2.13.7. Enterprise Risk Analysis

This section re-analyzes reinsurance structure alternatives introduced in Brehm et al. [2007], Enterprise Risk Analysis for Property & Liability Insurance Companies. This book is the ERM text on the syllabus for CAS Exam Part 7.

2.13.7.1. Reinsurance Example

This section analyzes the example given in Section 2.5 of Enterprise Risk Analysis.

Assumptions. ABCD writes 33M excess property and casualty business.

ABCD total gross

Loss ratio: 69.36%

Expense ratio: 23%

Combined ratio: 92.36%

Margin 2.52M

Casualty

14M premium

78% expected loss ratio

5M limits

4M xs 1M reinsurance, ceded premium 4.41M

Property

19M premium

63% expected loss ratio

20M limits

17M xs 3M per risk reinsurance, ceded premium 2.36M

95% share of 24M xs 1M cat reinsurance, ceded premium 1.53M with 1@100%

Cat program designed to cover to 250-year event.

Reinsurance total

Average recoveries 5.08M

Ceded premium 8.3M

Net premium 24.7M

Mythical alternative program

Stop-loss, 20 xs 30, ceded premium 1.98

Additional assumptions. There are no details of the stochastic model, so we assume

Frequency and severity models per DecL below,

Split the property losses into cat and non-cat by assuming that cat premium equals 2M, non-cat premium 17M, at the same loss ratios (this is just a split of losses, the by line loss ratios are not used), and

Cat, non-cat and casualty are independent.

Free and unlimited reinstatements on the catastrophe protection. See REF for a discussion of reinstatements.

2.13.7.2. Stochastic Models and Baseline Analysis

Construct the gross and net portfolios. All amounts in millions.

2.13.7.2.1. Gross Portfolio

The 250-year cat PML is printed last, to compare with the 25M program.

In [1]: from aggregate import build, qd, mv

In [2]: import pandas as pd

In [3]: import matplotlib.pyplot as plt

In [4]: abcd = build('port ABCD '

...: 'agg Casualty 14.0 premium at 78% lr '

...: '5 xs 0 '

...: 'sev lognorm 0.1 cv 10 '

...: 'mixed gamma 0.3 '

...: 'agg PropertyNC 17.0 premium at 63% lr '

...: '25 xs 0 '

...: 'sev lognorm [0.1 1] cv [5 10] wts [.7 .3] '

...: 'mixed gamma 0.1 '

...: 'agg PropertyC 2.0 premium at 63% lr '

...: '150 xs 0 '

...: 'sev 3 * pareto 2.375 - 3 '

...: 'poisson ', bs=1/128, approximation='exact')

...:

In [5]: qd(abcd)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

Casualty Freq 125.93 0.31296 0.60054

Sev 0.086717 0.086436 -0.0032438 4.0147 4.0286 9.5592 9.5552

Agg 10.92 10.885 -0.0032438 0.47532 0.47626 0.88481 0.88565

PropertyNC Freq 34.918 0.19657 0.24744

Sev 0.30672 0.30659 -0.00041535 4.91 4.9121 11.569 11.569

Agg 10.71 10.706 -0.00041535 0.85384 0.85419 1.9358 1.9358

PropertyC Freq 0.5801 1.3129 1.3129

Sev 2.172 2.172 -9.2692e-07 2.0207 2.0207 11.511 11.511

Agg 1.26 1.26 -9.2692e-07 2.9601 2.9601 12.398 12.398

total Freq 161.42 0.24785 0.57516

Sev 0.1418 0.14155 -0.0017419 5.8043 23.386

Agg 22.89 22.85 -0.0017419 0.48741 0.48813 1.6182 1.6193

log2 = 16, bandwidth = 1/128, validation: fails sev mean, agg mean.

In [6]: mv(abcd)

mean = 22.89

variance = 124.4768

std dev = 11.1569

In [7]: print(abcd['PropertyC'].q(0.996))

22.859375

2.13.7.2.2. Net Portfolio

In [8]: abcd_net = build('port ABCD:Net '

...: 'agg Casualty 14.0 premium at 78% lr '

...: '5 xs 0 '

...: 'sev lognorm 0.1 cv 10 '

...: 'occurrence net of 4 xs 1 '

...: 'mixed gamma 0.3 '

...: 'agg PropertyNC 17.0 premium at 63% lr '

...: '25 xs 0 '

...: 'sev lognorm [0.1 1] cv [5 10] wts [.7 .3] '

...: 'occurrence net of 17 xs 3 '

...: 'mixed gamma 0.1 '

...: 'agg PropertyC 2.0 premium at 63% lr '

