2.13.4. Loss Data Analytics Book

Examples from Jed Frees’ open source actuarial software. Text and github source available on-line.

2.13.4.1. Contents

2.13.4.2. Distribution Examples

2.13.4.2.1. Gamma distribution

In [1]: import scipy.stats as ss

In [2]: import numpy as np

In [3]: import matplotlib.pyplot as plt

In [4]: xs = np.linspace(0, 1000, 1001)

In [5]: fig, axs = plt.subplots(1, 2, figsize=(2 * 3.5, 2.45), constrained_layout=True, squeeze=True)

In [6]: ax0, ax1 = axs.flat

In [7]: for scale in [100, 150, 200, 250]:

...: ax0.plot(xs, ss.gamma(2, scale=scale).pdf(xs), label=f'scale = {scale}')

...:

In [8]: for shape in [2, 3, 4, 5]:

...: ax1.plot(xs, ss.gamma(shape, scale=100).pdf(xs), label=f'shape = {shape}')

...:

In [9]: for ax in axs.flat:

...: ax.legend(loc='upper right')

...: ax.set(ylabel='gamma density', xlabel='x')

...:

2.13.4.2.2. Pareto distribution

In [10]: xs = np.linspace(0, 3000, 3001)

In [11]: fig, axs = plt.subplots(1, 2, figsize=(2 * 3.5, 2.45), constrained_layout=True, squeeze=True)

In [12]: ax0, ax1 = axs.flat

In [13]: for scale in [2000, 2500, 3000, 3500]:

....: ax0.plot(xs, ss.pareto(3, scale=scale, loc=-scale).pdf(xs), label=f'scale = {scale}')

....:

In [14]: for shape in [1,2,3,4]:

....: ax1.plot(xs, ss.pareto(shape, scale=2000, loc=-2000).pdf(xs), label=f'shape = {shape}')

....:

In [15]: for ax in axs.flat:

....: ax.legend(loc='upper right')

....: ax.set(ylabel='Pareto density', xlabel='x')

....:

2.13.4.2.3. Weibull distribution

scipy.stats includes Weibull min (for positive \(x\)) and Weibull max (for negative \(x\)) distributions. We want the min version.

In [16]: xs = np.linspace(0, 400, 401)

In [17]: fig, axs = plt.subplots(1, 2, figsize=(2 * 3.5, 2.45), constrained_layout=True, squeeze=True)

In [18]: ax0, ax1 = axs.flat

In [19]: for scale in [50, 100, 150, 200]:

....: ax0.plot(xs, ss.weibull_min(3, scale=scale).pdf(xs), label=f'scale = {scale}')

....:

In [20]: for shape in [1.5, 2, 2.5, 3]:

....: ax1.plot(xs, ss.weibull_min(shape, scale=100).pdf(xs), label=f'shape = {shape}')

....:

In [21]: for ax in axs.flat:

....: ax.legend(loc='upper right')

....: ax.set(ylabel='Weibull_min density', xlabel='x')

....:

2.13.4.3. Mixture Example (3.3.5)

A collection of insurance policies consists of two types. 25% of policies are Type 1 and 75% of policies are Type 2. For a policy of Type 1, the loss amount per year follows an exponential distribution with mean 200, and for a policy of Type 2, the loss amount per year follows a Pareto distribution with parameters \(\alpha=3\) and \(\theta=200\). For a policy chosen at random from the entire collection of both types of policies, find the probability that the annual loss will be less than 100, and find the average loss.

Solution. The function pmv (print mean and variance) is a convenience.

In [22]: from aggregate import build, qd, mv

In [23]: def pmv(m, v):

....: print(f'mean = {m:.6g}\n'

....: f'variance = {v:.7g}')

....:

Create the Aggregate object, display its describe dataframe and compare the cdf with the exact computation.

In [24]: a = build('agg lda.3.3.5 '

....: '1 claim '

....: 'sev [200 200] * [expon pareto] [1 3] + [0 -200] wts [.25 .75] '

....: 'fixed',

....: normalize=False)

....:

In [25]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1 0

Sev 125 125 -2.3123e-05 1.4832 1.4754 inf 9.9477

Agg 125 125 -2.3123e-05 1.4832 1.4754 inf 9.9477

log2 = 16, bandwidth = 1/2, validation: fails sev cv, agg cv.

In [26]: a.sev.cdf(100), 0.25 * (1 - np.exp(-0.5)) + 0.75 * (1 - (2/3)**3)

Out[26]: (0.6261451128496194, 0.6261451128496194)

This example has a very thick tailed severity and it is best to specify normalized=False for the most accurate severity estimates. With default settings,

aggregate suffers considerable discretization error, with an estimated mean well below the actual 125. The sev.cdf method exposes the actual underlying

severity distribution cdf functions and reproduces the requested probability exactly. The object cdf function relies on the discretization and so is shifted by

half a bucket size. (Also available: sev.sf and sev.pdf.)

