate claims exceed 100.

In [21]: kpw_9_23 = build('agg KPW.9.23 dfreq [0:3] [1/2 1/5 1/5 1/10] '

....: 'sev 3 * norm + 100')

....:

In [22]: qd(kpw_9_23)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.9 1.16 0.7276

Sev 100 100 -1.1102e-16 0.03 0.03 -5.174e-11 0

Agg 90 90 -1.1102e-15 1.1605 1.1605 0.72937 0.72937

log2 = 16, bandwidth = 1/32, validation: fails sev skew.

In [23]: qd(kpw_9_23.density_df.loc[90:110:64, ['p', 'F', 'S']])

p F S

loss

90.0 3.2132e-06 0.50009 0.49991

92.0 2.3742e-05 0.50078 0.49922

94.0 0.00011248 0.50461 0.49539

96.0 0.00034169 0.51841 0.48159

98.0 0.00066552 0.55083 0.44917

100.0 0.00083113 0.60042 0.39958

102.0 0.00066552 0.64983 0.35017

104.0 0.00034169 0.68193 0.31807

106.0 0.00011248 0.69551 0.30449

108.0 2.3742e-05 0.69925 0.30075

110.0 3.2132e-06 0.69992 0.30008

Exercise 9.24. An employer self-insures a life insurance program with the following two characteristics:

Given that a claim has occurred, the claim amount is 2,000 with probability 0.4 and 3,000 with probability 0.6.

The number of claims has outcomes 0, 1, 2, 3, 4 with probabilities 1/16, 1/4, 3/8, 1/4, 1/16.

The employer purchases aggregate stop-loss coverage that limits the employer’s annual claims cost to 5,000. The aggregate stop-loss coverage costs 1,472. Determine the employer’s expected annual cost of the program, including the cost of stop-loss coverage.

In [24]: kpw_9_24 = build('agg KPW.9.24 dfreq [0:4] [1/16 1/4 3/8 1/4 1/16] '

....: 'dsev [2 3] [0.4 0.6] '

....: 'aggregate net of inf xs 5')

....:

In [25]: qd(kpw_9_24)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2 0.5 0

Sev 2.6 2.6 0 0.18842 0.18842 -0.40825 -0.40825

Agg 5.2 4.0275 -0.22548 0.51745 0.36633 0.091166 -1.4019

log2 = 5, bandwidth = 1, validation: n/a, reinsurance.

In [26]: net = kpw_9_24.describe.iloc[-1, 1]

In [27]: print(f'\ngross loss {kpw_9_24.agg_m:.5g}\nretained loss {net:.5g}\n'

....: f'premium {net + 1.472:.5g}')

....:

gross loss 5.2

retained loss 4.0275

premium 5.4995

Working in thousands.

Exercise 9.31. Medical and dental claims are assumed to be independent with compound Poisson distributions as follows:

Medical claims 2 expected claims, amounts uniform (0, 1000)

Dental claims 3 expected claims, amounts uniform (0, 200)

Let X be the amount of a given claim under a policy that covers both medical and dental claims. Determine E[(X − 100)+], the expected cost (in excess of 100) of any given claim.

In [28]: kpw_9_31 = build('agg KPW.9.31 [2 3] claims '

....: 'sev [1000 200] * uniform '

....: 'occurrence ceded to inf xs 100 '

....: 'poisson')

....:

In [29]: qd(kpw_9_31)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 5 0.44721 0.44721

Sev 260 177 -0.31923 1.0444 1.461 1.3042 1.4244

Agg 1300 885 -0.31923 0.64664 0.79177 0.85178 0.95458

log2 = 16, bandwidth = 1/4, validation: n/a, reinsurance.

In [30]: qd(kpw_9_31.reinsurance_audit_df.stack(0).head(3))

ex var sd cv skew

kind share limit attach

occ 1.0 inf 100.0 ceded 177 66871 258.59 1.461 1.4244

net 83 844.34 29.057 0.35009 -1.5092

subject 260 73733 271.54 1.0444 1.3042

Could also compute impact of aggregate reinsurance structures.

Exercise 9.34. A compound Poisson distribution has 5 expected claim and claim amount distribution p(100) = 0.80, p(500) = 0.16, and p(1,000) = 0.04. Determine the probability that aggregate claims will be exactly 600.

In [31]: kpw_9_34 = build('agg KPW.9.34 5 claims '

....: 'dsev [1 5 10] [.8 .16 .04] '

....: 'poisson')

....:

In [32]: qd(kpw_9_34)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 5 0.44721 0.44721

Sev 2 2 -2.2204e-16 1.0954 1.0954 2.2822 2.2822

Agg 10 10 4.6629e-15 0.66332 0.66332 1.0416 1.0416

log2 = 10, bandwidth = 1, validation: not unreasonable.

In [33]: print(f'{kpw_9_34.pmf(6):.6g}')

0.0598929

In [34]: kpw_9_34.density_df.index = kpw_9_34.density_df.index.astype(int)

In [35]: qd(kpw_9_34.density_df.query('p > 0.001')[['p', 'F', 'S']], accuracy=5)

p F S

loss

0 0.0067379 0.0067379 0.99326

1 0.026952 0.03369 0.96631

2 0.053904 0.087593 0.91241

3 0.071871 0.15946 0.84054

4 0.071871 0.23134 0.76866

5 0.062888 0.29422 0.70578

6 0.059893 0.35412 0.64588

7 0.065027 0.41914 0.58086

8 0.068449 0.48759 0.51241

9 0.062365 0.54996 0.45004

10 0.051448 0.60141 0.39859

11 0.045388 0.64679 0.35321

... ... ... ...

23 0.0099885 0.95791 0.042093

24 0.0084688 0.96638 0.033624

25 0.0065328 0.97291 0.027091

26 0.0050132 0.97792 0.022078

27 0.0042014 0.98212 0.017877

28 0.0036975 0.98582 0.014179

29 0.0030698 0.98889 0.011109

30 0.0023339 0.99122 0.0087753

31 0.0017543 0.99298 0.007021

32 0.0014285 0.99441 0.0055925

33 0.0012267 0.99563 0.0043658

34 0.0010036 0.99664 0.0033621

Work in hundreds. Convert index to integer to improve display. Show all outcomes with probability greater than 0.001.

Exercise 9.35. Aggregate payments have a compound distribution. The frequency distribution is negative binomial with \(r = 16\) and \(\beta = 6\), and the severity distribution is uniform on the interval (0, 8). Use the normal approximation to determine the premium such that the probability is 5% that aggregate payments will exceed the premium.

The negative binomial has mean \(r\beta\) and variance \(r\beta(1+\beta)\). Therefore the gamma mixing variance equals \(c=1/r\) (since \(r\beta(1+\beta)=n(1+cn)\).) Hence the mixing cv equals 0.25. The premium is the 95%ile of the aggregate distribution.

In [36]: kpw_9_35 = build('agg KPW.9.35 96 claims '

....: 'sev 8 * uniform '

....: 'mixed gamma 0.25')

....:

In [37]: qd(kpw_9_35)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 96 0.27003 0.50149

Sev 4 4 0 0.57735 0.57736 0 0

Agg 384 384 3.3307e-15 0.27639 0.27639 0.50366 0.50366

log2 = 16, bandwidth = 1/32, validation: not unreasonable.

In [38]: mv(kpw_9_35)

mean = 384

variance = 11264

std dev = 106.132

In [39]: appx = kpw_9_35.approximate('all')

In [40]: ans = {k: v.isf(0.05) for k, v in appx.items()}

In [41]: ans['FFT'] = kpw_9_35.q(0.95)

In [42]: qd(pd.DataFrame(ans.values(),

....: index=pd.Index(ans.keys(), name='method'),

....: columns=['premium']).sort_values('premium'),

....: accuracy=4)

....:

premium

method

norm 558.57

slognorm 571.88

sgamma 572.4

FFT 572.41

gamma 573.6

lognorm 578.31

The approximate method returns a dictionary with key the method, for normal and shifted and unshifted gamma and lognormal.

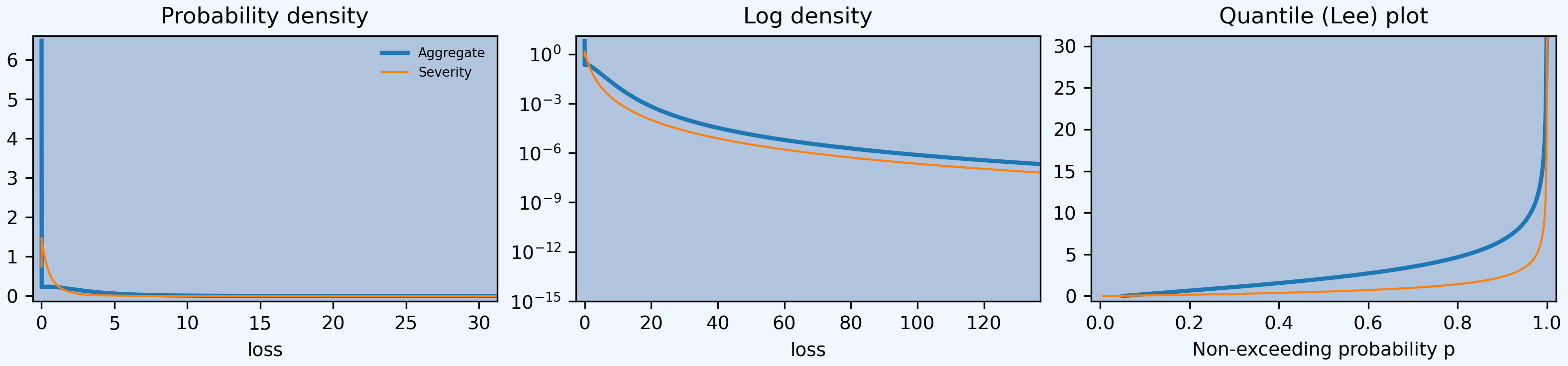

Exercise 9.36. The number of losses is Poisson with mean 3. Loss amounts have a Burr distribution with \(\alpha = 3\), \(\theta = 2\), and \(\gamma = 1\). Determine the variance of aggregate losses.

A matter of converting parameterizations. This is the scipy.stats burr12 distribution. The shape parameters are c=gamma and d=alpha. theta is a scale parameter.

In [43]: kpw_9_36 = build('agg KPW.9.36 3 claims '

....: 'sev 2 * burr12 1 3 '

....: 'poisson')

....:

In [44]: qd(kpw_9_36)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3 0.57735 0.57735

Sev 1 0.99995 -4.9059e-05 1.7321 1.7187 inf 15.681

Agg 3 2.9999 -4.9063e-05 1.1547 1.148 inf 6.5701

log2 = 16, bandwidth = 1/128, validation: fails sev cv, agg cv.

In [45]: mv(kpw_9_36)

mean = 3

variance = 12

std dev = 3.4641

In [46]: kpw_9_36.plot()

2.13.5.4. Compound Poisson, Example 9.9, 9.10

Policy A has a compound Poisson distribution with 2 expected claims and severity probabilities 0.6 on a payment of 1 and 0.4 on a payment of 2. Policy B has a compound Poisson distribution with 1 expected claim and probabilities 0.7 on a payment of 1 and 0.3 on a payment of 3.

Determine the probability that the total payment on the two policies will be 2.

Figure the weighted severity by hand.

In [47]: kpw_9_9 = build('agg KPW.9.9 3 claims '

....: 'dsev [1 2 3] [1.9/3 .8/3 .3/3] '

....: 'poisson')

....:

In [48]: qd(kpw_9_9)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3 0.57735 0.57735

Sev 1.4667 1.4667 -1.1102e-16 0.45681 0.45681 1.1192 1.1192

Agg 4.4 4.4 0 0.63474 0.63474 0.75284 0.75284

log2 = 7, bandwidth = 1, validation: not unreasonable.