...: '150 xs 0 '

...: 'sev 3 * pareto 2.375 - 3 '

...: 'occurrence net of 24 xs 1 '

...: 'poisson ', bs=1/128, approximation='exact')

...:

In [9]: qd(abcd_net)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

Casualty Freq 125.93 0.31296 0.60054

Sev 0.086717 0.065564 -0.24393 4.0147 2.5318 9.5592 4.1714

Agg 10.92 8.2563 -0.24393 0.47532 0.3858 0.88481 0.65534

PropertyNC Freq 34.918 0.19657 0.24744

Sev 0.30672 0.2098 -0.31597 4.91 2.8604 11.569 6.1847

Agg 10.71 7.3259 -0.31597 0.85384 0.52244 1.9358 1.0361

PropertyC Freq 0.5801 1.3129 1.3129

Sev 2.172 0.80417 -0.62976 2.0207 2.7345 11.511 36.228

Agg 1.26 0.4665 -0.62976 2.9601 3.8228 12.398 40.649

total Freq 161.42 0.24785 0.57516

Sev 0.1418 0.099419 -0.29888 5.8043 23.386

Agg 22.89 16.049 -0.29888 0.48741 0.32957 1.6182 2.0938

log2 = 16, bandwidth = 1/128, validation: n/a, reinsurance.

In [10]: qd(abcd_net.est_sd)

5.2892

2.13.7.2.3. Ceded Portfolio

In [11]: abcd_ceded = build('port ABCD:Ceded '

....: 'agg Casualty 14.0 premium at 78% lr '

....: '5 xs 0 '

....: 'sev lognorm 0.1 cv 10 '

....: 'occurrence ceded to 4 xs 1 '

....: 'mixed gamma 0.3 '

....: 'agg PropertyNC 17.0 premium at 63% lr '

....: '25 xs 0 '

....: 'sev lognorm [0.1 1] cv [5 10] wts [.7 .3] '

....: 'occurrence ceded to 17 xs 3 '

....: 'mixed gamma 0.1 '

....: 'agg PropertyC 2.0 premium at 63% lr '

....: '150 xs 0 '

....: 'sev 3 * pareto 2.375 - 3 '

....: 'occurrence ceded to 24 xs 1 '

....: 'poisson ', bs=1/128, approximation='exact')

....:

In [12]: qd(abcd_ceded)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

Casualty Freq 125.93 0.31296 0.60054

Sev 0.086717 0.020872 -0.75931 4.0147 11.205 9.5592 14.019

Agg 10.92 2.6283 -0.75931 0.47532 1.0464 0.88481 1.3572

PropertyNC Freq 34.918 0.19657 0.24744

Sev 0.30672 0.096787 -0.68444 4.91 10.657 11.569 13.51

Agg 10.71 3.3796 -0.68444 0.85384 1.8142 1.9358 2.3095

PropertyC Freq 0.5801 1.3129 1.3129

Sev 2.172 1.3679 -0.37024 2.0207 2.254 11.511 4.2512

Agg 1.26 0.7935 -0.37024 2.9601 3.2375 12.398 5.6851

total Freq 161.42 0.24785 0.57516

Sev 0.1418 0.042134 -0.70286 5.8043 23.386

Agg 22.89 6.8014 -0.70286 0.48741 1.0577 1.6182 1.7643

log2 = 16, bandwidth = 1/128, validation: n/a, reinsurance.

In [13]: qd(abcd_ceded.est_sd)

7.1941

2.13.7.2.4. Reinsurance Summary

The bottom table shows expected losses, counts, severity, loss ratios and margins implicit in the given reinsurance structure, pricing, and the gross stochastic model. The non-cat property reinsurance has the highest ceded loss ratio and the cat program the lowest.

In [14]: re_all = pd.concat((a.reinsurance_occ_layer_df for a in abcd_net),

....: keys=abcd_net.unit_names, names=['unit', 'share', 'limit', 'attach']); \

....: re_all = re_all.drop('gup', axis=0, level=3); \

....: qd(re_all, sparsify=False)

....:

stat ex ex ex cv cv cv en severity pct

view ceded net subject ceded net subject ceded ceded ceded

unit share limit attach

Casualty 1.0 4.0 1.0 2.6283 8.2563 10.885 11.205 2.5318 4.0286 2.007 1.3096 0.24147

PropertyNC 1.0 17.0 3.0 3.3796 7.3259 10.706 10.657 2.8604 4.9121 0.65611 5.151 0.31569

PropertyC 1.0 24.0 1.0 0.7935 0.4665 1.26 2.254 2.7345 2.0207 0.29294 2.7088 0.62976