In [27]: a.cdf(100), a.sev.cdf(100 + a.bs/2)

Out[27]: (0.626889166181137, 0.6268891661811365)

2.13.4.4. Coverage Modifications

Deductible Example (3.4.1)

A claim severity distribution is exponential with mean 1000. An insurance company will pay the amount of each claim in excess of a deductible of 100. Calculate the variance of the amount paid by the insurance company for one claim, including the possibility that the amount paid is 0.

Solution. In this case we must use unconditional severity to include the possibility that the amount paid is 0. This is done by adding ! at the end of the severity specification. The moments are computed exactly without updating.

In [28]: import numpy as np

In [29]: a = build('agg lda.3.4.1 1 claim '

....: 'inf xs 100 sev 1000 * expon 1 ! '

....: 'fixed', update=False)

....:

In [30]: qd(a)

E[X] CV(X) Skew(X)

X

Freq 1 0

Sev 904.84 1.1002 2.0257

Agg 904.84 1.1002 2.0257

log2 = 0, bandwidth = na, validation: n/a, not updated.

In [31]: m = 1000 * np.exp(-0.1)

In [32]: mv(a)

mean = 904.837

variance = 990944.1

std dev = 995.462

In [33]: pmv(m, (2 * 1000**2 * np.exp(-0.1)) - m**2)

mean = 904.837

variance = 990944.1

Deductible Example (3.4.2)

For an insurance:

Losses have a density function

\[\begin{split}f_{X}\left( x \right) = \left\{ \begin{matrix} 0.02x & 0 < x < 10, \\ 0 & \text{elsewhere.} \\ \end{matrix} \right.\end{split}\]The insurance has an ordinary deductible of 4 per loss.

\(Y^{P}\) is the claim payment per payment random variable.

Solution. The trick here is to realize that \(X\) is a beta variable with \(\alpha=2\) and \(\beta=1\).

In [34]: a = build('agg lda.3.4.2 1 claim 6 xs 4 sev 10 * beta 2 1 fixed')

In [35]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1 0

Sev 3.4286 3.4286 1.0348e-10 0.48947 0.48947 -0.29313 -0.29313

Agg 3.4286 3.4286 1.0348e-10 0.48947 0.48947 -0.29313 -0.29313

log2 = 16, bandwidth = 1/4096, validation: not unreasonable.

In [36]: mv(a)

mean = 3.42857

variance = 2.816327

std dev = 1.67819

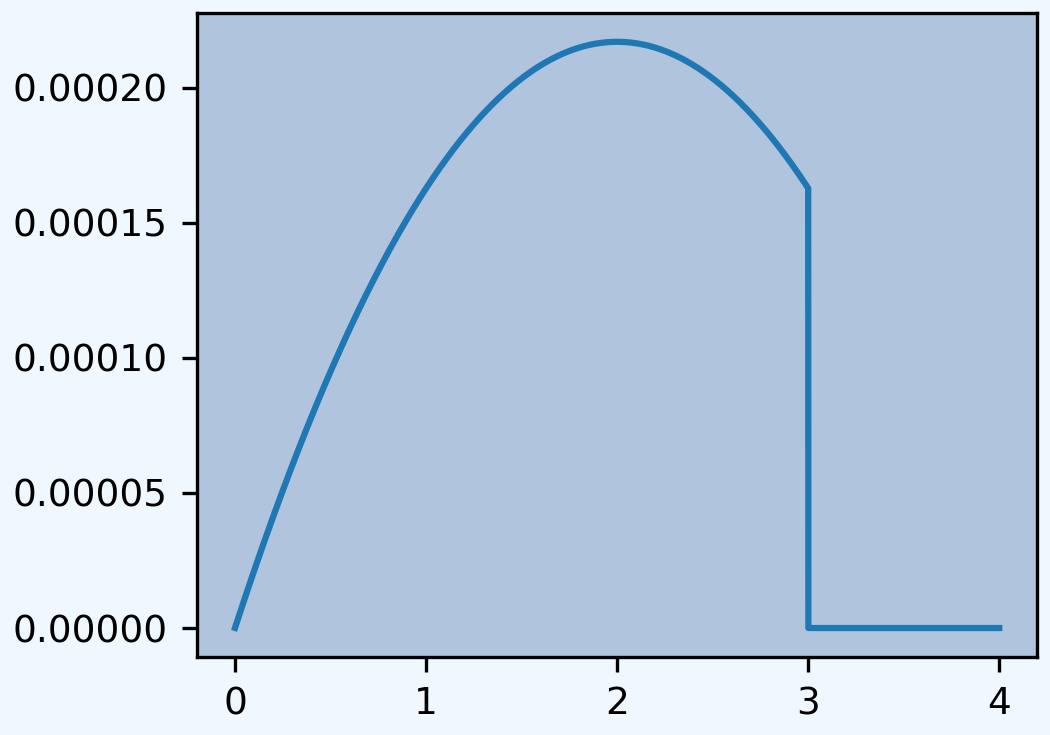

Limit Example (3.4.4)

Under a group insurance policy, an insurer agrees to pay 100% of the medical bills incurred during the year by employees of a small company, up to a maximum total of one million dollars. The total amount of bills incurred, \(X\), has pdf

where \(x\) is measured in millions. Calculate the total amount, in millions of dollars, the insurer would expect to pay under this policy.