In [49]: print(f'{kpw_9_9.pmf(2):.6g}')

0.129695

In [50]: kpw_9_9.density_df.index = kpw_9_9.density_df.index.astype(int)

In [51]: bit = kpw_9_9.density_df.query('p > 0.001')[['p', 'F', 'S']]

In [52]: bit['p*exp(3)'] = bit.p * np.exp(3)

In [53]: qd(bit, accuracy=5)

p F S p*exp(3)

loss

0 0.049787 0.049787 0.95021 1

1 0.094595 0.14438 0.85562 1.9

2 0.1297 0.27408 0.72592 2.605

3 0.14753 0.42161 0.57839 2.9632

4 0.14324 0.56484 0.43516 2.877

5 0.12498 0.68983 0.31017 2.5104

6 0.099904 0.78973 0.21027 2.0066

7 0.074101 0.86383 0.13617 1.4884

8 0.051641 0.91547 0.084527 1.0372

9 0.034066 0.94954 0.050462 0.68423

10 0.021404 0.97094 0.029058 0.42991

11 0.012877 0.98382 0.01618 0.25865

12 0.0074477 0.99127 0.0087326 0.14959

13 0.0041552 0.99542 0.0045774 0.08346

14 0.0022429 0.99767 0.0023345 0.04505

15 0.0011742 0.99884 0.0011603 0.023584

The last column answers Example 9.10.

Alternatively, use the Portfolio class.

In [54]: p = build('port KPW.9.9.p '

....: 'agg A 2 claims dsev [1 2] [.6 .4] poisson '

....: 'agg B 1 claims dsev [1 3] [.7 .3] poisson')

....:

In [55]: qd(p)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

A Freq 2 0.70711 0.70711

Sev 1.4 1.4 0 0.34993 0.34993 0.40825 0.40825

Agg 2.8 2.8 6.6613e-16 0.74915 0.74915 0.82344 0.82344

B Freq 1 1 1

Sev 1.6 1.6 2.2204e-16 0.57282 0.57282 0.87287 0.87287

Agg 1.6 1.6 8.8818e-16 1.1524 1.1524 1.4037 1.4037

total Freq 3 0.57735 0.57735

Sev 1.4667 1.4667 2.2204e-16 0.45681 1.1192

Agg 4.4 4.4 -1.6653e-15 0.63474 0.63474 0.75284 0.75284

log2 = 16, bandwidth = 1/1024, validation: not unreasonable.

Exercise 9.39. For a compound distribution, frequency has a binomial distribution with parameters m = 3 and q = 0.4 and severity has an exponential distribution with a mean of 100. Calculate \(\Pr(A \le 300)\).

Assume 1.2 expected claims. Work in hundreds.

In [56]: kpw_9_39 = build('agg KPW.9.39 1.2 claims '

....: 'sev expon binomial 0.4')

....:

In [57]: qd(kpw_9_39)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1.2 0.70711 0.2357

Sev 1 1 -3.9736e-08 1 1 2 2

Agg 1.2 1.2 -3.9736e-08 1.1547 1.1547 1.7681 1.7681

log2 = 16, bandwidth = 1/1024, validation: not unreasonable.

In [58]: print(f'probability = {kpw_9_39.cdf(3):.6g}')

probability = 0.894092

Exercise 9.40. A company sells three policies. For policy A, all claim payments are 10,000 and a single policy has a Poisson number of claims with mean 0.01. For policy B, all claim payments are 20,000 and a single policy has a Poisson number of claims with mean 0.02. For policy C, all claim payments are 40,000 and a single policy has a Poisson number of claims with mean 0.03. All policies are independent. For the coming year, there are 5,000, 3,000, and 1,000 of policies A, B, and C, respectively. Calculate the expected total payment, the standard deviation of total payment, and the probability that total payments will exceed 30,000.

Must use a Portfolio. Work in thousands.

In [59]: kpw_9_40 = build('port kpw_9_40\n'

....: '\tagg A 50 claims dsev [10] poisson\n'

....: '\tagg B 60 claims dsev [20] poisson\n'

....: '\tagg C 30 claims dsev [40] poisson\n')

....:

In [60]: qd(kpw_9_40)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

A Freq 50 0.14142 0.14142

Sev 10 10 0 0 0

Agg 500 500 1.9984e-15 0.14142 0.14142 0.14142 0.14142

B Freq 60 0.1291 0.1291

Sev 20 20 0 0 0

Agg 1200 1200 -6.1062e-15 0.1291 0.1291 0.1291 0.1291

C Freq 30 0.18257 0.18257

Sev 40 40 0 0 0

Agg 1200 1200 -2.2204e-15 0.18257 0.18257 0.18257 0.18257

total Freq 140 0.084515 0.084515

Sev 20.714 20.714 0 0.53086 0.82553

Agg 2900 2899.9 -4.1178e-05 0.095686 0.095811 0.11466 0.08019

log2 = 16, bandwidth = 1/16, validation: fails agg cv.

In [61]: qd(pd.Series({'expected payment': kpw_9_40.agg_m,

....: 'sd payment': kpw_9_40.agg_sd,

....: 'Pr > 3000': kpw_9_40.sf(3000)}).to_frame('value'),

....: accuracy=5)

....:

value

expected payment 2900

sd payment 277.49

Pr > 3000 0.34658

2.13.5.5. ZM Binomial, Example 9.11

A compound distribution has a zero-modified binomial distribution with 𝑚 = 3, \(q = 0.3\), and \(p_0^M = 0.4\). Individual payments are 0, 50, and 150, with probabilities 0.3, 0.5, and 0.2, respectively. Use the recursive formula to determine the probability distribution of \(S\).

Todo

Implement ZM and ZT.

2.13.5.6. ETNB, Example 9.12

The number of claims has a Poisson–ETNB distribution with Poisson parameter 𝜆 = 2 and ETNB parameters \(\beta = 3\) and \(r = 0.2\). The claim size distribution has probabilities 0.3, 0.5, and 0.2 at 0, 10, and 20, respectively. Determine the total claims distribution recursively.

Todo

Implement ZM and ZT.

Exercise 9.45. For a compound Poisson distribution, has 6 expected claims and individual losses take values 1, 2, 4 with equal probabilities. Determine the distribution of the aggregate.

In [62]: kpw_9_45 = build('agg KPW.9.45 6 claims '

....: 'dsev [1 2 4] poisson')

....:

In [63]: qd(kpw_9_45)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 6 0.40825 0.40825

Sev 2.3333 2.3333 2.2204e-16 0.53452 0.53452 0.3818 0.3818

Agg 14 14 4.6629e-15 0.46291 0.46291 0.53639 0.53639

log2 = 9, bandwidth = 1, validation: not unreasonable.

In [64]: qd(kpw_9_45.density_df.query('p > 0.001')[['p', 'F', 'S']], accuracy=5)

p F S

loss

0.0 0.0024788 0.0024788 0.99752

1.0 0.0049575 0.0074363 0.99256

2.0 0.009915 0.017351 0.98265

3.0 0.01322 0.030571 0.96943

4.0 0.021483 0.052054 0.94795

5.0 0.027101 0.079155 0.92085

6.0 0.036575 0.11573 0.88427

7.0 0.041045 0.15678 0.84322

8.0 0.050031 0.20681 0.79319

9.0 0.05345 0.26026 0.73974

10.0 0.059963 0.32022 0.67978

11.0 0.06019 0.38041 0.61959

... ... ... ...

24.0 0.017373 0.93502 0.064978

25.0 0.014016 0.94904 0.050962

26.0 0.011474 0.96051 0.039488

27.0 0.0090615 0.96957 0.030427

28.0 0.0072502 0.97682 0.023176

29.0 0.0056163 0.98244 0.01756

30.0 0.0044008 0.98684 0.013159

31.0 0.0033471 0.99019 0.0098123

32.0 0.0025718 0.99276 0.0072405

33.0 0.0019231 0.99468 0.0053174

34.0 0.0014512 0.99613 0.0038662

35.0 0.0010677 0.9972 0.0027985

Exercise 9.47. Aggregate claims are compound Poisson with 2 expected claims and severity outcomes 1, 2 with probability 1/4 and 3/4. For a premium of 6, an insurer covers aggregate claims and agrees to pay a dividend (a refund of premium) equal to the excess, if any, of 75% of the premium over 100% of the claims. Determine the excess of premium over expected claims and dividends.

In [65]: kpw_9_47 = build('agg KPW.9.47 2 claims '

....: 'dsev [1 2] [1/4 3/4] poisson')

....:

In [66]: qd(kpw_9_47)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2 0.70711 0.70711

Sev 1.75 1.75 0 0.24744 0.24744 -1.1547 -1.1547

Agg 3.5 3.5 2.2204e-16 0.72843 0.72843 0.75429 0.75429

log2 = 6, bandwidth = 1, validation: not unreasonable.

In [67]: bit = kpw_9_47.density_df.query('p > 0')[['p', 'F', 'S']]

In [68]: bit['dividend'] = np.maximum(0.75 * 6 - bit.index, 0)

In [69]: qd(bit.head(10), accuracy=4)

p F S dividend

loss

0.0 0.13534 0.13534 0.86466 4.5

1.0 0.067668 0.203 0.797 3.5

2.0 0.21992 0.42292 0.57708 2.5

3.0 0.10432 0.52724 0.47276 1.5

4.0 0.17798 0.70522 0.29478 0.5

5.0 0.080391 0.78561 0.21439 0

6.0 0.095689 0.8813 0.1187 0

7.0 0.041288 0.92259 0.077408 0

8.0 0.038464 0.96106 0.038945 0

9.0 0.0159 0.97696 0.023045 0

In [70]: exp_div = (bit.dividend * bit.p).sum()

In [71]: print(f'prem = {6:.5g}\n'

....: f'exp loss = {kpw_9_47.agg_m:.5g}\n'

....: f'dividend = {exp_div:.5g}\n'

....: f'excess = {6 - kpw_9_47.agg_m - exp_div:.5g}')

....:

prem = 6

exp loss = 3.5

dividend = 1.6411

excess = 0.85888

Exercise 9.57, 9.58. Aggregate losses have a compound Poisson claim distribution with 3 expected claims and individual claim amount distribution p(1) = 0.4, p(2) = 0.3, p(3) = 0.2, and p(4) = 0.1. Determine the probability that aggregate losses do not exceed 3.

Repeat the Exercise with a negative binomial frequency distribution with r = 6 and \(\beta = 0.5\).

In [72]: kpw_9_57 = build('agg KPW.9.57 3 claims '

....: 'dsev [1:4] [.4 .3 .2 .1] poisson')

....:

In [73]: qd(kpw_9_57)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3 0.57735 0.57735

Sev 2 2 -3.3307e-16 0.5 0.5 0.6 0.6

Agg 6 6 -1.1102e-16 0.6455 0.6455 0.75394 0.75394

log2 = 8, bandwidth = 1, validation: not unreasonable.

In [74]: kpw_9_58 = build('agg KPW.9.58 3 claims '

....: 'dsev [1:4] [.4 .3 .2 .1] mixed gamma 6**-0.5')

....:

In [75]: qd(kpw_9_58)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3 0.70711 0.94281

Sev 2 2 -3.3307e-16 0.5 0.5 0.6 0.6

Agg 6 6 -7.6605e-15 0.76376 0.76376 1.0474 1.0474

log2 = 8, bandwidth = 1, validation: not unreasonable.