In [15]: re_summary = re_all.iloc[:, [0, 3, 6, 7]]; \

....: re_summary.columns = ['ex', 'cv', 'en', 'severity']; \

....: re_summary['premium'] = [4.41, 2.36, 1.53]; \

....: re_summary['lr'] = re_summary.ex / re_summary.premium; \

....: re_summary['margin'] = re_summary.premium - re_summary.ex; \

....: qd(re_summary)

....:

ex cv en severity premium lr margin

unit share limit attach

Casualty 1.0 4.0 1.0 2.6283 11.205 2.007 1.3096 4.41 0.59599 1.7817

PropertyNC 1.0 17.0 3.0 3.3796 10.657 0.65611 5.151 2.36 1.432 -1.0196

PropertyC 1.0 24.0 1.0 0.7935 2.254 0.29294 2.7088 1.53 0.51863 0.7365

2.13.7.2.5. Underwriting Result Distributions

Make the underwriting result distributions, including the proposed stop loss reinsurance (computed by hand).

The dataframe compare accumulates the gross, ceded, and net probability mass functions. We use these

to determine statistics and to plot.

In [16]: compare = abcd.density_df[['loss', 'p_total']]; \

....: compare.columns = ['loss', 'gross']; \

....: compare['gross_uw'] = 33 - compare.loss; \

....: compare['net_current'] = abcd_net.density_df.p_total; \

....: compare['net_current_uw'] = 33 - 4.41 - 2.36 - 1.53 - compare.loss;

....:

In [17]: from aggregate import make_ceder_netter

In [18]: compare['net_stoploss'] = abcd.density_df.p_total; \

....: c, n = make_ceder_netter([(1, 20, 30)]); \

....: compare['nsll'] = n(compare.loss); \

....: g = compare.groupby('nsll').net_stoploss.sum(); \

....: compare['net_stoploss'] = 0.0; \

....: compare.loc[g.index, 'net_stoploss'] = g; \

....: compare['net_stoploss_uw'] = 33 - 1.98 - compare.loss;

....:

2.13.7.2.6. Comparison with ERA Book Figures

Statistics summary, compare Figure 2.5.2.

In [19]: from aggregate import MomentWrangler

In [20]: from scipy.interpolate import interp1d

In [21]: ans = []; cdfs = []

In [22]: for xs, den in [(compare.gross_uw, compare.gross), (compare.net_current_uw, compare.net_current),

....: (compare.net_stoploss_uw, compare.net_stoploss)]:

....: xd = xs * den

....: ex1 = np.sum(xd)

....: xd *= xs

....: ex2 = np.sum(xd)

....: ex3 = np.sum(xd * xs)

....: mw = MomentWrangler()

....: mw.noncentral = ex1, ex2, ex3

....: ans.append(mw)

....: cdfs.append(interp1d(den.cumsum(), xs))

....:

In [23]: fig_252 = pd.concat([i.stats for i in ans], keys=['Gross', 'Current', 'StopLoss'], axis=1)

In [24]: for p in [0.01, 0.99]:

....: fig_252.loc[f'q({p})'] = [float(i(p)) for i in cdfs]

....:

In [25]: qd(fig_252)