Solution. In this case the distribution has no obvious parametric form—though it is related to a beta. We can solve it in aggregate by using a custom empirical distribution.

In [37]: xs = np.linspace(0, 4, 2**13, endpoint=False)

In [38]: F = np.where(xs<3,(xs * xs * (2 - xs / 3)) / 9, 1)

In [39]: ps = np.diff(F, append=1)

In [40]: fig, ax = plt.subplots(1, 1, figsize=(3.5, 2.45), constrained_layout=True, squeeze=True)

In [41]: ax.plot(xs, ps);

When the empirical distribution has many entries it is faster to build the Aggregate object directly, rather than use DecL. The moments of the severity and aggregate distribution are computed from the numerical approximation during creation. There is no need to update the object.

In [42]: from aggregate import Aggregate

In [43]: a = Aggregate('Example', exp_en=1, sev_name='dhistogram', sev_xs=xs, sev_ps=ps,

....: exp_attachment=0, exp_limit=1, freq_name='fixed')

....:

In [44]: print(a)

aggregate object name Example

claim count 1.00

frequency distribution fixed

severity distribution dhistogram, 1 xs 0.

E[X] CV(X) Skew(X)

X

Freq 1 0 NaN

Sev 0.93514 0.1826 -2.9018

Agg 0.93514 0.1826 -2.9018

Limit and Deductible Example (3.4.5)

The ground up loss random variable for a health insurance policy in 2006 is modeled with \(X\), a random variable with an exponential distribution having mean 1000. An insurance policy pays the loss above an ordinary deductible of 100, with a maximum annual payment of 500. The ground up loss random variable is expected to be 5% larger in 2007, but the insurance in 2007 has the same deductible and maximum payment as in 2006. Find the percentage increase in the expected cost per payment from 2006 to 2007.

Solution. Trend increases the ground-up severity distribution but not the limit and attachment. The calculation is performed exactly on creation; again, there is no need to update the Aggregate object.

In [45]: import pandas as pd

In [46]: a06 = build('agg X06 1 claim 500 xs 100 sev 1000 * expon fixed', update=False)

In [47]: a07 = build('agg X07 1 claim 500 xs 100 sev 1050 * expon fixed', update=False)

In [48]: ans = pd.concat((a06.describe, a07.describe), keys=['2006', '2007'])

In [49]: qd(ans)

E[X] CV(X) Skew(X)

X

2006 Freq 1 0 NaN

Sev 393.47 0.40656 -1.1717

Agg 393.47 0.40656 -1.1717

2007 Freq 1 0 NaN

Sev 397.8 0.39691 -1.2342

Agg 397.8 0.39691 -1.2342

In [50]: ans.iloc[5, 0] / ans.iloc[2, 0] - 1

Out[50]: 0.011000207063778467

Reinsurance Example (3.4.6, modified)

Losses arising in a certain portfolio have a two-parameter Pareto distribution with \(\alpha=5\) and \(\theta=3,600\). A reinsurance arrangement has been made, under which (a) the reinsurer accepts 15% of losses up to \(u=5,000\) and all amounts in excess of 5,000 and (b) the insurer pays for the remaining losses.

Express the random variables for the reinsurer’s and the insurer’s payments as a function of \(X\), the portfolio losses.

Calculate the mean amount paid on a single claim by the insurer.

Calculate the standard deviation of the amount paid on a single claim by the insurer (retaining the 15% copayment).

Solution. The net position can be modeled as:

agg insurer.net 1 claim

sev 3600 * pareto 5 - 3600

occurrence net of 0.15 so 5000 xs 0 and inf xs 5000

fixed

but this involves the thick-tailed Pareto across its entire range. It is better to recognize the severity is limited by the second excess layer and proceed as follows.

In [51]: a = build('agg insurer.net 1 claim '

....: '5000 xs 0 sev 3600 * pareto 5 - 3600 '

....: 'occurrence net of 0.15 so 5000 xs 0 '

....: 'fixed')

....:

In [52]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1 0

Sev 872.37 741.53 -0.14998 1.1256 1.1256 2.0952 2.0952

Agg 872.37 741.53 -0.14998 1.1256 1.1256 2.0952 2.0952

log2 = 16, bandwidth = 1/4, validation: n/a, reinsurance.

In [53]: print('\n', a.agg_m, a.agg_sd)

872.3650484486672 981.9314221673877

2.13.4.5. Aggregate Loss Distributions

Poisson/Discrete Example (5.3.1)

The number of accidents follows a Poisson distribution with mean 12. Each accident generates 1, 2, or 3 claimants with probabilities 1/2, 1/3, and 1/6 respectively.

Calculate the variance in the total number of claimants.

Solution.

In [54]: a = build('agg QU 12 claims dsev [1 2 3] [1/2 1/3 1/6] poisson')

In [55]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 12 0.28868 0.28868

Sev 1.6667 1.6667 -1.1102e-16 0.44721 0.44721 0.6261 0.6261

Agg 20 20 -7.9936e-15 0.31623 0.31623 0.36366 0.36366

log2 = 10, bandwidth = 1, validation: not unreasonable.