In [76]: bit = pd.concat((kpw_9_57.density_df[['p', 'F', 'S']],

....: kpw_9_58.density_df[['p', 'F', 'S']]),

....: keys=('Po', 'NB'), axis=1)

....:

In [77]: qd(bit.head(16), accuracy=5)

Po NB

p F S p F S

loss

0.0 0.049787 0.049787 0.95021 0.087791 0.087791 0.91221

1.0 0.059744 0.10953 0.89047 0.070233 0.15802 0.84198

2.0 0.080655 0.19019 0.80981 0.08545 0.24348 0.75652

3.0 0.097981 0.28817 0.71183 0.095933 0.33941 0.66059

4.0 0.10751 0.39568 0.60432 0.098486 0.43789 0.56211

5.0 0.10445 0.50013 0.49987 0.089535 0.52743 0.47257

6.0 0.098668 0.5988 0.4012 0.082877 0.61031 0.38969

7.0 0.088215 0.68701 0.31299 0.073657 0.68396 0.31604

8.0 0.07506 0.76207 0.23793 0.063257 0.74722 0.25278

9.0 0.061311 0.82338 0.17662 0.05302 0.80024 0.19976

10.0 0.048587 0.87197 0.12803 0.043819 0.84406 0.15594

11.0 0.037239 0.90921 0.09079 0.035507 0.87957 0.12043

12.0 0.027715 0.93692 0.063075 0.028316 0.90789 0.092115

13.0 0.020101 0.95703 0.042974 0.022288 0.93017 0.069827

14.0 0.014239 0.97127 0.028735 0.017338 0.94751 0.052489

15.0 0.0098562 0.98112 0.018879 0.013334 0.96085 0.039155

Exercise 9.59. A policy covers physical damage incurred by the trucks in a company’s fleet. The number of losses in a year has a Poisson distribution with expectation 5. The amount of a single loss has a gamma distribution with shape 0.5 and scale 2,500. The insurance contract pays a maximum annual benefit of 20,000. Determine the probability that the maximum benefit will be paid. Use a span of 100 and the method of rounding.

In [78]: kpw_9_59 = build('agg KPW.9.59 5 claims '

....: 'sev 2500 * gamma 0.5 '

....: 'poisson')

....:

In [79]: qd(kpw_9_59)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 5 0.44721 0.44721

Sev 1250 1250 -3.109e-06 1.4142 1.4142 2.8284 2.8284

Agg 6250 6250 -3.109e-06 0.7746 0.7746 1.291 1.291

log2 = 16, bandwidth = 2, validation: not unreasonable.

In [80]: print(f'pr(loss >= 20000) = {kpw_9_59.sf(20000):.6g}')

pr(loss >= 20000) = 0.015939

Repeated at the requested span of 100.

In [81]: kpw_9_59.update(log2=10, bs=100)

In [82]: print(f'pr(loss >= 20000) = {kpw_9_59.sf(20000):.6g}')

pr(loss >= 20000) = 0.0157042

Exercise 9.60. An individual has purchased health insurance, for which they pay 10 for each physician visit and 5 for each prescription. The probability that a payment will be 10 is 0.25, and the probability that it will be 5 is 0.75. The total number of payments per year has the Poisson–Poisson (Neyman Type A) distribution with primary mean 10 and secondary mean 4. Determine the probability that total payments in one year will exceed 400. Compare your answer to a normal approximation.

In [83]: kpw_9_60 = build('agg KPW.9.60 40 claims '

....: 'dsev [5 10] [3/4 1/4] '

....: 'neyman 4')

....:

In [84]: qd(kpw_9_60)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 40 0.35355 0.41012

Sev 6.25 6.25 0 0.34641 0.34641 1.1547 1.1547

Agg 250 250 -9.1038e-14 0.35777 0.35777 0.42101 0.42101

log2 = 14, bandwidth = 1, validation: not unreasonable.

In [85]: fz = kpw_9_60.approximate('norm')

In [86]: print(f'FFT {kpw_9_60.sf(400):.5g}\n'

....: f'Normal approx {fz.sf(400):.5g}')

....:

FFT 0.054616

Normal approx 0.046766

2.13.5.7. Poisson Pareto, Example 9.14

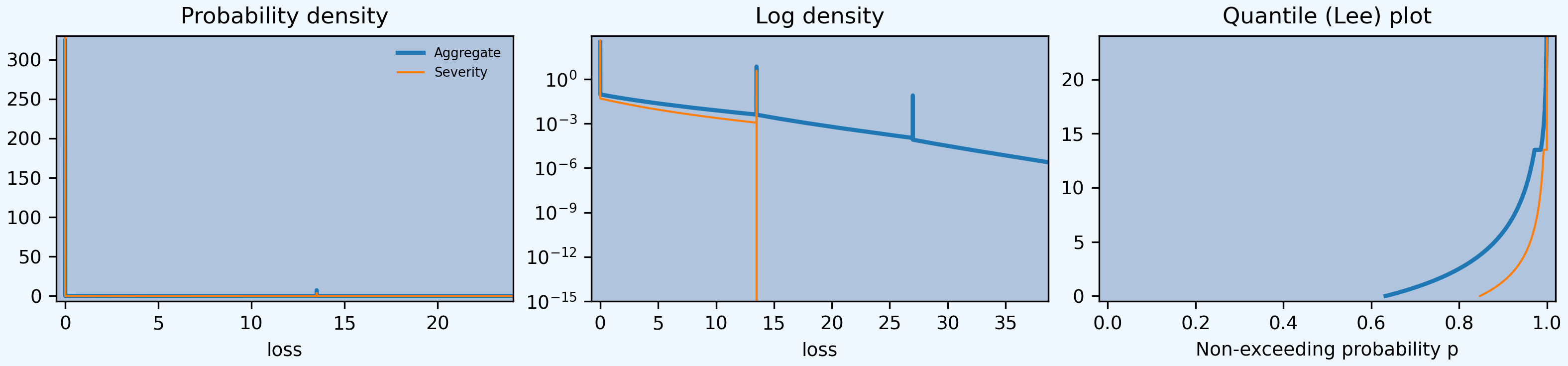

The number of ground-up losses is Poisson distributed with mean 3. The individual loss distribution is Pareto with shape parameter :math:alpha= 4` and scale parameter 10. An individual ordinary deductible of 6, coinsurance of 75%, and an individual loss limit of 24 (before application of the deductible and coinsurance) are all applied. Determine the mean, variance, and distribution of aggregate payments.

The covered layer is 18 xs 6, in which the insured pays 25% because of the coinsurance clause. The severity is unconditional.

In [87]: kpw_9_14 = build('agg KPW.9.14 3 claims '

....: '18 xs 6 '

....: 'sev 10 * pareto 4 - 10 ! '

....: 'occurrence net of 0.25 so inf xs 0 '

....: 'poisson')

....:

In [88]: qd(kpw_9_14)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3 0.57735 0.57735

Sev 0.72899 0.54678 -0.24995 3.5115 3.5113 4.6513 4.6511

Agg 2.187 1.6403 -0.24995 2.108 2.1079 2.8396 2.8395

log2 = 16, bandwidth = 1/512, validation: n/a, reinsurance.

In [89]: print(f'variance = {kpw_9_14.describe.iloc[-1,[1, 4]].prod()**2:.6g}\ncomputed with bs=1/{1/kpw_9_14.bs:.0f} and log2={kpw_9_14.log2}')

variance = 11.9552

computed with bs=1/512 and log2=16

In [90]: qd(kpw_9_14.density_df.loc[[0, 1, 2, 3], ['p', 'F', 'S']])

p F S

loss

0.0 0.63277 0.63277 0.36723

1.0 0.00013621 0.71496 0.28504

2.0 0.00010097 0.7751 0.2249

3.0 7.6416e-05 0.82013 0.17987

In [91]: kpw_9_14.plot()

describe returns gross under E[X] and the requested net or ceded under Est E[X]. The print statement computes net variance from the product of estimated mean and cv. The spikes on the density corresponds to the possibility of only limit claims.

Exercise 9.63. A ground-up model of individual losses has a gamma distribution with shape parameter 2 and scale 100. The number of losses has a negative binomial distribution with \(r = 2\) and \(\beta = 1.5\). An ordinary deductible of 50 and a loss limit of 175 (before imposition of the deductible) are applied to each individual loss.

Determine the mean and variance of the aggregate payments on a per-loss basis.

Determine the distribution of the number of payments.

Determine the cumulative distribution function of the amount of a payment, given that a payment is made.

Discretize the severity distribution using the method of rounding and a span of 40.

Calculate the discretized distribution of aggregate payments up to a discretized amount paid of 120.

Negative binomial \(c=1/2\) and hence mixing cv \(\sqrt{c}\), and the mean equals \(r\beta/(1+\beta)=1.4\). The cover is 125 xs 50. The severity is unconditional. First, the default calculation using bs=1/64.

In [92]: kpw_9_63 = build('agg KPW.9.63 1.4 claims '

....: '125 xs 50 '

....: 'sev 100 * gamma 2 ! '

....: 'mixed gamma 2**-0.5')

....:

In [93]: qd(kpw_9_63)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1.4 1.1019 1.5557

Sev 86.467 86.467 3.9488e-12 0.54006 0.54006 -0.74977 -0.74977

Agg 121.05 121.05 -3.9543e-08 1.1927 1.1927 1.6385 1.6385

log2 = 16, bandwidth = 1/32, validation: fails agg mean error >> sev, possible aliasing; try larger bs.

In [94]: mv(kpw_9_63)

mean = 121.054

variance = 20847.33

std dev = 144.386

In [95]: qd(kpw_9_63.density_df.loc[:400:40*64,

....: ['p', 'F', 'S', 'p_sev', 'F_sev', 'S_sev']],

....: accuracy=5)

....:

p F S p_sev F_sev S_sev

loss

0.0 0.37325 0.37325 0.62675 0.090251 0.090251 0.90975

80.0 4.2253e-05 0.47185 0.52815 0.00011072 0.37323 0.62677

160.0 3.327e-05 0.72045 0.27955 0 1 0

240.0 3.0211e-05 0.80373 0.19627 0 1 0

320.0 1.7591e-05 0.9016 0.098397 0 1 0

400.0 9.0878e-06 0.94991 0.050095 0 1 0

Next, calculations performed with the requested broader bs=40.

In [96]: kpw_9_63.update(log2=8, bs=40)

In [97]: qd(kpw_9_63)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1.4 1.1019 1.5557

Sev 86.467 84.042 -0.02805 0.54006 0.546 -0.74977 -0.81723

Agg 121.05 117.66 -0.02805 1.1927 1.1947 1.6385 1.636

log2 = 8, bandwidth = 40, validation: fails sev mean, agg mean.

In [98]: qd(kpw_9_63.density_df.loc[:400,

....: ['p', 'F', 'S', 'p_sev', 'F_sev', 'S_sev']],

....: accuracy=5)

....:

p F S p_sev F_sev S_sev

loss

0.0 0.39509 0.39509 0.60491 0.1558 0.1558 0.8442

40.0 0.05047 0.44556 0.55444 0.14517 0.30097 0.69903

80.0 0.053928 0.49949 0.50051 0.1412 0.44217 0.55783

120.0 0.20376 0.70325 0.29675 0.55783 1 0

160.0 0.042972 0.74622 0.25378 0 1 0

200.0 0.042194 0.78841 0.21159 0 1 0

240.0 0.081719 0.87013 0.12987 0 1 0

280.0 0.024403 0.89453 0.10547 0 1 0

320.0 0.02234 0.91687 0.083127 0 1 0

360.0 0.030181 0.94705 0.052946 0 1 0

400.0 0.011572 0.95863 0.041374 0 1 0

The apparent difference in the severity distribution is caused by the rounding method. In the first case F(40) is almost exact whereas in the second it is actually F(60).