Gross Current StopLoss

ex 10.15 8.6513 10.021

var 124.41 27.975 58.777

sd 11.154 5.2892 7.6666

cv 1.0989 0.61137 0.76502

skew -1.6193 -2.0938 -1.0088

q(0.01) 25.98 18.081 24

q(0.99) -25.76 -5.6036 -7.7399

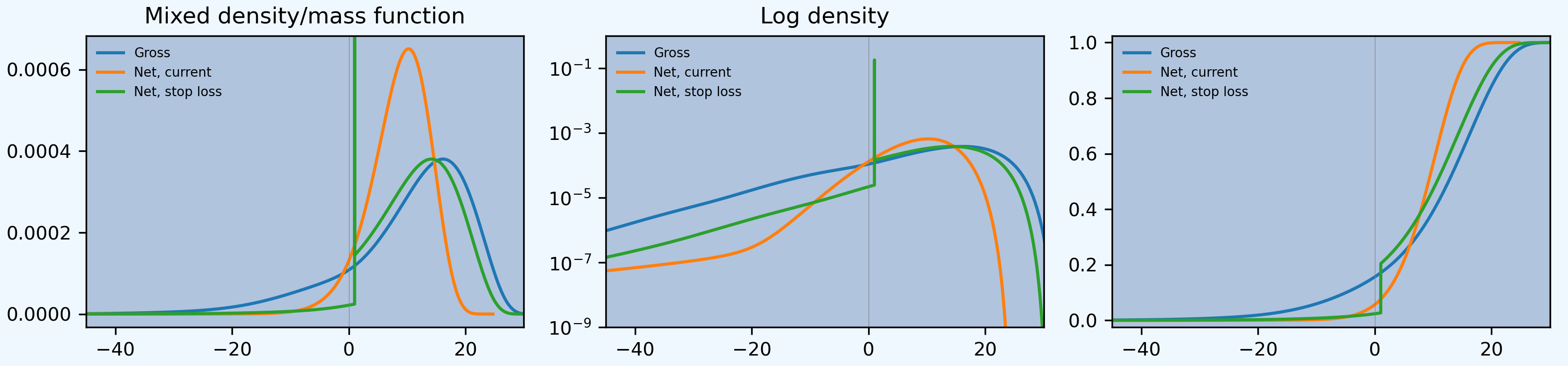

Plot of densities and distributions, compare Figure 2.5.3 and 2.5.4.

In [26]: fig, axs = plt.subplots(1, 3, figsize=(3 * 3.5, 2.45), constrained_layout=True)

In [27]: ax0, ax1, ax2 = axs.flat

In [28]: for ax in [ax0, ax1]:

....: ax.plot(compare.gross_uw, compare.gross, label='Gross')

....: ax.plot(compare.net_current_uw, compare.net_current, label='Net, current')

....: yl = ax.get_ylim()

....: ax.plot(compare.net_stoploss_uw, compare.net_stoploss, label='Net, stop loss')

....: ax.legend(loc='upper left')

....: ax.set(xlim=[-45, 30], ylim=yl)

....: ax.axvline(0, lw=.25, c='C7')

....:

In [29]: ax1.set(yscale='log', ylim=[1e-9, 1], title='Log density'); \

....: ax0.set(title='Mixed density/mass function');

....:

In [30]: ax2.plot(compare.gross_uw, 1 - compare.gross.cumsum(), label='Gross'); \

....: ax2.plot(compare.net_current_uw, 1 - compare.net_current.cumsum(), label='Net, current'); \

....: ax2.plot(compare.net_stoploss_uw, 1 - compare.net_stoploss.cumsum(), label='Net, stop loss'); \

....: ax2.legend(loc='upper left'); \

....: ax2.set(xlim=[-45, 30], ylim=[-0.025, 1.025]);

....:

In [31]: ax2.axvline(0, lw=.25, c='C7');

Numerical distribution of underwriting results at various return points, compare Figure 2.5.5. Given there was no information about the stochastic model provided, and the model here is based on common benchmarks, the agreement between the two distributions is striking.

In [32]: fig_255 = pd.DataFrame(columns=['Gross', 'Current', 'StopLoss'], dtype=float)

In [33]: for p in [.0025, .005, 0.0075, .01, .0125, .015, .0175, .02,

....: .04, .06, .08, .1, .12, .14, .16, .18, .2, .22, .24,

....: .25, .26, .28, .3, .32, .34, .36, .38, .4, .42, .44,

....: .46, .48, .5]:

....: fig_255.loc[p] = [float(i(1-p)) for i in cdfs]

....:

In [34]: fig_255.index.name = 'p'

In [35]: qd(fig_255, float_format=lambda x: f'{x:.3f}', max_rows=len(fig_255))

Gross Current StopLoss

p

0.0025 -38.503 -10.257 -20.483

0.0050 -32.113 -7.826 -14.093

0.0075 -28.394 -6.514 -10.374

0.0100 -25.760 -5.604 -7.740

0.0125 -23.740 -4.902 -5.720

0.0150 -22.114 -4.328 -4.094

0.0175 -20.758 -3.842 -2.738

0.0200 -19.595 -3.420 -1.575

0.0400 -13.603 -1.182 1.021

0.0600 -9.962 0.182 1.021

0.0800 -7.211 1.186 1.022

0.1000 -4.936 1.991 1.023

0.1200 -2.978 2.669 1.024

0.1400 -1.263 3.259 1.025

0.1600 0.246 3.784 1.026

0.1800 1.575 4.259 1.027

0.2000 2.752 4.695 1.028

0.2200 3.801 5.100 1.821

0.2400 4.745 5.478 2.765

0.2500 5.183 5.659 3.203

0.2600 5.603 5.835 3.623

0.2800 6.391 6.173 4.411

0.3000 7.121 6.496 5.141

0.3200 7.802 6.805 5.822

0.3400 8.442 7.103 6.462

0.3600 9.047 7.390 7.067

0.3800 9.622 7.669 7.642

0.4000 10.171 7.941 8.191

0.4200 10.697 8.206 8.717

0.4400 11.203 8.465 9.223

0.4600 11.692 8.720 9.712

0.4800 12.167 8.970 10.187

0.5000 12.628 9.217 10.648

2.13.7.3. Modern Analysis

The first step is to analyze the pricing in the context of needed capital. Strip expenses out (at 23% across all units) to determine a net (of expenses) technical premium.