In [56]: mv(a)

mean = 20

variance = 40

std dev = 6.32456

As always, a contains the (exact) full distribution of outcomes. We could answer any question about it.

Discrete Example (5.3.2)

You are the producer of a television quiz show that gives cash prizes. The number of prizes, \(N\), and prize amount, \(X\), have the following distributions:

Your budget for prizes equals the expected aggregate cash prizes plus the standard deviation of aggregate cash prizes. Calculate your budget.

Solution. Just a matter of translating into DecL. No need to update the object.

In [57]: a = build('agg lda.5.3.2 dfreq [1 2] [.8 .2] '

....: 'dsev [0 100 1000] [.2 .7 .1]', update=False)

....:

In [58]: display(a)

lda.5.3.2, <aggregate.distributions.Aggregate object at 0x7f1b710cc1c0>

In [59]: mv(a)

mean = 204

variance = 98344

std dev = 313.598

In [60]: a.agg_m + a.agg_sd

Out[60]: 517.5984693840198

Geometric/Discrete Example (5.3.3 and 5.4.1)

The number of claims in a period has a geometric distribution with mean \(4\). The amount of each claim \(X\) follows \(\Pr(X=x) = 0.25, \ x=1,2,3,4\), i.e. a discrete uniform distribution on \(\{1,2,3,4\}\). The number of claims and the claim amounts are independent. Let \(S_N\) denote the aggregate claim amount in the period. Calculate \(F_{S_N}(3)\).

Solution. We can compute the entire distribution. Here we show up to the 99th percentile. If the probability clause in dsev is omitted then all outcomes are treated as equally likely.

In [61]: a = build('agg lda.5.3.3 4 claims dsev [1:4] geometric')

In [62]: qd(a, accuracy=4)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 4 1.118 2.0125

Sev 2.5 2.5 0 0.44721 0.44721 0 0

Agg 10 10 -1.9499e-10 1.1402 1.1402 2.024 2.024

log2 = 8, bandwidth = 1, validation: not unreasonable.

In [63]: b = a.density_df.loc[0:a.q(0.99), ['p_total', 'F']]

In [64]: b.index = b.index.astype(int)

In [65]: qd(b, accuracy=4)

p_total F

loss

0 0.2 0.2

1 0.04 0.24

2 0.048 0.288

3 0.0576 0.3456

4 0.06912 0.41472

5 0.042944 0.45766

6 0.043533 0.5012

7 0.042639 0.54384

8 0.039647 0.58348

9 0.033753 0.61724

10 0.031914 0.64915

11 0.029591 0.67874

... ... ...

40 0.0023287 0.97449

41 0.0021339 0.97662

42 0.0019554 0.97858

43 0.0017918 0.98037

44 0.001642 0.98201

45 0.0015046 0.98352

46 0.0013788 0.9849

47 0.0012634 0.98616

48 0.0011577 0.98732

49 0.0010609 0.98838

50 0.00097217 0.98935

51 0.00089085 0.99024

Moments Example (5.3.4)

You are given:

As a benchmark, use the normal approximation to determine the probability that the aggregate loss will exceed 150% of the expected loss.

Solution. Use the MomentAggregator class to compute the moments of an aggregate from those of frequency and severity.

In [66]: import scipy.stats as ss

In [67]: from aggregate import MomentAggregator

In [68]: mom = MomentAggregator.agg_from_fs2(8, 9, 10000, 3937**2)

In [69]: fz = ss.norm(loc=mom.ex, scale=mom.sd)

In [70]: mom['prob'] = fz.sf(1.5*mom.ex)

In [71]: qd(mom)

ex 80000

var 1.024e+09

sd 32000

cv 0.4

prob 0.10565

Poisson/Uniform Example (5.3.5 and 5.4.2)

For an individual over 65:

The number of pharmacy claims is a Poisson random variable with mean 25.

The amount of each pharmacy claim is uniformly distributed between 5 and 95.

The amounts of the claims and the number of claims are mutually independent.

Estimate the probability that aggregate claims for this individual will exceed 2000 using the normal approximation.

Solution. Here is a close-to exact solution in addition to the normal approximation. Note that the uniform distribution has no shape parameter. The severity is made by shifting and scaling the base. Scaling is like multiplication and is applied before the location (addition) shift.

In [72]: a = build('agg Pharma 25 claims sev 90 * uniform + 5 poisson')

In [73]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 25 0.2 0.2

Sev 50 50 0 0.51962 0.51962 0 0

Agg 1250 1250 2.6645e-15 0.22539 0.22539 0.25293 0.25293

log2 = 16, bandwidth = 1/16, validation: not unreasonable.

Here are the moments for the approximation. The approximate function returns a scipy.stats frozen normal object, which yields the approximation.

In [74]: print(a.sf(2000), a.agg_m, a.agg_var)

0.00698200305408303 1250.0 79375.0

In [75]: fz = a.approximate('norm')

In [76]: fz.sf(2000), a.sf(2000)

Out[76]: (0.0038830948902722645, 0.00698200305408303)

approximate will also provide (shifted) gamma and lognormal fits.