2.13.5.8. Group Life Individual Risk Model, Example 9.15, 9.18

Consider a group life insurance contract with an accidental death benefit. Assume that for all members the probability of death in the next year is 0.01 and that 30% of deaths are accidental. For 50 employees, the benefit for an ordinary death is 50,000 and for an accidental death it is 100,000. For the remaining 25 employees, the benefits are 75,000 and 150,000, respectively. Develop an individual risk model and determine its mean and variance.

The Portfolio solution, working in thousands.

In [99]: kpw_9_15p = build('port KPW.9.15.p '

....: 'agg A 0.5 claims '

....: 'dsev [50 100] [0.7 0.3] '

....: 'binomial 0.01 '

....: 'agg B 0.25 claims '

....: 'dsev [75 150] [0.7 0.3] '

....: 'binomial 0.01 ')

....:

In [100]: qd(kpw_9_15p)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

A Freq 0.5 1.4071 1.3929

Sev 65 65 0 0.35251 0.35251 0.87287 0.87287

Agg 32.5 32.5 2.82e-14 1.4928 1.4928 1.6562 1.6562

B Freq 0.25 1.99 1.9699

Sev 97.5 97.5 0 0.35251 0.35251 0.87287 0.87287

Agg 24.375 24.375 1.1613e-13 2.1112 2.1112 2.3423 2.3423

total Freq 0.75 1.1489 1.1373

Sev 75.833 75.833 0 0.41249 1.1623

Agg 56.875 56.875 -8.6597e-15 1.2435 1.2435 1.4369 1.4369

log2 = 16, bandwidth = 1/16, validation: not unreasonable.

In [101]: mv(kpw_9_15p)

mean = 56.875

variance = 5001.984

std dev = 70.7247

The density_df dataframe contains the exact aggregate distribution, which is not easy to compute by other means. KPW says (emphasis added)

With regard to calculating the probabilities, there are at least three options. One is to do an exact calculation, which involves numerous convolutions and almost always requires more excessive computing time. Recursive formulas have been developed, but they are cumbersome and are not presented here. For one such method, see De Pril [27]. One alternative is a parametric approximation as discussed for the collective risk model. Another alternative is to replace the individual risk model with a similar collective risk model and then do the calculations with that model. These two approaches are presented here.

The following solution attempts to commute convolution through the mixture. This works for a compound Poisson. However, the sum of binomials is not binomial, and so the frequencies can’t be independent binomial. They can be independent Poisson because it is additive.

In [102]: kpw_9_15w = build('agg KPW.9.15.w '

.....: '0.75 claims '

.....: 'dsev [50 75 100 150] '

.....: '[0.35/0.75, 0.175/0.75, 0.15/0.75, 0.075/0.75] '

.....: 'binomial 0.01 ')

.....:

In [103]: qd(kpw_9_15w)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.75 1.1489 1.1373

Sev 75.833 75.833 2.2204e-16 0.41249 0.41249 1.1623 1.1623

Agg 56.875 56.875 -6.9356e-11 1.2437 1.2437 1.4389 1.4389

log2 = 10, bandwidth = 1, validation: fails agg mean error >> sev, possible aliasing; try larger bs.

In [104]: mv(kpw_9_15w)

mean = 56.875

variance = 5003.745

std dev = 70.7372

The compound Poisson approximation matches the mean but its variance is slightly off.

In [105]: kpw_9_15cp = build('agg KPW.9.15.cp '

.....: '0.75 claims '

.....: 'dsev [50 75 100 150] '

.....: '[0.35/0.75, 0.175/0.75, 0.15/0.75, 0.075/0.75] '

.....: 'poisson ')

.....:

In [106]: qd(kpw_9_15cp)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.75 1.1547 1.1547

Sev 75.833 75.833 2.2204e-16 0.41249 0.41249 1.1623 1.1623

Agg 56.875 56.875 -1.1396e-10 1.2491 1.2491 1.4523 1.4523

log2 = 10, bandwidth = 1, validation: fails agg mean error >> sev, possible aliasing; try larger bs.

In [107]: mv(kpw_9_15cp)

mean = 56.875

variance = 5046.875

std dev = 71.0414

Comparing probabilities shows that all three distributions are very close.

In [108]: bit = pd.concat((kpw_9_15p.density_df.loc[:400:128, ['p_total']].query('p_total > 1e-10'),

.....: kpw_9_15cp.density_df.loc[:400, ['p_total']].query('p_total > 0'),

.....: kpw_9_15w.density_df.loc[:400, ['p_total']].query('p_total > 0'),

.....: ),

.....: keys=('exact', 'compound Po', 'wrong'), axis=1).rename(columns={'p_total': 'p'})

.....:

In [109]: bit = bit.droplevel(1, axis=1)

In [110]: bit.index.name = 'loss'

In [111]: qd(bit, accuracy=5)

exact compound Po wrong

loss

0.0 0.47059 0.47237 0.47059

200.0 0.024856 0.024881 0.024823

400.0 0.00061615 0.00064447 0.00061581

50.0 NaN 0.16533 0.16637

75.0 NaN 0.082664 0.083185

100.0 NaN 0.099787 0.10032

125.0 NaN 0.028932 0.029017

150.0 NaN 0.070835 0.071104

175.0 NaN 0.017463 0.017428

225.0 NaN 0.011552 0.011478

250.0 NaN 0.011399 0.0113

275.0 NaN 0.0040587 0.0039712

300.0 NaN 0.0050707 0.004986

325.0 NaN 0.0018166 0.0017595

350.0 NaN 0.001694 0.0016392

375.0 NaN 0.00077117 0.00073805

2.13.5.9. Group Life Individual Risk Model, Example 9.16, 9.17

A small manufacturing business has a group life insurance contract on its 14 permanent employees. The actuary for the insurer has selected a mortality table to represent the mortality of the group. Each employee is insured for the amount of his or her salary rounded up to the next 1,000. The group’s data are shown in the next table.

If the insurer adds a 45% relative loading to the net (pure) premium, what are the chances that it will lose money in a given year? Use the normal and lognormal approximations.

In order to make the answer self-contained, the code below includes the data munging to re-create the table, pasted from a pdf.

In [112]: data = '''1

.....: 20

.....: M

.....: 15,000

.....: 0.00149

.....: 2

.....: 23

.....: M

.....: 16,000

.....: 0.00142

.....: 3

.....: 27

.....: M

.....: 20,000

.....: 0.00128

.....: 4

.....: 30

.....: M

.....: 28,000

.....: 0.00122

.....: 5

.....: 31

.....: M

.....: 31,000

.....: 0.00123

.....: 6

.....: 46

.....: M

.....: 18,000

.....: 0.00353

.....: 7

.....: 47

.....: M

.....: 26,000

.....: 0.00394

.....: 8

.....: 49

.....: M

.....: 24,000

.....: 0.00484

.....: 9

.....: 64

.....: M

.....: 60,000

.....: 0.02182

.....: 10

.....: 17

.....: F

.....: 14,000

.....: 0.00050

.....: 11

.....: 22

.....: F

.....: 17,000

.....: 0.00050

.....: 12

.....: 26

.....: F

.....: 19,000

.....: 0.00054

.....: 13

.....: 37

.....: F

.....: 30,000

.....: 0.00103

.....: 14

.....: 55

.....: F

.....: 55,000

.....: 0.00479'''

.....:

In [113]: sdata = data.split('\n')

In [114]: df = pd.DataFrame(zip(*[iter(sdata)]*5),

.....: columns=['Employee', 'Age', 'Sex', 'Benefit', 'q'])

.....:

In [115]: df.Benefit = df.Benefit.str.replace(',','').astype(float)

In [116]: df.q = df.q.astype(float)

In [117]: df = df.set_index('Employee')

In [118]: qd(df)

Age Sex Benefit q

Employee

1 20 M 15000 0.00149

2 23 M 16000 0.00142

3 27 M 20000 0.00128

4 30 M 28000 0.00122

5 31 M 31000 0.00123

6 46 M 18000 0.00353

7 47 M 26000 0.00394

8 49 M 24000 0.00484

9 64 M 60000 0.02182

10 17 F 14000 0.0005

11 22 F 17000 0.0005

12 26 F 19000 0.00054

13 37 F 30000 0.00103

14 55 F 55000 0.00479

In [119]: print(f'expected claim count = {df.q.sum():.6g}')

expected claim count = 0.04813

Here are the FFT-exact, and various approximations to the required probability. Working in thousands. The dsev clauses enter the fixed benefit amount for each employee. Note the outsize impact of employee 9.

In [120]: from aggregate import Portfolio

In [121]: a = [build(f'agg ee.{i} {r.q} claims '

.....: f'dsev [{r.Benefit / 1000}] '

.....: f'bernoulli')

.....: for i, r in df.iterrows()]

.....:

In [122]: kpw_9_16p = Portfolio('KPW.9.16p', a)

In [123]: kpw_9_16p.update(log2=8, bs=1, remove_fuzz=True)

In [124]: qd(kpw_9_16p)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

ee.1 Freq 0.00149 25.887 25.848

Sev 15 15 -1.1102e-16 0 0

Agg 0.02235 0.02235 8.8818e-16 25.887 25.887 25.848 25.848

ee.2 Freq 0.00142 26.518 26.481

Sev 16 16 0 0 0

Agg 0.02272 0.02272 -1.481e-13 26.518 26.518 26.481 26.481

ee.3 Freq 0.00128 27.933 27.897

Sev 20 20 0 0 0

Agg 0.0256 0.0256 -8.7597e-14 27.933 27.933 27.897 27.897

ee.4 Freq 0.00122 28.612 28.577

Sev 28 28 2.2204e-16 0 0

Agg 0.03416 0.03416 3.908e-14 28.612 28.612 28.577 28.577

... ... ... ... ... ... ... ...

ee.12 Freq 0.00054 43.022 42.998

Sev 19 19 0 0 0

Agg 0.01026 0.01026 1.35e-13 43.022 43.022 42.998 42.998

ee.13 Freq 0.00103 31.143 31.111

Sev 30 30 0 0 0

Agg 0.0309 0.0309 -4.2188e-15 31.143 31.143 31.111 31.111

ee.14 Freq 0.00479 14.414 14.345

Sev 55 55 -1.1102e-16 0 0

Agg 0.26345 0.26345 -2.1538e-14 14.414 14.414 14.345 14.345

total Freq 0.04813 4.5315 4.4789

Sev 42.685 42.685 0 0.43586 -0.28928

Agg 2.0544 2.0544 -5.9397e-14 4.9289 4.9289 5.2673 5.2673

log2 = 8, bandwidth = 1, validation: not unreasonable.