In [36]: er = 0.23

In [37]: df = pd.DataFrame({'unit': ['Casualty', 'PropertyNC', 'PropertyC'],

....: 'prem': [14, 17, 2],

....: 'gross_loss': [a.est_m for a in abcd]}).set_index('unit')

....:

In [38]: df['ceded_prem'] = [4.41, 2.36, 1.53]; \

....: df['net_prem'] = df.prem - df.ceded_prem; \

....: df['tech_prem'] = df.prem * (1 - er); \

....: df['margin'] = df.tech_prem - df.gross_loss; \

....: df.loc['Total'] = df.sum(0); \

....: df['lr'] = df.gross_loss / df.prem; \

....: df['cr'] = df.lr + er; \

....: df['tech_lr'] = df.gross_loss / df.tech_prem;

....:

In [39]: fp = lambda x: f'{x:.1%}';

In [40]: fc = lambda x: f'{x:.2f}'

In [41]: qd(df, float_format=fc, formatters={'lr':fp, 'cr': fp, 'tech_lr': fp})

prem gross_loss ceded_prem net_prem tech_prem margin lr cr tech_lr

unit

Casualty 14.00 10.88 4.41 9.59 10.78 -0.10 77.7% 100.7% 101.0%

PropertyNC 17.00 10.71 2.36 14.64 13.09 2.38 63.0% 86.0% 81.8%

PropertyC 2.00 1.26 1.53 0.47 1.54 0.28 63.0% 86.0% 81.8%

Total 33.00 22.85 8.30 24.70 25.41 2.56 69.2% 92.2% 89.9%

The example does not specify a capital standard. Let’s investigate the implied

return on capital at different capital standards. The capital standard is

expressed as a loss percentile. The next calculation produces a table of

returns expressed as a cost of capital (coc). It also shows the expected

policyholder deficit.

In [42]: tech_prem = df.loc['Total', 'tech_prem']; \

....: ps = [.99, .995, .996, .999]; \

....: As = [abcd.q(p) for p in ps]; \

....: el = abcd.density_df.loc[As, 'exa_total']; \

....: margin = tech_prem - el; \

....: cocs = margin / (As - tech_prem); \

....: summary = pd.DataFrame({'p': ps, 'a': As, 'prem':tech_prem, 'el': el,

....: 'margin': margin, 'tech_lr': el / tech_prem, 'coc': cocs,

....: 'epd': (abcd.est_m - el) / abcd.est_m}).set_index('p')

....:

In [43]: summary.index = [fp(i) for i in summary.index]; \

....: summary.index.name = 'p'; \

....: qd(summary, float_format=fc, formatters={'coc': fp, 'tech_lr': fp, 'epd': fp})

....:

a prem el margin tech_lr coc epd

p

99.0% 58.77 25.41 22.75 2.66 89.5% 8.0% 0.5%

99.5% 65.12 25.41 22.79 2.62 89.7% 6.6% 0.3%

99.6% 67.16 25.41 22.80 2.61 89.7% 6.2% 0.2%

99.9% 80.90 25.41 22.83 2.58 89.8% 4.6% 0.1%

Based on this analysis, we assume a 99.5% (200-year) capital standard, which gives a reasonable 8% return on capital. 200-year capital is also the Solvency II standard.

From here, the analysis could proceed in many directions. The approach we select is

Calibrate a set of distortions to total pricing on a gross basis with the 200-year capital standard.

Analyze the pricing implied by these distortions on the net book and its natural allocation by unit.

Compare the model value (implied ceded premium) with market reinsurance price.

The model value is the maximum amount that is consistent with pricing according to each distortion. Reinsurance cheaper than the model value is efficient: replacing traditional capital with reinsurance capital lowers the economic cost of bearing risk.

2.13.7.3.1. Calibrate Distortions

Extract the exact cost of capital implied by given gross pricing.