In [77]: approx = a.approximate('all')

In [78]: b = pd.DataFrame([[k, v.sf(2000)] for k, v in approx.items()],

....: columns=['approx', 'prob']).set_index('approx')

....:

In [79]: b.loc['exact'] = a.sf(2000)

In [80]: b.sort_values('prob')

Out[80]:

prob

approx

norm 0.003883

exact 0.006982

sgamma 0.007101

slognorm 0.007175

gamma 0.009789

lognorm 0.013118

Here is a comparison of the FFT model with the normal approximation. Example 5.4.2 derives a similar probability using simulation.

In [81]: fig, ax = plt.subplots(1, 1, figsize=(3.5, 2.45), constrained_layout=True, squeeze=True)

In [82]: (a.density_df.p / a.bs).plot(label='Exact', ax=ax);

In [83]: ax.plot(a.xs, fz.pdf(a.xs), label='Normal approx');

In [84]: ax.set(xlim=[0, 3000], title='Normal approximation');

In [85]: ax.legend(loc='upper right');

Geometric/Discrete Example (5.3.6 and 5.3.7)

In a given week, the number of projects that require you to work overtime has a geometric distribution with \(\beta=2\). For each project, the distribution of the number of overtime hours in the week, \(X\), is as follows:

The number of projects and the number of overtime hours are independent. You will get paid for overtime hours in excess of 15 hours in the week. Calculate the expected number of overtime hours for which you will get paid in the week.

Solution. This is a one-liner in aggregate. Remember that aggregate reinsurance is specified after the frequency clause. The first column in the describe dataframe shows the analytic gross answer and the second the FFT-computed net.

In [86]: a = build('agg Projects 2 claims '

....: 'dsev [5 10 20] [.2 .3 .5] geometric '

....: 'aggregate net of 15 xs 0')

....:

In [87]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2 1.2247 2.0412

Sev 14 14 0 0.44607 0.44607 -0.23403 -0.23403

Agg 28 18.807 -0.32831 1.2647 1.6713 2.0725 2.6373

log2 = 9, bandwidth = 1, validation: n/a, reinsurance.

Example 5.3.7 uses a recursive calculation in steps of 5. We can replicate that using an aggregate tower. The reinsurance_audit_df provides ceded and net statistics by layer. Here we extract just the ceded part to get the excess (overtime).

In [88]: a1 = build('agg Projects.1 2 claims '

....: 'dsev [5 10 20] [.2 .3 .5] geometric '

....: 'aggregate net of tower [0 5 10 15 inf]')

....:

In [89]: b = a1.reinsurance_audit_df.xs('ceded', axis=1, level=0)

In [90]: b['cumul ex'] = b.ex[::-1].cumsum() - a.agg_m

In [91]: qd(b, accuracy=4)

ex var sd cv skew cumul ex

kind share limit attach

agg 1.0 5.0 0.0 3.3333 5.5556 2.357 0.70711 -0.70711 28

5.0 3.1111 5.8765 2.4242 0.77919 -0.50418 24.666

10.0 2.7481 6.1884 2.4877 0.90521 -0.1995 21.555

inf 15.0 18.807 988 31.433 1.6713 2.6373 18.807

all inf gup 28 1253.9 35.41 1.2647 2.0713 -0.00026862

Zero-Modified Poisson/Burr Example (5.5.4)

Aggregate losses are modeled as follows:

The number of losses follows a zero-modified Poisson distribution with \(\lambda=3\) and \(p_0^M = 0.5\).

The amount of each loss has a Burr distribution with \(\alpha=3, \theta=50, \gamma=1\).

There is a deductible of \(d=30\) on each loss.

The number of losses and the amounts of the losses are mutually independent.

Calculate \(\mathsf{E}(N^P)\) and \(\mathsf{Var}(N^P)\).

Solution.

Todo

Implement ZT and ZM!

Negative Binomial Example (5.5.5 and 5.5.6 modified)

A group dental policy has a negative binomial claim count distribution with mean 300 and variance 800. Ground-up severity is given by the following table:

You expect severity to increase 50% with no change in frequency. You decide to impose a per claim deductible of 100. Calculate the expected total claim payment \(S\) after these changes. What is the variance of the total claim payment, \(\mathsf{Var}(S)\)? (Modified:) Compare the aggregate distributions before and after the policy change.

Solution. A negative binomial with mean 300 and variance 800 has \(8/3 = 1 + 300c\) and giving a mixing cv of \(\sqrt{c}=(5/900)^{0.5}=0.0745\). Hence the aggregate program is

TODO: why is the answer not exact?

In [92]: cv = ((8 / 3 - 1) / 300)**0.5

In [93]: a0 = build(f'agg Original 300 claims dsev [4 8 12 20] mixed gamma {cv}')

In [94]: a1 = build(f'agg Revised 300 claims inf xs 10 '

....: f'sev dhistogram xps [{4*1.5} {8*1.5} {12*1.5} {20*1.5}] ! mixed gamma {cv}')

....:

In [95]: qd(a0)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 300 0.094281 0.15321

Sev 11 11 0 0.53783 0.53783 0.43465 0.43465

Agg 3300 3300 -3.3207e-13 0.099263 0.099263 0.15833 0.15832

log2 = 20, bandwidth = 1, validation: not unreasonable.