In [125]: mv(kpw_9_16p)

mean = 2.05441

variance = 102.5336

std dev = 10.1259

In [126]: appx = kpw_9_16p.approximate('all')

In [127]: premium = 1.45 * kpw_9_16p.agg_m

In [128]: ans = {k: v.sf(premium) for k, v in appx.items()}

In [129]: ans['FFT'] = kpw_9_16p.sf(premium)

In [130]: qd(pd.DataFrame(ans.values(),

.....: index=pd.Index(ans.keys(), name='method'),

.....: columns=['premium']).sort_values('premium'),

.....: accuracy=5)

.....:

premium

method

FFT 0.047261

gamma 0.091498

lognorm 0.13449

sgamma 0.18346

slognorm 0.28099

norm 0.46363

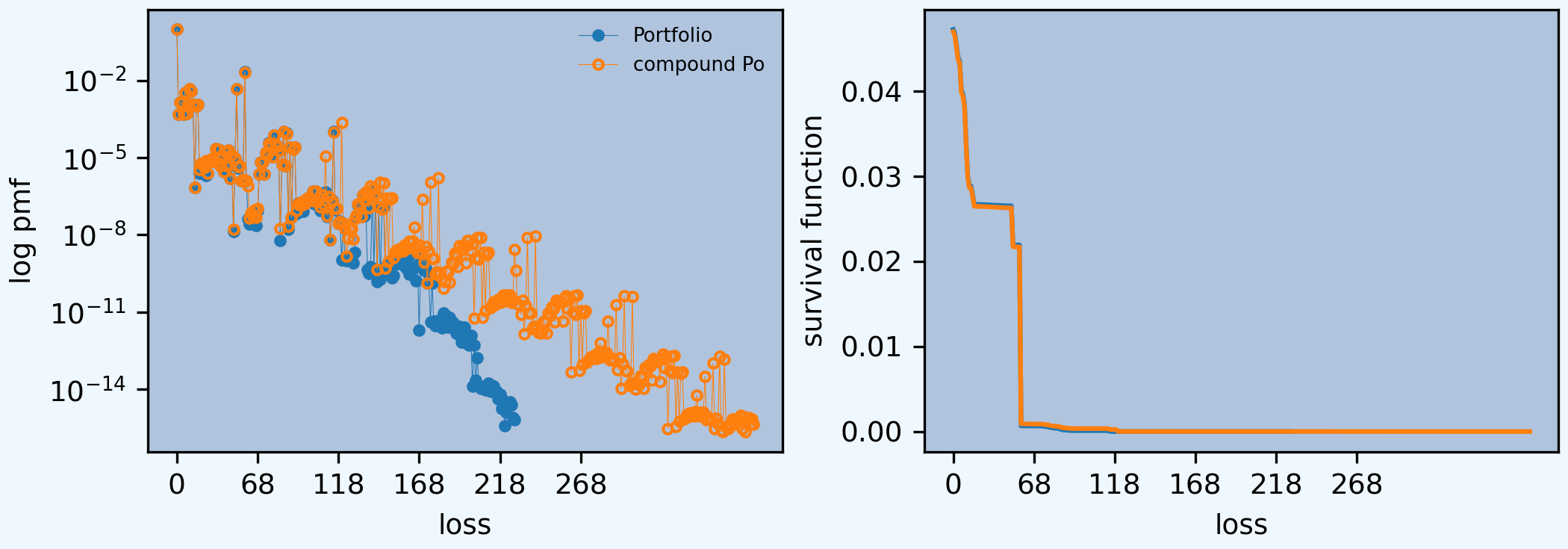

Here is a sample from the distribution and the mean-matched compound Poisson (for Exercise 9.18). The latter dsev clause works because all the benefit amounts are different. The temporary variable sev creates the severity curve. The log pmf graph reflects the irregular benefit amounts. Compare the cdf under comp Po with Table 9.17.

In [131]: sev = df[['Benefit', 'q']]

In [132]: sev.q = sev.q / sev.q.sum()

In [133]: sev = sev.sort_values('Benefit')

In [134]: kpw_9_16cp = build('agg kpw_9_16.po '

.....: f'{df.q.sum()} claims '

.....: f'dsev {sev.Benefit.values / 1000} {sev.q.values} '

.....: 'poisson', bs=1, log2=10)

.....:

In [135]: qd(kpw_9_16cp)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.04813 4.5582 4.5582

Sev 42.685 42.685 0 0.43586 0.43586 -0.28928 -0.28928

Agg 2.0544 2.0544 3.4417e-14 4.9723 4.9723 5.4286 5.4286

log2 = 10, bandwidth = 1, validation: not unreasonable.

In [136]: bit = pd.concat((kpw_9_16p.density_df.query('p_total > 0')[['p_total', 'F', 'S']],

.....: kpw_9_16cp.density_df.query('p_total > 0')[['p_total', 'F', 'S']]),

.....: keys=['exact', 'comp Po'], axis=1)

.....:

In [137]: bit.index = [f'{i:.0f}' for i in bit.index]

In [138]: bit.index.name = 'loss'

In [139]: with pd.option_context('display.max_rows', 360, 'display.max_columns', 10,

.....: 'display.width', 150, 'display.float_format', lambda x: f'{x:.7g}'):

.....: print(bit)

.....:

exact comp Po

p_total F S p_total F S

loss

0 0.952739 0.952739 0.04726095 0.9530099 0.9530099 0.04699011

14 0.0004766078 0.9532157 0.04678434 0.0004765049 0.9534864 0.04651361

15 0.0014217 0.9546374 0.04536264 0.001419985 0.9549064 0.04509362

16 0.001354813 0.9559922 0.04400783 0.001353274 0.9562597 0.04374035

17 0.0004766078 0.9564688 0.04353122 0.0004765049 0.9567362 0.04326384

18 0.003375083 0.9598439 0.04015614 0.003364125 0.9601003 0.03989972

19 0.0005147571 0.9603586 0.03964138 0.0005146252 0.9606149 0.03938509

20 0.001221069 0.9615797 0.03842031 0.001219853 0.9618348 0.03816524

24 0.004633684 0.9662134 0.03378663 0.004612568 0.9664473 0.03355267

26 0.00376864 0.969982 0.03001799 0.003754859 0.9702022 0.02979781

28 0.001163761 0.9711458 0.02885423 0.001162791 0.971365 0.02863502

29 7.112054e-07 0.9711465 0.02885352 7.099922e-07 0.9713657 0.02863431

30 0.0009830108 0.9721295 0.02787051 0.0009833345 0.972349 0.02765098

31 0.001175572 0.9733051 0.02669493 0.001174457 0.9735235 0.02647652

32 2.399591e-06 0.9733075 0.02669253 3.352879e-06 0.9735268 0.02647317

33 5.971631e-06 0.9733134 0.02668656 5.946495e-06 0.9735328 0.02646722

34 6.178405e-06 0.9733196 0.02668038 6.272902e-06 0.9735391 0.02646095

35 4.242488e-06 0.9733239 0.02667614 4.23041e-06 0.9735433 0.02645672

36 1.993891e-06 0.9733259 0.02667415 7.927184e-06 0.9735512 0.02644879

37 2.434369e-06 0.9733283 0.02667171 2.426553e-06 0.9735536 0.02644637

38 6.643644e-06 0.9733349 0.02666507 6.751312e-06 0.9735604 0.02643961

39 7.574225e-06 0.9733425 0.02665749 7.531446e-06 0.9735679 0.02643208

40 8.474451e-06 0.973351 0.02664902 9.207982e-06 0.9735771 0.02642287

41 7.941654e-06 0.9733589 0.02664108 7.901023e-06 0.973585 0.02641497

42 2.23561e-05 0.9733813 0.02661872 2.219562e-05 0.9736072 0.02639278

43 6.125396e-06 0.9733874 0.0266126 6.100774e-06 0.9736133 0.02638668

44 2.143545e-05 0.9734088 0.02659116 2.130123e-05 0.9736346 0.02636538

45 4.672158e-06 0.9734135 0.02658649 4.659237e-06 0.9736393 0.02636072

46 1.210077e-05 0.9734256 0.02657439 1.205366e-05 0.9736513 0.02634866

47 2.791514e-06 0.9734284 0.0265716 2.78804e-06 0.9736541 0.02634587

48 5.56219e-06 0.973434 0.02656603 1.670997e-05 0.9736708 0.02632916

49 4.696495e-06 0.9734387 0.02656134 4.6784e-06 0.9736755 0.02632449

50 2.022647e-05 0.9734589 0.02654111 2.007543e-05 0.9736956 0.02630441

51 1.510358e-06 0.9734604 0.0265396 1.516371e-06 0.9736971 0.02630289

52 5.666162e-06 0.9734661 0.02653394 1.304127e-05 0.9737101 0.02628985

53 1.370555e-08 0.9734661 0.02653392 1.686769e-08 0.9737102 0.02628984

54 9.392317e-06 0.9734755 0.02652453 9.356468e-06 0.9737195 0.02628048

55 0.004591308 0.9780668 0.02193322 0.004570612 0.9782901 0.02170987

56 3.900383e-06 0.9780707 0.02192932 4.60947e-06 0.9782947 0.02170526

57 4.682325e-06 0.9780754 0.02192464 4.659748e-06 0.9782994 0.0217006

58 1.240279e-06 0.9780766 0.0219234 1.246296e-06 0.9783006 0.02169935

59 1.480938e-06 0.9780781 0.02192192 1.478042e-06 0.9783021 0.02169787

60 0.02125253 0.9993306 0.000669383 0.02079525 0.9990974 0.0009026226

61 1.248838e-06 0.9993319 0.0006681341 1.247493e-06 0.9990986 0.0009013751

62 4.172979e-08 0.9993319 0.0006680924 7.93117e-07 0.9990994 0.000900582

63 2.713599e-08 0.9993319 0.0006680653 4.479884e-08 0.9990995 0.0009005372

64 4.244129e-08 0.999332 0.0006680228 6.96877e-08 0.9990995 0.0009004675

65 4.491981e-08 0.999332 0.0006679779 5.030504e-08 0.9990996 0.0009004172

66 4.146533e-08 0.9993321 0.0006679364 9.361181e-08 0.9990997 0.0009003236

67 2.339189e-08 0.9993321 0.000667913 4.760197e-08 0.9990997 0.000900276

68 8.513895e-08 0.9993322 0.0006678279 1.101497e-07 0.9990998 0.0009001659

69 2.329551e-06 0.9993345 0.0006654983 2.321713e-06 0.9991022 0.0008978441

70 6.910878e-06 0.9993414 0.0006585875 6.89662e-06 0.9991091 0.0008909475

71 6.544798e-06 0.999348 0.0006520427 6.512085e-06 0.9991156 0.0008844354

72 2.350356e-06 0.9993503 0.0006496923 2.366974e-06 0.9991179 0.0008820685

73 1.628085e-05 0.9993666 0.0006334115 1.615066e-05 0.9991341 0.0008659178

74 1.314419e-05 0.9993797 0.0006202673 1.294404e-05 0.999147 0.0008529738

75 3.761971e-05 0.9994174 0.0005826475 3.685732e-05 0.9991839 0.0008161165

76 3.023577e-05 0.9994476 0.0005524118 2.959418e-05 0.9992135 0.0007865223

77 1.064505e-05 0.9994582 0.0005417667 1.041214e-05 0.9992239 0.0007761101

78 7.531246e-05 0.9995335 0.0004664543 7.34545e-05 0.9992973 0.0007026556

79 3.379094e-05 0.9995673 0.0004326633 3.334395e-05 0.9993307 0.0006693117

80 2.725768e-05 0.9995946 0.0004054057 2.665243e-05 0.9993573 0.0006426592

81 1.816289e-05 0.9996128 0.0003872428 1.801028e-05 0.9993754 0.000624649

82 5.911614e-09 0.9996128 0.0003872369 1.74019e-08 0.9993754 0.0006246316

83 5.608384e-06 0.9996184 0.0003816285 5.586048e-06 0.999381 0.0006190455

84 0.0001033707 0.9997217 0.0002782578 0.0001006574 0.9994816 0.0005183881

85 4.743e-06 0.9997265 0.0002735148 4.72191e-06 0.9994863 0.0005136662

86 8.972427e-05 0.9998162 0.0001837905 8.756326e-05 0.9995739 0.0004261029

87 1.649612e-08 0.9998162 0.000183774 2.194197e-08 0.9995739 0.000426081

88 2.598867e-05 0.9998422 0.0001577853 2.540443e-05 0.9995993 0.0004006766

89 4.722525e-08 0.9998423 0.0001577381 4.726622e-08 0.9995994 0.0004006293

90 2.194831e-05 0.9998642 0.0001357898 2.147808e-05 0.9996208 0.0003791512

91 2.623287e-05 0.9998904 0.0001095569 2.56655e-05 0.9996465 0.0003534857

92 6.536066e-08 0.9998905 0.0001094916 8.594597e-08 0.9996466 0.0003533998

93 1.65287e-07 0.9998907 0.0001093263 1.62614e-07 0.9996468 0.0003532372

94 1.743665e-07 0.9998908 0.0001091519 1.733535e-07 0.9996469 0.0003530638

95 1.355125e-07 0.999891 0.0001090164 1.365987e-07 0.9996471 0.0003529272

96 8.286137e-08 0.9998911 0.0001089335 2.111788e-07 0.9996473 0.000352716

97 1.619798e-07 0.9998912 0.0001087716 1.594421e-07 0.9996474 0.0003525566

98 1.778121e-07 0.9998914 0.0001085938 1.768561e-07 0.9996476 0.0003523797

99 2.722478e-07 0.9998917 0.0001083215 2.665397e-07 0.9996479 0.0003521132

100 2.116102e-07 0.9998919 0.0001081099 2.234979e-07 0.9996481 0.0003518897

101 2.354722e-07 0.9998921 0.0001078744 2.302657e-07 0.9996483 0.0003516594

102 5.121685e-07 0.9998926 0.0001073623 4.978643e-07 0.9996488 0.0003511616

103 1.63469e-07 0.9998928 0.0001071988 2.132647e-07 0.9996491 0.0003509483

104 5.007765e-07 0.9998933 0.000106698 4.873585e-07 0.9996495 0.0003504609

105 2.016058e-07 0.9998935 0.0001064964 1.979245e-07 0.9996497 0.000350263

106 2.772016e-07 0.9998938 0.0001062192 2.703786e-07 0.99965 0.0003499926

107 8.955276e-08 0.9998939 0.0001061296 1.233815e-07 0.9996501 0.0003498692

108 1.241644e-07 0.999894 0.0001060055 3.6475e-07 0.9996505 0.0003495045

109 1.499989e-07 0.9998941 0.0001058555 1.469601e-07 0.9996506 0.0003493575

110 4.787335e-07 0.9998946 0.0001053768 1.139834e-05 0.999662 0.0003379592

111 5.24875e-08 0.9998947 0.0001053243 5.520826e-08 0.9996621 0.000337904

112 1.489302e-07 0.9998948 0.0001051753 3.069069e-07 0.9996624 0.0003375971

113 6.282775e-09 0.9998948 0.0001051691 6.359186e-09 0.9996624 0.0003375907

114 2.166401e-07 0.999895 0.0001049524 2.112529e-07 0.9996626 0.0003373795

115 0.0001024173 0.9999975 2.53513e-06 9.973353e-05 0.9997624 0.0002376459

116 9.301591e-08 0.9999976 2.442114e-06 1.065637e-07 0.9997625 0.0002375394

117 1.046485e-07 0.9999977 2.337466e-06 1.054805e-07 0.9997626 0.0002374339

118 2.779748e-08 0.9999977 2.309668e-06 2.74138e-08 0.9997626 0.0002374065

119 3.323942e-08 0.9999977 2.276429e-06 3.258744e-08 0.9997626 0.0002373739

120 1.07834e-09 0.9999977 2.27535e-06 0.0002268827 0.9999895 1.049118e-05

121 2.805718e-08 0.9999978 2.247293e-06 2.767002e-08 0.9999895 1.046351e-05

122 1.04354e-09 0.9999978 2.24625e-06 1.753529e-08 0.9999896 1.044597e-05

123 1.015218e-09 0.9999978 2.245234e-06 1.506102e-09 0.9999896 1.044447e-05

124 1.11823e-09 0.9999978 2.244116e-06 7.176094e-09 0.9999896 1.043729e-05

125 1.330164e-09 0.9999978 2.242786e-06 1.78429e-08 0.9999896 1.041945e-05

126 1.040647e-09 0.9999978 2.241745e-06 1.771138e-08 0.9999896 1.040174e-05

127 7.934845e-10 0.9999978 2.240952e-06 6.910456e-09 0.9999896 1.039483e-05

128 2.074415e-09 0.9999978 2.238878e-06 4.117227e-08 0.9999896 1.035365e-05

129 5.213364e-08 0.9999978 2.186744e-06 5.695507e-08 0.9999897 1.02967e-05

130 1.542995e-07 0.999998 2.032444e-06 1.646233e-07 0.9999899 1.013208e-05

131 1.46062e-07 0.9999981 1.886382e-06 1.424089e-07 0.99999 9.989666e-06

132 5.249366e-08 0.9999982 1.833889e-06 5.171857e-08 0.9999901 9.937948e-06

133 3.632949e-07 0.9999985 1.470594e-06 3.526438e-07 0.9999904 9.585304e-06

134 5.60785e-08 0.9999986 1.414515e-06 2.220186e-07 0.9999906 9.363285e-06

135 1.318434e-07 0.9999987 1.282672e-06 4.663595e-07 0.9999911 8.896926e-06

136 4.358886e-10 0.9999987 1.282236e-06 3.667832e-07 0.9999915 8.530142e-06

137 3.292504e-10 0.9999987 1.281907e-06 1.138415e-07 0.9999916 8.416301e-06

138 6.005527e-10 0.9999987 1.281306e-06 8.153441e-07 0.9999924 7.600957e-06

139 4.976509e-07 0.9999992 7.836552e-07 6.051008e-07 0.999993 6.995856e-06

140 4.940901e-10 0.9999992 7.831612e-07 3.024997e-07 0.9999933 6.693356e-06

141 4.051553e-07 0.9999996 3.780058e-07 4.064893e-07 0.9999937 6.286867e-06

142 1.556782e-10 0.9999996 3.778501e-07 4.463796e-10 0.9999937 6.286421e-06

143 1.251058e-07 0.9999997 2.527444e-07 1.219742e-07 0.9999938 6.164447e-06

144 1.937367e-10 0.9999997 2.525506e-07 1.098375e-06 0.9999949 5.066072e-06

145 1.058015e-07 0.9999999 1.467492e-07 1.030876e-07 0.999995 4.962984e-06

146 1.262168e-07 1 2.053237e-08 1.016858e-06 0.9999961 3.946126e-06

147 3.685373e-10 1 2.016383e-08 5.121882e-10 0.9999961 3.945614e-06

148 6.46479e-10 1 1.951735e-08 2.77595e-07 0.9999963 3.668019e-06