In [44]: coc = summary.loc['99.5%', 'coc']

In [45]: print(coc)

0.06591531668710866

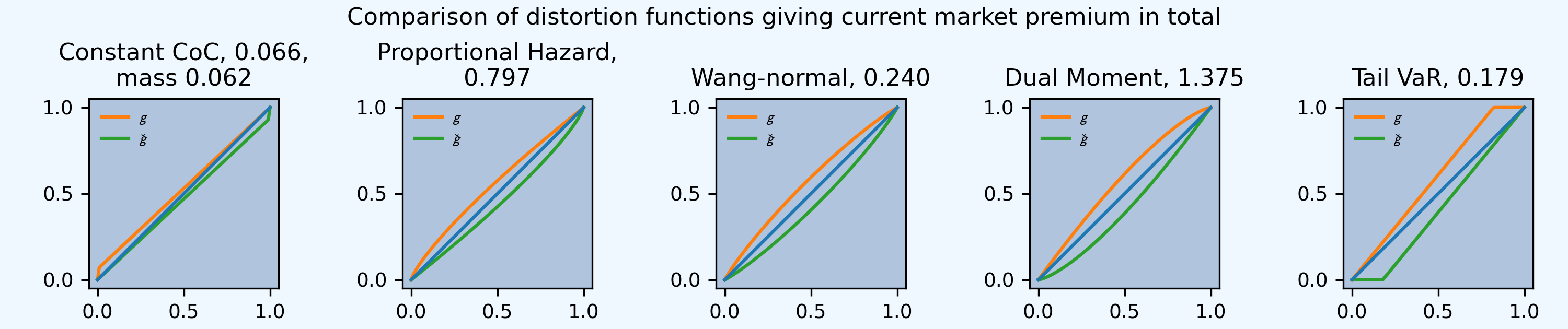

Calibrate distortions to current pricing. Use five one-parameter distortion families

constant cost of capital (CCoC),

proportional hazard (PH)

Wang,

dual, and

TVaR.

They are sorted from most tail-centric (expensive for tail risk) to cheapest. See Mildenhall and Major [2022].

The next dataframe shows the asset level and implied loss ratio,

distortion name, survival probability (0.5%), expected loss, premium, premium

to capital leverage (PQ), the cost of (return on) capital, the distortion

family parameter, and the parameterization error. The calibrated premium

matches the technical premium.

In [46]: abcd.calibrate_distortions(ROEs=[coc], Ps=[.995], strict='ordered');

In [47]: qd(abcd.distortion_df)

S L P PQ Q COC param error

a LR method

65.117188 0.896997 ccoc 0.0049978 22.793 25.41 0.63993 39.707 0.065915 0.065915 0

ph 0.0049978 22.793 25.41 0.63993 39.707 0.065915 0.7966 4.7227e-06

wang 0.0049978 22.793 25.41 0.63993 39.707 0.065915 0.24044 1.1474e-06

dual 0.0049978 22.793 25.41 0.63993 39.707 0.065915 1.3749 -7.4227e-11

tvar 0.0049978 22.793 25.41 0.63993 39.707 0.065915 0.17864 9.4873e-06

The plot show this effect: COC is fattest on the left for small exceedance probabilities (high losses), whereas TVaR is fattest on the right.

In [48]: fig, axs = plt.subplots(1, 5, figsize=(10.0, 2.1), constrained_layout=True)

In [49]: for ax, (k, v) in zip(axs.flat, abcd.dists.items()):

....: v.plot(ax=ax)

....:

In [50]: fig.suptitle('Comparison of distortion functions giving current market premium in total')

Out[50]: Text(0.5, 0.98, 'Comparison of distortion functions giving current market premium in total')

2.13.7.3.2. Analyze Implied Pricing

Apply the distortions to the net portfolio and analyze the resulting pricing

using analyze_distortions(), which includes a by-unit margin

allocation. The dataframe ans.comp_df contains a wealth of other

information; we just focus on the premium. The last row, Technical, shows

market reinsurance pricing.

In [51]: abcd_net.dists = abcd.dists

In [52]: ansn = abcd_net.analyze_distortions(p=0.996, add_comps=False); \

....: ans = abcd.analyze_distortions(p=0.996, add_comps=False); \

....: bit = pd.concat((ans.comp_df.xs('P', 0, 1), ansn.comp_df.xs('P', 0, 1),

....: ans.comp_df.xs('P', 0, 1) - ansn.comp_df.xs('P', 0, 1)),

....: axis=1, keys=['gross', 'net', 'ceded']); \

....: bit = bit.iloc[[0, 2,-1, 1, -2]]; \

....: bit.loc['Technical'] = 0.0; \

....: bit.loc['Technical', 'gross'] = df.tech_prem.sort_index().values; \

....: bit.loc['Technical', 'ceded'] = df.ceded_prem.sort_index().values; \

....: bit.loc['Technical', 'net'] = df.net_prem.sort_index().values; \

....: qd(bit, sparsify=False, line_width=50)