In [96]: qd(a1)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 300 0.094281 0.15321

Sev 7.5 7.5 4.6567e-11 1.0392 1.0392 0.7207 0.7207

Agg 2250 2250 4.4878e-11 0.11175 0.11175 0.16722 0.16669

log2 = 20, bandwidth = 1, validation: not unreasonable.

In [97]: mv(a0)

mean = 3300

variance = 107300

std dev = 327.567

In [98]: mv(a1)

mean = 2250

variance = 63225

std dev = 251.446

Here is a comparison of the two densities.

In [99]: fig, ax = plt.subplots(1, 1, figsize=(3.5, 2.45), constrained_layout=True, squeeze=True)

In [100]: a0.density_df.p_total.plot(ax=ax, label='Original');

In [101]: a1.density_df.p_total.plot(ax=ax, label='Adjusted');

In [102]: ax.set(xlim=[-10, 1.25 * a0.q(0.9999)]);

In [103]: ax.legend(loc='upper right');

Poisson/Exponential Coverage and Underwriting Modification (Example 5.5.7)

A company insures a fleet of vehicles. Aggregate losses have a compound Poisson distribution. The expected number of losses is 20. Loss amounts, regardless of vehicle type, have exponential distribution with \(\theta=200\). To reduce the cost of the insurance, two modifications are to be made:

A certain type of vehicle will not be insured. It is estimated that this will reduce loss frequency by 20%.

A deductible of 100 per loss will be imposed.

Calculate the expected aggregate amount paid by the insurer after the modifications.

Solution. The ! at the end of the severity clause indicates unconditional severity (including zero claims that fail to meet the deductible).

In [104]: a = build(f'agg Auto {20 * 0.8} claims inf xs 100 sev 200 * expon ! poisson')

In [105]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 16 0.25 0.25

Sev 121.31 121.31 -6.5104e-08 1.5157 1.5157 2.4172 2.4172

Agg 1940.9 1940.9 -6.5104e-08 0.45397 0.45397 0.68096 0.68096

log2 = 16, bandwidth = 1/4, validation: not unreasonable.

If severity is conditional there are 16 claims in excess of the deductible, giving a much higher number. The mean severity is still 200 because of the exponential’s memoryless property.

In [106]: a = build(f'agg Auto {20 * 0.8} claims inf xs 100 sev 200 * expon poisson')

In [107]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 16 0.25 0.25

Sev 200 200 -6.5104e-08 1 1 2 2

Agg 3200 3200 -6.5104e-08 0.35355 0.35355 0.53033 0.53033

log2 = 16, bandwidth = 1/4, validation: not unreasonable.

2.13.4.6. Portfolio Management

VaR for a Discrete Variable Example (10.3.4)

Consider an insurance loss random variable with the following probability distribution:

Determine the VaR at \(q = 0.6, 0.9, 0.95, 0.95001\).

Solution.

In [108]: a = build('agg VaR 1 claim dsev [1 3 4] [.75 .2 .05] fixed')

In [109]: [a.q(i) for i in [.6, .9, .95, .9501]]

Out[109]: [1.0, 3.0, 3.0, 4.0]