149 6.999917e-10 1 1.881736e-08 9.506666e-10 0.9999963 3.667068e-06

150 4.588675e-10 1 1.835849e-08 2.346692e-07 0.9999966 3.432399e-06

151 2.170583e-10 1 1.814144e-08 2.805268e-07 0.9999968 3.151872e-06

152 2.643346e-10 1 1.78771e-08 1.33265e-09 0.9999968 3.15054e-06

153 7.16224e-10 1 1.716088e-08 2.204159e-09 0.9999969 3.148335e-06

154 8.158174e-10 1 1.634506e-08 2.534458e-09 0.9999969 3.145801e-06

155 9.122321e-10 1 1.543283e-08 2.028215e-09 0.9999969 3.143773e-06

156 8.566022e-10 1 1.457623e-08 2.859701e-09 0.9999969 3.140913e-06

157 2.40212e-09 1 1.217411e-08 2.93432e-09 0.9999969 3.137979e-06

158 6.608837e-10 1 1.151322e-08 2.44401e-09 0.9999969 3.135535e-06

159 2.304181e-09 1 9.209041e-09 4.077408e-09 0.9999969 3.131457e-06

160 5.036921e-10 1 8.705349e-09 2.915487e-09 0.9999969 3.128542e-06

161 1.300943e-09 1 7.404406e-09 3.161405e-09 0.9999969 3.12538e-06

162 3.006818e-10 1 7.103724e-09 5.729582e-09 0.9999969 3.119651e-06

163 5.986384e-10 1 6.505086e-09 3.201579e-09 0.9999969 3.116449e-06

164 5.047601e-10 1 6.000326e-09 5.670897e-09 0.9999969 3.110778e-06

165 2.172347e-09 1 3.827979e-09 2.073139e-08 0.9999969 3.090047e-06

166 1.623502e-10 1 3.665628e-09 3.083291e-09 0.9999969 3.086964e-06

167 6.086006e-10 1 3.057028e-09 2.082057e-09 0.9999969 3.084882e-06

168 2.04573e-12 1 3.054982e-09 3.995334e-09 0.9999969 3.080886e-06

169 1.009057e-09 1 2.045925e-09 2.109975e-09 0.9999969 3.078776e-06

170 6.145147e-10 1 1.431411e-09 2.439393e-07 0.9999972 2.834837e-06

171 4.192868e-10 1 1.012124e-09 8.580199e-10 0.9999972 2.833979e-06

172 5.027193e-10 1 5.094045e-10 3.601279e-09 0.9999972 2.830378e-06

173 1.333299e-10 1 3.760746e-10 1.352801e-10 0.9999972 2.830242e-06

174 1.590085e-10 1 2.170661e-10 2.382985e-09 0.9999972 2.827859e-06

175 4.288268e-12 1 2.127779e-10 1.088124e-06 0.9999983 1.739736e-06

176 1.340885e-10 1 7.868939e-11 1.228987e-09 0.9999983 1.738507e-06

177 4.486189e-12 1 7.42032e-11 1.192855e-09 0.9999983 1.737314e-06

178 2.920835e-12 1 7.128231e-11 3.02749e-10 0.9999983 1.737011e-06

179 4.562823e-12 1 6.671952e-11 3.683841e-10 0.9999983 1.736643e-06

180 4.82662e-12 1 6.189294e-11 1.65027e-06 0.9999999 8.637285e-08

181 4.454919e-12 1 5.743805e-11 3.319206e-10 0.9999999 8.604093e-08

182 2.514367e-12 1 5.492373e-11 2.035136e-10 0.9999999 8.583741e-08

183 9.143925e-12 1 4.577982e-11 8.424069e-11 0.9999999 8.575317e-08

184 3.826298e-12 1 4.195355e-11 1.503577e-10 0.9999999 8.560282e-08

185 7.320083e-12 1 3.463352e-11 4.000487e-10 0.9999999 8.520277e-08

186 2.580997e-12 1 3.205247e-11 3.64933e-10 0.9999999 8.483783e-08

187 6.060502e-12 1 2.599199e-11 1.396254e-10 0.9999999 8.469821e-08

188 3.909234e-12 1 2.208278e-11 8.727237e-10 0.9999999 8.382548e-08

189 3.768936e-12 1 1.831379e-11 7.747876e-10 0.9999999 8.30507e-08

190 3.132506e-12 1 1.51813e-11 1.950703e-09 0.9999999 8.109999e-08

191 1.538332e-12 1 1.364298e-11 1.62618e-09 0.9999999 7.947381e-08

192 1.447886e-12 1 1.219513e-11 5.652266e-10 0.9999999 7.890859e-08

193 2.725839e-12 1 9.469314e-12 3.871408e-09 0.9999999 7.503718e-08

194 6.673824e-13 1 8.801959e-12 2.58819e-09 0.9999999 7.244899e-08

195 2.106876e-12 1 6.695089e-12 3.878648e-09 0.9999999 6.857034e-08

196 2.600251e-12 1 4.094836e-12 3.322862e-09 0.9999999 6.524748e-08

197 6.347047e-13 1 3.460121e-12 8.305254e-10 0.9999999 6.441695e-08

198 7.662416e-13 1 2.693845e-12 6.129516e-09 0.9999999 5.828744e-08

199 5.279873e-13 1 2.165823e-12 6.156754e-09 0.9999999 5.213068e-08

200 1.257773e-12 1 9.080514e-13 2.36799e-09 1 4.976269e-08

201 1.318127e-14 1 8.948398e-13 4.582293e-09 1 4.51804e-08

202 5.310998e-13 1 3.637091e-13 5.655193e-12 1 4.517475e-08

203 2.332875e-14 1 3.403944e-13 1.331814e-09 1 4.384293e-08

204 1.743248e-13 1 1.660894e-13 7.991045e-09 1 3.585189e-08

205 1.421973e-14 1 1.518785e-13 1.125462e-09 1 3.472643e-08

206 1.067366e-14 1 1.412204e-13 7.84441e-09 1 2.688202e-08

207 1.25541e-14 1 1.286748e-13 6.361132e-12 1 2.687566e-08

208 1.108523e-14 1 1.175726e-13 2.022885e-09 1 2.485277e-08

209 9.803926e-15 1 1.078027e-13 1.1113e-11 1 2.484166e-08

210 9.503263e-15 1 9.825474e-14 1.710189e-09 1 2.313147e-08

211 1.723964e-14 1 8.104628e-14 2.045013e-09 1 2.108646e-08

212 8.14414e-15 1 7.294165e-14 1.447721e-11 1 2.107198e-08

213 1.419199e-14 1 5.87308e-14 1.99869e-11 1 2.105199e-08

214 1.306909e-14 1 4.563017e-14 2.498278e-11 1 2.102701e-08

215 9.182056e-15 1 3.641532e-14 1.943114e-11 1 2.100758e-08

216 8.3874e-15 1 2.797762e-14 2.588086e-11 1 2.09817e-08

217 4.424326e-15 1 2.353673e-14 3.051195e-11 1 2.095118e-08

218 6.462422e-15 1 1.709743e-14 2.291723e-11 1 2.092827e-08

219 1.852404e-15 1 1.521006e-14 3.87301e-11 1 2.088954e-08

220 3.656445e-15 1 1.154632e-14 4.736282e-11 1 2.084217e-08

221 3.85918e-16 1 1.121325e-14 2.793092e-11 1 2.081424e-08

222 1.257844e-15 1 9.992007e-15 4.501632e-11 1 2.076923e-08

223 2.590752e-15 1 7.438494e-15 2.96758e-11 1 2.073955e-08

224 3.203268e-15 1 4.218847e-15 4.462978e-11 1 2.069492e-08

226 2.513132e-15 1 1.665335e-15 2.380553e-11 1 2.02578e-08

228 8.000274e-16 1 8.881784e-16 2.928074e-11 1 2.020762e-08

230 6.667216e-16 1 2.220446e-16 2.644072e-09 1 1.754439e-08

225 NaN NaN NaN 4.133196e-10 1 2.02816e-08

227 NaN NaN NaN 2.090073e-11 1 2.02369e-08

229 NaN NaN NaN 1.915667e-11 1 2.018846e-08

231 NaN NaN NaN 8.206594e-12 1 1.753618e-08

232 NaN NaN NaN 2.810019e-11 1 1.750808e-08

233 NaN NaN NaN 1.469202e-12 1 1.750661e-08

234 NaN NaN NaN 1.791823e-11 1 1.748869e-08

235 NaN NaN NaN 7.914547e-09 1 9.574146e-09

236 NaN NaN NaN 9.459713e-12 1 9.564686e-09

237 NaN NaN NaN 8.997999e-12 1 9.555688e-09

238 NaN NaN NaN 2.312338e-12 1 9.553376e-09

239 NaN NaN NaN 2.852462e-12 1 9.550524e-09

240 NaN NaN NaN 9.002972e-09 1 5.475517e-10

241 NaN NaN NaN 2.816684e-12 1 5.44735e-10

242 NaN NaN NaN 1.639808e-12 1 5.430952e-10

243 NaN NaN NaN 1.558068e-12 1 5.415371e-10

244 NaN NaN NaN 1.794712e-12 1 5.397425e-10

245 NaN NaN NaN 4.569197e-12 1 5.351732e-10

246 NaN NaN NaN 3.991432e-12 1 5.311818e-10

247 NaN NaN NaN 1.48429e-12 1 5.296975e-10

248 NaN NaN NaN 9.45804e-12 1 5.202395e-10

249 NaN NaN NaN 7.367474e-12 1 5.128721e-10

250 NaN NaN NaN 1.533775e-11 1 4.975343e-10

251 NaN NaN NaN 1.288323e-11 1 4.846511e-10

252 NaN NaN NaN 4.119826e-12 1 4.805313e-10

253 NaN NaN NaN 2.848955e-11 1 4.520417e-10

254 NaN NaN NaN 2.153303e-11 1 4.305087e-10

255 NaN NaN NaN 2.401756e-11 1 4.064912e-10

256 NaN NaN NaN 2.364939e-11 1 3.828418e-10

257 NaN NaN NaN 4.549044e-12 1 3.782927e-10

258 NaN NaN NaN 3.505759e-11 1 3.432351e-10

259 NaN NaN NaN 4.316564e-11 1 3.000695e-10

260 NaN NaN NaN 1.428383e-11 1 2.857857e-10

261 NaN NaN NaN 3.440264e-11 1 2.513831e-10

262 NaN NaN NaN 4.775503e-14 1 2.513354e-10

263 NaN NaN NaN 9.695625e-12 1 2.416398e-10

264 NaN NaN NaN 4.360835e-11 1 1.980315e-10

265 NaN NaN NaN 8.192855e-12 1 1.898386e-10

266 NaN NaN NaN 4.524329e-11 1 1.445953e-10

267 NaN NaN NaN 5.492698e-14 1 1.445404e-10

268 NaN NaN NaN 1.10606e-11 1 1.334798e-10

269 NaN NaN NaN 9.141233e-14 1 1.333884e-10

270 NaN NaN NaN 9.353046e-12 1 1.240353e-10

271 NaN NaN NaN 1.118703e-11 1 1.128483e-10

272 NaN NaN NaN 1.160805e-13 1 1.127322e-10

273 NaN NaN NaN 1.367965e-13 1 1.125954e-10

274 NaN NaN NaN 1.828934e-13 1 1.124125e-10

275 NaN NaN NaN 1.578676e-13 1 1.122547e-10

276 NaN NaN NaN 1.74829e-13 1 1.120798e-10

277 NaN NaN NaN 2.204896e-13 1 1.118593e-10

278 NaN NaN NaN 1.607224e-13 1 1.116985e-10

279 NaN NaN NaN 2.648382e-13 1 1.114338e-10

280 NaN NaN NaN 6.39425e-13 1 1.107944e-10

281 NaN NaN NaN 1.809595e-13 1 1.106134e-10

282 NaN NaN NaN 2.707045e-13 1 1.103427e-10

283 NaN NaN NaN 1.970095e-13 1 1.101457e-10

284 NaN NaN NaN 2.664828e-13 1 1.098792e-10

285 NaN NaN NaN 4.382094e-12 1 1.054972e-10

286 NaN NaN NaN 1.397449e-13 1 1.053574e-10

287 NaN NaN NaN 1.477025e-13 1 1.052097e-10

288 NaN NaN NaN 1.615116e-13 1 1.050482e-10

289 NaN NaN NaN 1.259848e-13 1 1.049222e-10

290 NaN NaN NaN 1.916858e-11 1 8.575363e-11

291 NaN NaN NaN 5.610997e-14 1 8.569756e-11

292 NaN NaN NaN 1.640735e-13 1 8.553347e-11

293 NaN NaN NaN 1.077555e-14 1 8.55227e-11

294 NaN NaN NaN 1.011079e-13 1 8.542156e-11

295 NaN NaN NaN 4.317568e-11 1 4.224587e-11

296 NaN NaN NaN 5.481826e-14 1 4.219103e-11

297 NaN NaN NaN 5.099189e-14 1 4.214007e-11

298 NaN NaN NaN 1.407973e-14 1 4.212597e-11

299 NaN NaN NaN 1.710537e-14 1 4.210887e-11

300 NaN NaN NaN 3.929458e-11 1 2.814304e-12

301 NaN NaN NaN 1.865038e-14 1 2.795653e-12

302 NaN NaN NaN 1.020398e-14 1 2.785439e-12

303 NaN NaN NaN 1.61517e-14 1 2.76934e-12

304 NaN NaN NaN 1.513325e-14 1 2.754241e-12

305 NaN NaN NaN 3.490552e-14 1 2.71938e-12

306 NaN NaN NaN 3.002566e-14 1 2.689404e-12

307 NaN NaN NaN 1.066545e-14 1 2.678746e-12

308 NaN NaN NaN 6.886354e-14 1 2.609912e-12

309 NaN NaN NaN 5.300219e-14 1 2.556955e-12

310 NaN NaN NaN 9.01918e-14 1 2.466805e-12

311 NaN NaN NaN 7.905782e-14 1 2.387757e-12

312 NaN NaN NaN 2.253344e-14 1 2.365219e-12

313 NaN NaN NaN 1.580737e-13 1 2.207123e-12

314 NaN NaN NaN 1.355182e-13 1 2.071565e-12

315 NaN NaN NaN 1.186181e-13 1 1.952993e-12

316 NaN NaN NaN 1.363317e-13 1 1.816658e-12

317 NaN NaN NaN 1.995775e-14 1 1.796674e-12

318 NaN NaN NaN 1.624001e-13 1 1.634248e-12

319 NaN NaN NaN 2.30203e-13 1 1.404099e-12

320 NaN NaN NaN 7.025782e-14 1 1.333822e-12

321 NaN NaN NaN 1.935323e-13 1 1.14031e-12

322 NaN NaN NaN 3.044294e-16 1 1.139977e-12

323 NaN NaN NaN 5.294786e-14 1 1.087019e-12

324 NaN NaN NaN 1.904147e-13 1 8.966161e-13

325 NaN NaN NaN 4.47376e-14 1 8.518741e-13

326 NaN NaN NaN 2.081715e-13 1 6.437073e-13

327 NaN NaN NaN 3.651783e-16 1 6.433742e-13

328 NaN NaN NaN 4.841219e-14 1 5.949685e-13

329 NaN NaN NaN 5.792017e-16 1 5.944134e-13

330 NaN NaN NaN 4.096891e-14 1 5.534462e-13

331 NaN NaN NaN 4.899058e-14 1 5.044853e-13

332 NaN NaN NaN 7.188962e-16 1 5.038192e-13

333 NaN NaN NaN 7.541253e-16 1 5.030421e-13

334 NaN NaN NaN 1.051268e-15 1 5.020429e-13

335 NaN NaN NaN 1.215004e-15 1 5.008216e-13

336 NaN NaN NaN 9.354349e-16 1 4.999334e-13

337 NaN NaN NaN 1.222217e-15 1 4.987122e-13

338 NaN NaN NaN 8.942888e-16 1 4.97824e-13

339 NaN NaN NaN 1.412135e-15 1 4.963807e-13

340 NaN NaN NaN 5.994606e-15 1 4.903855e-13

341 NaN NaN NaN 9.247895e-16 1 4.894973e-13

342 NaN NaN NaN 1.322465e-15 1 4.881651e-13

343 NaN NaN NaN 1.014759e-15 1 4.871659e-13

344 NaN NaN NaN 1.290385e-15 1 4.858336e-13

345 NaN NaN NaN 3.144116e-14 1 4.544143e-13

346 NaN NaN NaN 6.647595e-16 1 4.537482e-13

347 NaN NaN NaN 8.041342e-16 1 4.52971e-13

348 NaN NaN NaN 7.163302e-16 1 4.523049e-13

349 NaN NaN NaN 6.480017e-16 1 4.516387e-13

350 NaN NaN NaN 1.043598e-13 1 3.472778e-13

351 NaN NaN NaN 2.970056e-16 1 3.469447e-13

352 NaN NaN NaN 7.695338e-16 1 3.461675e-13

354 NaN NaN NaN 4.549113e-16 1 3.457234e-13

355 NaN NaN NaN 1.88428e-13 1 1.573186e-13

356 NaN NaN NaN 2.541842e-16 1 1.570966e-13

357 NaN NaN NaN 2.321641e-16 1 1.568745e-13

360 NaN NaN NaN 1.4293e-13 1 1.398881e-14

368 NaN NaN NaN 3.653724e-16 1 1.365574e-14

369 NaN NaN NaN 3.012033e-16 1 1.332268e-14

370 NaN NaN NaN 4.262703e-16 1 1.287859e-14

371 NaN NaN NaN 3.993759e-16 1 1.24345e-14

373 NaN NaN NaN 7.04541e-16 1 1.176836e-14

374 NaN NaN NaN 6.775864e-16 1 1.110223e-14

375 NaN NaN NaN 4.868756e-16 1 1.065814e-14

376 NaN NaN NaN 6.44266e-16 1 9.992007e-15

378 NaN NaN NaN 6.361091e-16 1 9.325873e-15

379 NaN NaN NaN 9.883173e-16 1 8.326673e-15

380 NaN NaN NaN 2.902703e-16 1 7.993606e-15

381 NaN NaN NaN 8.696954e-16 1 7.105427e-15

383 NaN NaN NaN 2.30469e-16 1 6.883383e-15

384 NaN NaN NaN 7.177201e-16 1 6.217249e-15

386 NaN NaN NaN 7.941167e-16 1 5.440093e-15

410 NaN NaN NaN 4.545908e-16 1 4.996004e-15

415 NaN NaN NaN 6.831854e-16 1 4.32987e-15

420 NaN NaN NaN 4.481143e-16 1 3.885781e-15

In [140]: fig, axs = plt.subplots(1,2, figsize=(3.5*2, 2.45), constrained_layout=True, squeeze=True)

In [141]: ax0, ax1 = axs.flat

In [142]: bit[('exact', 'p_total')].plot(marker='.', lw=.25, logy=True, ax=ax0, label='Portfolio');

In [143]: bit[('comp Po', 'p_total')].plot(marker='.', markerfacecolor='None', lw=.25, logy=True, ax=ax0, label='compound Po');

In [144]: (1-bit[('exact', 'p_total')].cumsum()).plot(ax=ax1);

In [145]: (1-bit[('comp Po', 'p_total')].cumsum()).plot(ax=ax1);

In [146]: ax0.legend();

In [147]: ax0.set(ylabel='log pmf');

In [148]: ax1.set(ylabel='survival function');

Exercise 9.73.

An insurance company sold one-year term life insurance on a group of 2,300 independent lives as given in the next table.

The insurance company reinsures amounts in excess of 100,000 on each life. The reinsurer wishes to charge a premium that is sufficient to guarantee that it will lose money 5% of the time on such groups. Obtain the appropriate premium by each of the following ways:

Using a normal approximation to the aggregate claims distribution.

Using a lognormal approximation.

Using a gamma approximation.

Using the compound Poisson approximation that matches the means.

In order to make the answer self-contained, the code below includes the data munging to re-create the table, pasted from a pdf.

In [149]: data = '''1

.....: 100,000

.....: 0.10

.....: 500

.....: 2

.....: 200,000

.....: 0.02

.....: 500

.....: 3

.....: 300,000

.....: 0.02

.....: 500

.....: 4

.....: 200,000

.....: 0.10

.....: 300

.....: 5

.....: 200,000

.....: 0.10

.....: 500'''

.....:

In [150]: sdata = data.split('\n')

In [151]: df = pd.DataFrame(zip(*[iter(sdata)]*4),

.....: columns=['Class', 'Benefit', 'q', 'Number'])

.....:

In [152]: df.Benefit = df.Benefit.str.replace(',','').astype(float)

In [153]: df.q = df.q.astype(float)

In [154]: df.Number = df.Number.astype(int)

In [155]: df = df.set_index('Class')

In [156]: qd(df)

Benefit q Number

Class

1 1e+05 0.1 500

2 2e+05 0.02 500

3 3e+05 0.02 500

4 2e+05 0.1 300

5 2e+05 0.1 500

Next, build the exact solution for the gross book as a Portfolio (extra credit).

In [157]: a = [build(f'agg Class.{i} {r.q * r.Number} claims '

.....: f'dsev [{r.Benefit / 100000}] '

.....: f'binomial {r.q}')

.....: for i, r in df.iterrows()]

.....:

In [158]: p = Portfolio('KPW.9.73p', a)

In [159]: p.update(log2=10, bs=1, remove_fuzz=True)

In [160]: qd(p)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

Class.1 Freq 50 0.13416 0.11926

Sev 1 1 0 0 0

Agg 50 50 -8.4155e-14 0.13416 0.13416 0.11926 0.11926

Class.2 Freq 10 0.31305 0.30666

Sev 2 2 0 0 0

Agg 20 20 5.7554e-13 0.31305 0.31305 0.30666 0.30666

Class.3 Freq 10 0.31305 0.30666

Sev 3 3 0 0 0

Agg 30 30 2.9909e-13 0.31305 0.31305 0.30666 0.30666

Class.4 Freq 30 0.17321 0.15396

Sev 2 2 0 0 0

Agg 60 60 -1.3123e-13 0.17321 0.17321 0.15396 0.15396

Class.5 Freq 50 0.13416 0.11926

Sev 2 2 0 0 0

Agg 100 100 -1.1879e-13 0.13416 0.13416 0.11926 0.11926

total Freq 150 0.077917 0.070413

Sev 1.7333 1.7333 0 0.33086 0.081688

Agg 260 260 9.77e-15 0.082527 0.082527 0.083622 0.083622

log2 = 10, bandwidth = 1, validation: not unreasonable.

Build the reinsurer’s loss distribution exactly, as p_ceded, a Portfolio, and the compound Poisson approximation cp_ceded, an Aggregate. The temporary variable bit is used to calculate the mixed severity distribution.

In [161]: a_ceded = [build(f'agg Class.{i}.c {r.q * r.Number} claims '

.....: f'dsev [{r.Benefit / 100000 - 1}] '

.....: f'binomial {r.q}')

.....: for i, r in df.query('Benefit > 100000').iterrows()]

.....:

In [162]: p_ceded = Portfolio('KPW.9.73pc', a_ceded)

In [163]: p_ceded.update(log2=10, bs=1, remove_fuzz=True)

In [164]: qd(p_ceded)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

Class.2.c Freq 10 0.31305 0.30666

Sev 1 1 0 0 0

Agg 10 10 1.0121e-12 0.31305 0.31305 0.30666 0.30666

Class.3.c Freq 10 0.31305 0.30666

Sev 2 2 0 0 0

Agg 20 20 5.7554e-13 0.31305 0.31305 0.30666 0.30666

Class.4.c Freq 30 0.17321 0.15396

Sev 1 1 0 0 0

Agg 30 30 -9.6367e-14 0.17321 0.17321 0.15396 0.15396

Class.5.c Freq 50 0.13416 0.11926

Sev 1 1 0 0 0

Agg 50 50 -8.4155e-14 0.13416 0.13416 0.11926 0.11926

total Freq 100 0.095708 0.087165

Sev 1.1 1.1 0 0.27273 2.6667

Agg 110 110 1.4877e-14 0.1 0.1 0.10689 0.10689

log2 = 10, bandwidth = 1, validation: not unreasonable.

In [165]: bit = df.query('Benefit > 100000')

In [166]: bit['Claims'] = bit.q * bit.Number

In [167]: bit.groupby('Benefit').Claims.sum()

Out[167]:

Benefit

200000.0 90.0

300000.0 10.0

Name: Claims, dtype: float64

In [168]: cp_ceded = build('agg CP.Approx '

.....: f'{bit.Claims.sum()} claims '

.....: f'dsev [1 2] [0.9 0.1] '

.....: 'poisson')

.....:

In [169]: qd(cp_ceded)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 100 0.1 0.1

Sev 1.1 1.1 0 0.27273 0.27273 2.6667 2.6667

Agg 110 110 6.1506e-14 0.10365 0.10365 0.11469 0.11469

log2 = 14, bandwidth = 1, validation: not unreasonable.

Compute the various estimated premiums, the 95%iles of the aggregate loss distribution.

In [170]: prem_confidence = 0.95

In [171]: appx = p_ceded.approximate('all')

In [172]: ans = {k: v.ppf(prem_confidence) for k, v in appx.items()}

In [173]: ans['FFT'] = p_ceded.q(prem_confidence)

In [174]: ans['Comp Po'] = cp_ceded.q(prem_confidence)

In [175]: qd(pd.DataFrame(ans.values(),

.....: index=pd.Index(ans.keys(), name='method'),

.....: columns=['premium']).sort_values('premium'),

.....: accuracy=5)

.....:

premium

method

FFT 128

norm 128.09

slognorm 128.42

sgamma 128.42

gamma 128.7

lognorm 128.97

Comp Po 129

Exercise 9.74. A group insurance contract covers 1,000 employees. An employee can have at most one claim per year. For 500 employees, there is a 0.02 probability of a claim, and when there is a claim, the amount has an exponential distribution with mean 500. For 250 other employees, there is a 0.03 probability of a claim and amounts are exponential with mean 750. For the remaining 250 employees, the probability is 0.04 and the mean is 1,000. Determine the exact mean and variance of total claims payments. Next, construct a compound Poisson model with the same mean and determine the variance of this model.

In [176]: kpw_9_74p = build('port KPW.9.74p '

.....: 'agg A 10. claims sev 500 * expon binomial 0.02 '

.....: 'agg B 7.5 claims sev 750 * expon binomial 0.03 '

.....: 'agg C 10. claims sev 1000 * expon binomial 0.04 ')

.....:

In [177]: qd(kpw_9_74p)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

A Freq 10 0.31305 0.30666

Sev 500 500 -6.6667e-07 1 1 2 2

Agg 5000 5000 -6.6667e-07 0.44497 0.44497 0.66748 0.66748

B Freq 7.5 0.35963 0.34851

Sev 750 750 -2.963e-07 1 1 2 2

Agg 5625 5625 -2.963e-07 0.51251 0.51251 0.76882 0.76882

C Freq 10 0.30984 0.29693

Sev 1000 1000 -1.6667e-07 1 1 2 2

Agg 10000 10000 -1.6667e-07 0.44272 0.44272 0.66417 0.66417

total Freq 27.5 0.18781 0.18203

Sev 750 750 -3.2323e-07 1.0778 2.372

Agg 20625 20625 -3.2323e-07 0.27794 0.27794 0.44276 0.44276

log2 = 16, bandwidth = 2, validation: not unreasonable.

In [178]: mv(kpw_9_74p)

mean = 20625

variance = 3.286094e+07

std dev = 5732.45

Compound Poisson approximation is easy to construct as a mixture.

In [179]: kpw_9_74cp = build('agg KPW.9.74.cp [10 7.5 10] claims sev [500 750 1000] * expon poisson')

In [180]: qd(kpw_9_74cp)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 27.5 0.19069 0.19069

Sev 750 750 -3.2323e-07 1.0778 1.0778 2.372 2.372

Agg 20625 20625 -3.2323e-07 0.28036 0.28036 0.44729 0.44729

log2 = 16, bandwidth = 2, validation: not unreasonable.

In [181]: mv(kpw_9_74cp)

mean = 20625

variance = 3.34375e+07