....:

gross gross gross gross \

line Casualty PropertyC PropertyNC total

Method

Dist ccoc 10.371 4.6237 10.55 25.545

Dist ph 11.347 1.5483 12.542 25.438

Dist wang 11.514 1.4754 12.439 25.428

Dist dual 11.698 1.4415 12.283 25.423

Dist tvar 11.908 1.4298 12.084 25.421

Technical 10.78 1.54 13.09 25.41

net net net net \

line Casualty PropertyC PropertyNC total

Method

Dist ccoc 7.8043 2.3449 6.9327 17.082

Dist ph 8.6519 0.53481 7.977 17.164

Dist wang 8.7296 0.49483 8.0137 17.238

Dist dual 8.8065 0.47931 8.0416 17.327

Dist tvar 8.8941 0.47972 8.0693 17.443

Technical 9.59 0.47 14.64 24.7

ceded ceded ceded ceded

line Casualty PropertyC PropertyNC total

Method

Dist ccoc 2.5669 2.2788 3.6172 8.4632

Dist ph 2.6952 1.0135 4.5651 8.2738

Dist wang 2.784 0.98056 4.4253 8.1898

Dist dual 2.8917 0.96217 4.2413 8.0952

Dist tvar 3.0137 0.95009 4.0143 7.9781

Technical 4.41 1.53 2.36 8.3

2.13.7.3.3. Compare Model Value and Market Price

Focus on the last block above, under ceded. The rows Dist ... show the

model value of reinsurance according to each distortion. The row

Technical shows the market price. The market suggests to buy when the

value is greater than the price.

The analysis provides a clear answer only for casualty, where the model value of reinsurance is much lower than the market price for all distortions: don’t buy the reinsurance.

For property cat, CCoC, the most tail-centric distortion, sees a lot of value in the reinsurance — hardly surprising. All the other less tail-centric distortions do not see it as adding value overall (lower value than market price). The order of the distortions and their assessment of the value of cat reinsurance are perfectly aligned, as they were for casualty albeit in the opposite order.

For property non-cat, the PH and Wang distortions see value, the others do not, though dual is close. This is the most interesting case because the ranking does not agree with the distortion ordering (as it does for the other two units). Property non-cat contributes to volatility and tail-risk, and so is more nuanced. Management often struggles with property risk reinsurance because tail-centric measures understate the value it provides. Actuaries stuggle to find analytic methods that capture its management-perceived value. The range of distortions considered covers the two views well.

In total the program is not seen as good value by any of the distortions. Since they span the reasonable range of risk preferences, this is a robust result.

Management often cares about more than just tail risk and they generally rejects the findings from CCoC. Whether or not they see value in reinsurance is sensitive to their exact risk appetite. These findings are consistent with the fact that each company tends to structure its reinsurance differently, tailored to their own risk appetite. Difference in risk appetite have a material impact on decision making.

2.13.7.3.4. Analysis for Stop Loss Reinsurance

Here is the analysis for the stop loss reinsurance. This analysis is manual,

because the net of stop loss distribution for a Portfolio is not

currently built-in. We have to extract the relevant distributions and apply

the distortions, estimate a_stoploss the net asset requirement at

p=0.995 (rounded to be a multiple of bs), determine the net expected

loss and the model value. Recall compare.net_stoploss is the density of

the net of stop-loss loss outcome. S1 is used to create its survival

function, to which the distortion is applied to determine pricing. exa

and exag are the objective and risk adjusted losses (model value) given

an asset level a, computed as \(\int_0^a S\) and \(\int_0^a g

(S)\) respectively (see PIR REF). We then select the relevant row and assemble

the answer.

In [53]: S0 = pd.Series(compare.net_stoploss, index=compare.loss); \

....: S0.name = 'S'; \

....: S1 = S0[::-1].shift(1, fill_value=0).cumsum(); \

....: a0 = float(interp1d(S0.cumsum(), S0.index)(0.995)); \

....: a_stoploss = abcd.snap(a0); \

....: print(f'Net of stoploss assets {a_stoploss:.3f}');

....:

Net of stoploss assets 45.109

In [54]: net_el_stoploss_unlim = (compare.loss * compare.net_stoploss).sum(); \

....: net_el_stoploss = (np.minimum(compare.loss, a_stoploss) * compare.net_stoploss).sum(); \

....: epd = 1 - net_el_stoploss / net_el_stoploss_unlim; \

....: qd(pd.Series([net_el_stoploss_unlim, net_el_stoploss, epd], index=['unlimited net loss', 'net loss limited by assets', 'epd']));

....:

unlimited net loss 20.999

net loss limited by assets 20.941

epd 0.0027373

In [55]: pricer = S1.to_frame().sort_index();