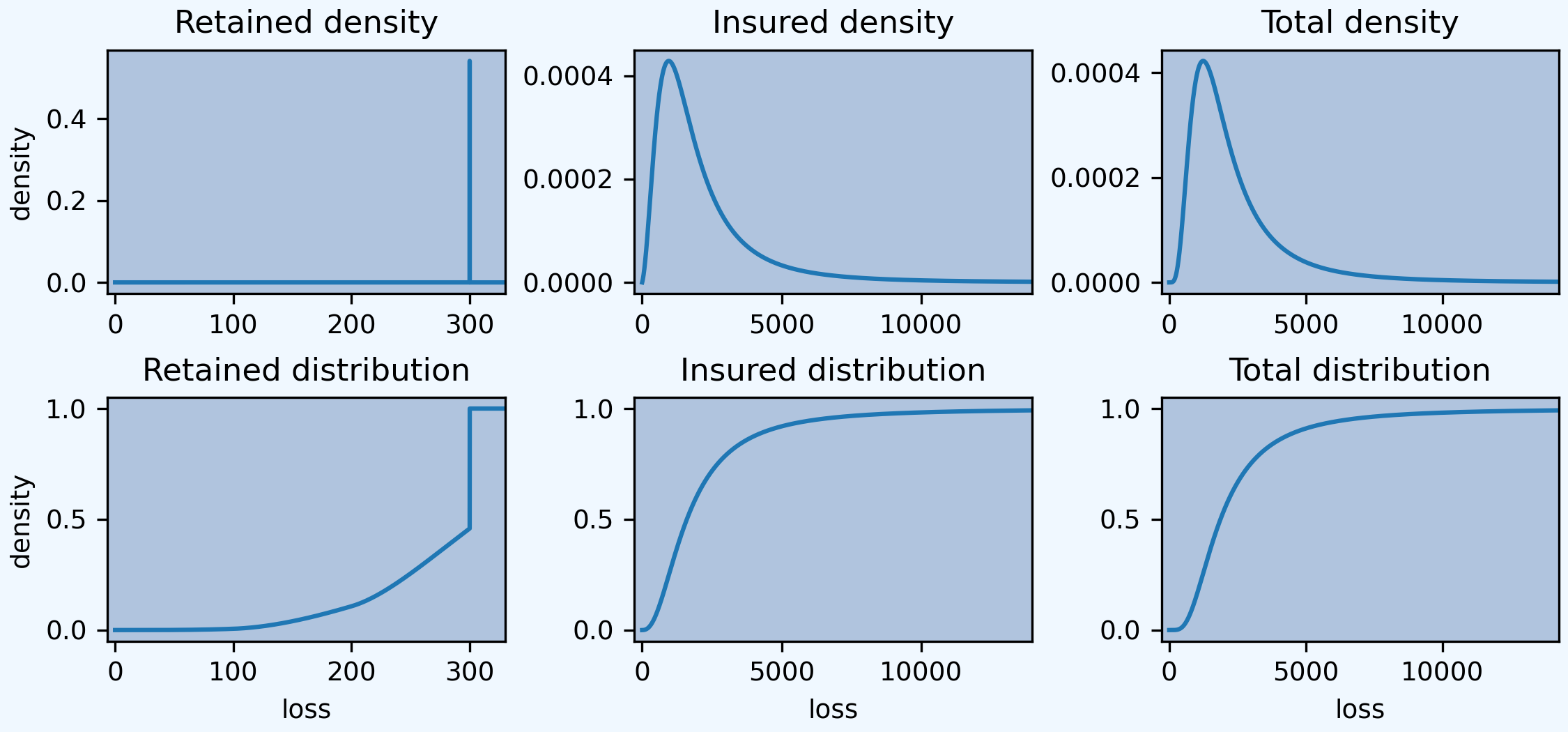

Multi-Unit Telecom Management Example (10.4.3.3)

You are the Chief Risk Officer of a telecommunications firm. Your firm has several property and liability risks. We will consider:

\(X_1\), buildings, modeled using a gamma distribution with mean 200 and scale parameter 100.

\(X_2\), motor vehicles, modeled using a gamma distribution with mean 400 and scale parameter 200.

\(X_3\), directors and executive officers risk, modeled using a Pareto distribution with mean 1000 and scale parameter 1000.

\(X_4\), cyber risks, modeled using a Pareto distribution with mean 1000 and scale parameter 2000.

Denote the total risk as \(X = X_1 + X_2 + X_3 + X_4\). For simplicity, you assume that these risks are independent. (Later, we will consider the more complex case of dependence.)

To manage the risk, you seek some insurance protection. You wish to manage internally small building and motor vehicles amounts, up to \(M_1\) and \(M_2\), respectively. You seek insurance to cover all other risks. Specifically, the insurer’s portion is

so that your retained risk is \(Y_{retained}= X - Y_{insurer} = \min(X_1,M_1) + \min(X_2,M_2)\). Using deductibles \(M_1=\) 100 and \(M_2=\) 200:

Determine the expected claim amount of (i) that retained, (ii) that accepted by the insurer, and (iii) the total overall amount.

Determine the 80th, 90th, 95th, and 99th percentiles for (i) that retained, (ii) that accepted by the insurer, and (iii) the total overall amount.

Compare the distributions by plotting the densities for (i) that retained, (ii) that accepted by the insurer, and (iii) the total overall amount.

Solution. Begin by figuring the gamma and Pareto parameters. For a gamma, the mean equals shape times scale, so shape equals 2 for building and motor. For a Pareto, the mean equals scale / (shape - 1), so shape equals 2 (no variance) for D&O and 3 for cyber (no third moment). We model the results using three Portfolio objects, one for the retention, one for the insured amount, and one total. In each case the distribution gives total losses; the frequency component is trivial.

Since the insured and total aggregates have no variance it is hard to estimate an appropriate bucket size. The default method uses the standard deviation as a scale factor. We must use judgement (or trial and error), and select log2=18 and bs=1 to ensure there is enough “space”. Checking the describe dataframe shows these values match the means well by unit and in total. The insured severity must be made unconditional.

In [110]: from aggregate import build

In [111]: retained = build('''port retained

.....: agg building 1 claim 100 xs 0 sev 100 * gamma 2 fixed

.....: agg motor 1 claim 200 xs 0 sev 200 * gamma 2 fixed

.....: ''')

.....:

In [112]: qd(retained)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

building Freq 1 0

Sev 89.636 89.636 1.0437e-10 0.23985 0.23985 -2.1029 -2.1029

Agg 89.636 89.636 1.0437e-10 0.23985 0.23985 -2.1029 -2.1029

motor Freq 1 0

Sev 179.27 179.27 2.6093e-11 0.23985 0.23985 -2.1029 -2.1029

Agg 179.27 179.27 2.6093e-11 0.23985 0.23985 -2.1029 -2.1029

total Freq 2 0

Sev 134.45 134.45 5.2187e-11 0.41837 -0.0046

Agg 268.91 268.91 5.2187e-11 0.17878 0.17878 -1.6928 -1.6928

log2 = 16, bandwidth = 1/128, validation: not unreasonable.