In [56]: for nm, dist in abcd.dists.items():

....: pricer[f'{nm}_exa'] = pricer['S'].shift(1, fill_value=0).cumsum() * abcd.bs

....: pricer[f'{nm}_gS'] = dist.g(pricer.S)

....: pricer[f'{nm}_exag'] = pricer[f'{nm}_gS'].shift(1, fill_value=0).cumsum() * abcd.bs

....: pricer = pricer.sort_index()

....:

In [57]: try:

....: pricer = pricer.loc[[a_stoploss]]; \

....: pricer.columns = pricer.columns.str.split('_', expand=True); \

....: comp = pricer.stack(0).droplevel(0,0); \

....: comp.loc['Technical'] = [net_el_stoploss, tech_prem - 1.98, np.nan]; \

....: comp['stoploss_value'] = tech_prem - comp.exag; \

....: comp = comp.sort_values('stoploss_value', ascending=False); \

....: qd(comp)

....: except:

....: print('Unspecfied error: TODO investigate.')

....:

Unspecfied error: TODO investigate.

The output table reveals that the stop loss value is greater than its market price for the CCoC, PH, and Wang distortions, but less for the dual and TVaR. Thus, management averse to tail risk regard it as beneficial, but those more concerned with volatility and body risk do not see it as worthwhile.

A note of caution is in order on this analysis. Stop loss structures are a broker favorite, but are generally not liked by reinsurers. Aggregate features are hard to underwrite and price, and the lower premium is not attractive. A treaty similar to the proposed stop loss would be very hard to find in the market.

2.13.7.4. Visualizing Risk

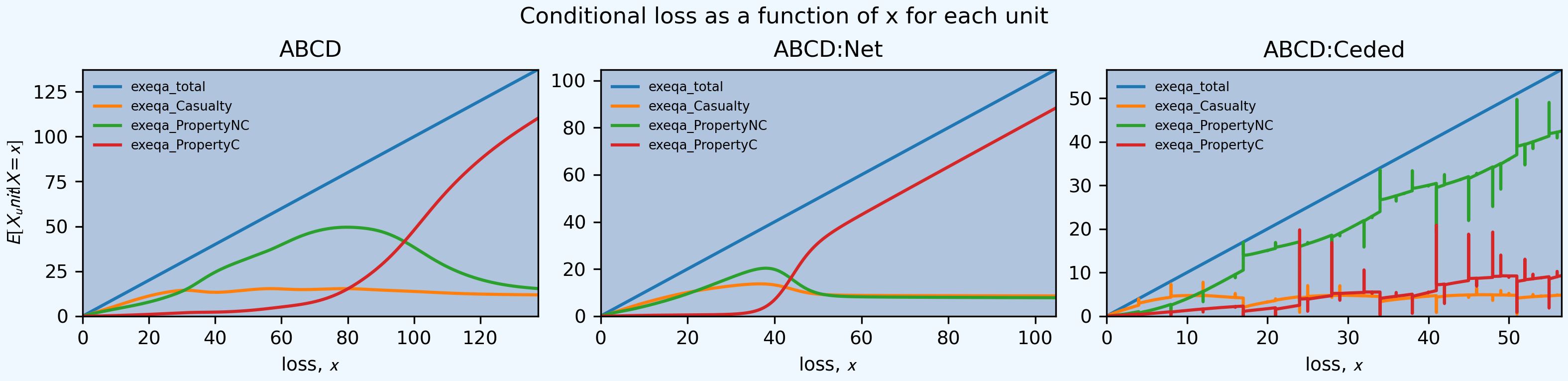

The next figure shows the kappa functions, a handy way to visualize which units are contributing to total risk across the loss spectrum (see REF). Here the horizontal axis is total loss. The middle plot shows the reinsurance is quite effective at lowering the risk from Property NC (green line), but less effective at altering the risk profile of the other two lines. In particular, cat (red line) still dominates the tail risk.

In [58]: fig, axs = plt.subplots(1, 3, figsize=(3 * 3.5, 2.55), constrained_layout=True)

In [59]: for ax, a in zip(axs.flat, [abcd, abcd_net, abcd_ceded]):

....: mx = a.q(0.9999)

....: a.density_df.filter(regex='exeqa_[CPt]').plot(ax=ax,

....: xlim=[0, mx], ylim=[0, mx], title=a.name);

....: ax.set(xlabel='loss, $x$');

....:

In [60]: axs.flat[0].set(ylabel='$E[X_unit | X=x]$');

In [61]: fig.suptitle('Conditional loss as a function of x for each unit');