In [113]: insured = build('''port insured

.....: agg building 1 claim inf xs 100 sev 100 * gamma 2 ! fixed

.....: agg motor 1 claim inf xs 200 sev 200 * gamma 2 ! fixed

.....: agg d.and.o 1 claim sev 1000 * pareto 2 - 1000 fixed

.....: agg cyber 1 claim sev 2000 * pareto 3 - 2000 fixed

.....: ''', log2=18, bs=1)

.....:

In [114]: qd(insured)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

building Freq 1 0

Sev 110.36 110.36 -1.3889e-06 1.1901 1.1901 1.757 1.757

Agg 110.36 110.36 -1.3889e-06 1.1901 1.1901 1.757 1.757

motor Freq 1 0

Sev 220.73 220.73 -3.4722e-07 1.1901 1.1901 1.757 1.757

Agg 220.73 220.73 -3.4722e-07 1.1901 1.1901 1.757 1.757

d.and.o Freq 1 0

Sev 1000 992.43 -0.0075717 inf 2.6992 24.633

Agg 1000 992.43 -0.0075717 inf 2.6992 24.633

cyber Freq 1 0

Sev 1000 999.83 -0.00017075 1.7321 1.7062 inf 12.894

Agg 1000 999.83 -0.00017075 1.7321 1.7062 inf 12.894

total Freq 4 0

Sev 582.77 580.84 -0.0033215 inf

Agg 2331.1 2323.3 -0.0033392 inf 1.3721 16.508

log2 = 18, bandwidth = 1, validation: fails sev mean, agg mean.

In [115]: total = build('''port total

.....: agg building 1 claim sev 100 * gamma 2 fixed

.....: agg motor 1 claim sev 200 * gamma 2 fixed

.....: agg d.and.o 1 claim sev 1000 * pareto 2 - 1000 fixed

.....: agg cyber 1 claim sev 2000 * pareto 3 - 2000 fixed

.....: ''', log2=18, bs=1)

.....:

In [116]: qd(total)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

building Freq 1 0

Sev 200 200 -1.2153e-11 0.70711 0.70711 1.4142 1.4142

Agg 200 200 -1.2153e-11 0.70711 0.70711 1.4142 1.4142

motor Freq 1 0

Sev 400 400 -7.5939e-13 0.70711 0.70711 1.4142 1.4142

Agg 400 400 -7.5939e-13 0.70711 0.70711 1.4142 1.4142

d.and.o Freq 1 0

Sev 1000 992.43 -0.0075717 inf 2.6992 24.633

Agg 1000 992.43 -0.0075717 inf 2.6992 24.633

cyber Freq 1 0

Sev 1000 999.83 -0.00017075 1.7321 1.7062 inf 12.894

Agg 1000 999.83 -0.00017075 1.7321 1.7062 inf 12.894

total Freq 4 0

Sev 650 648.06 -0.0029779 inf

Agg 2600 2592.2 -0.0029969 inf 1.2304 16.463

log2 = 18, bandwidth = 1, validation: fails sev mean, agg mean.

The spacing in the agg programs is for clarity. We could also program using dfreq as agg motor dfreq [1] 100 xs 0 sev.... Next, assemble the requested data elements.

In [117]: pfs = [retained, insured, total]

In [118]: answers = pd.DataFrame(columns=['retained', 'insured', 'total'])

In [119]: answers.index.name = 'statistic'

In [120]: answers.loc['expected claim amount'] = [x.agg_m for x in pfs]

In [121]: for p in [.8, .9, .95, .99]:

.....: answers.loc[f'claim p_{p:.2f}'] = [x.q(p) for x in pfs]

.....:

In [122]: qd(answers)

retained insured total

statistic

expected claim amount 268.91 2331.1 2600

claim p_0.80 300 3090 3364

claim p_0.90 300 4483 4756

claim p_0.95 300 6244 6516

claim p_0.99 300 12706 12977

Finally, plot the densities. Compared to the text plot, the FFT reveals a discontinuous distribution for retained loss, with a large mass at 300. This is clearer on the lower plots, which show the distribution functions.

In [123]: fig, axs = plt.subplots(2, 3, figsize=(7.5, 3.5), constrained_layout=True, squeeze=True)

In [124]: xl = {}

In [125]: for ax, pf in zip(axs.flat, pfs):

.....: pf.density_df.p_total.plot(ax=ax)

.....: q = pf.q(0.99) * 1.1

.....: xl[hash(pf)] = [-q / 50, q]

.....: ax.set(xlim=xl[hash(pf)], title=pf.name.title() + ' density')

.....: if pf is retained:

.....: ax.set(ylabel='density')

.....:

In [126]: for ax, pf in zip(axs.flat[3:], pfs):

.....: pf.density_df.F.plot(ax=ax)

.....: ax.set(xlim=xl[hash(pf)], title=pf.name.title() + ' distribution', xlabel='loss')

.....: if pf is retained:

.....: ax.set(ylabel='density')

.....: