2.13.6. Bahnemann Monograph

Examples from the CAS published monograph Bahnemann [2015], Distributions for actuaries, which is a text for CAS Part 8. It is available for free on the [CAS Website](https://www.casact.org/monograph/cas-monograph-no-2).

2.13.6.1. Contents

Chapter 4: Aggregate Claims

2.13.6.2. Simple Discrete Aggregate, Example 4.1

Assume that n = 0, 1, 2 are the only possible numbers of claims and they occur with probabilities 0.6, 0.3 and 0.1, and that there exist just three potential claim sizes: 1, 2, and 3 with probabilities 0.4, 0.5 and 0.1. (Note: the text uses claim sizes 100, 200 and 300.) Compute the distribution of possible outcomes and its mean and variance.

Imports and convenience functions.

In [1]: from aggregate import build, qd, mv

In [2]: import matplotlib.pyplot as plt

Build the aggregate and display key statistics.

In [3]: a = build('agg Bahn.4.1 dfreq[0 1 2][.6 .3 .1] '

...: 'dsev[1 2 3][.4 .5 .1]')

...:

In [4]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.5 1.3416 0.99381

Sev 1.7 1.7 -1.1102e-16 0.37665 0.37665 0.36568 0.36568

Agg 0.85 0.85 -2.2204e-16 1.4435 1.4435 1.3333 1.3333

log2 = 4, bandwidth = 1, validation: not unreasonable.

In [5]: mv(a)

mean = 0.85

variance = 1.5055

std dev = 1.22699

Display all possible outcomes. Compare with the table on p. 107.

In [6]: qd(a.density_df.query('p_total > 0') [['p_total', 'F']])

p_total F

loss

0.0 0.6 0.6

1.0 0.12 0.72

2.0 0.166 0.886

3.0 0.07 0.956

4.0 0.033 0.989

5.0 0.01 0.999

6.0 0.001 1

2.13.6.3. Poisson-Gamma (Tweedie) Aggregate, Example 4.2

The text considers a Tweedie with expected claim count \(\lambda=2.5\) and gammma shape 3 and scale 400. It computes the mean, variance and skewness, and uses the series expansion for the distribution to compute the CDF at various points (Table 4.1). These results can be replicated as follows.

In [7]: a = build('agg Bahn.4.2 2.5 claims '

...: 'sev 400 * gamma 3 poisson')

...:

In [8]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2.5 0.63246 0.63246

Sev 1200 1200 1.5543e-15 0.57735 0.57735 1.1547 1.1547

Agg 3000 3000 -2.7578e-13 0.7303 0.7303 0.91287 0.91287

log2 = 16, bandwidth = 1/2, validation: not unreasonable.

In [9]: mv(a)

mean = 3000

variance = 4800000

std dev = 2190.89

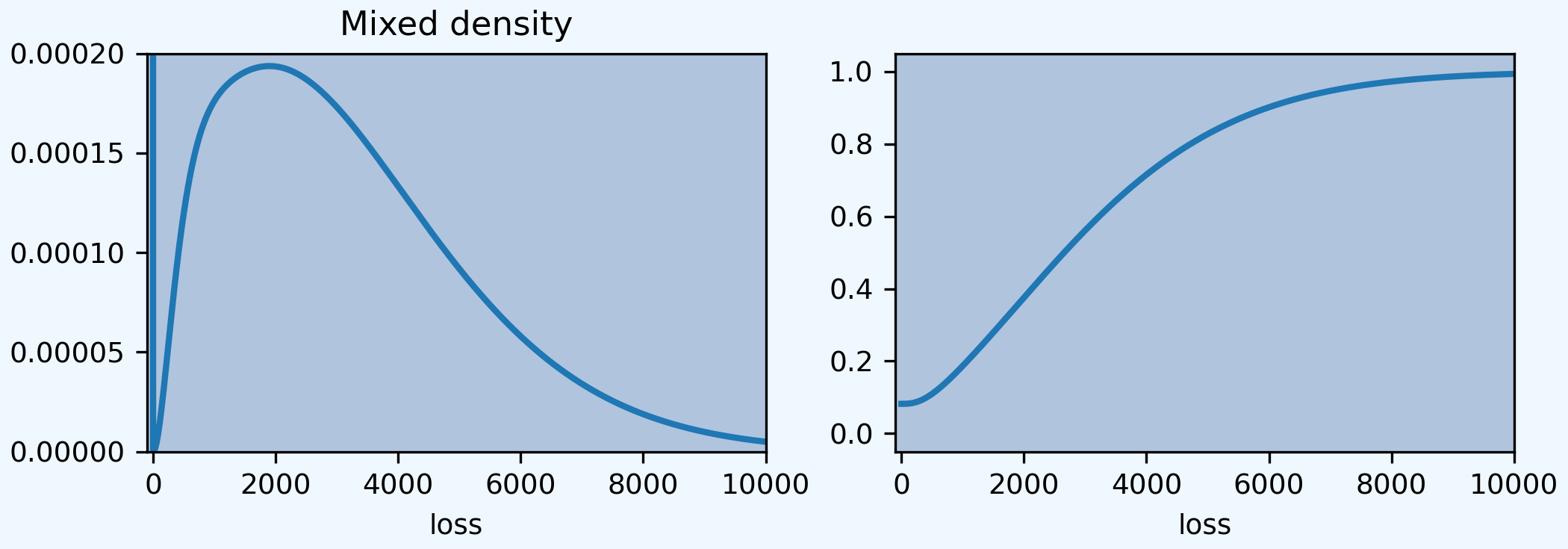

Extract various points of the pmf, cdf, and sf. The adjustment to the index is cosmetic. aggregate returns the entire distribution. The left plot shows the mixed density, with a mass at zero; right shows the cdf.

In [10]: bit = a.density_df.loc[

....: sorted(np.hstack((500, np.arange(0, 10000.5, 1000)))),

....: ['p', 'F', 'S']]

....:

In [11]: qd(bit, accuracy=4)

p F S

loss

0.0 0.082085 0.082085 0.91792

500.0 5.9764e-05 0.10958 0.89042

1000.0 8.8058e-05 0.18677 0.81323

2000.0 9.6726e-05 0.37558 0.62442

3000.0 8.6514e-05 0.56132 0.43868

4000.0 6.6611e-05 0.71519 0.28481

5000.0 4.5895e-05 0.82731 0.17269

6000.0 2.8971e-05 0.90135 0.098646

7000.0 1.7022e-05 0.94653 0.053468

8000.0 9.4148e-06 0.97234 0.027662

9000.0 4.9432e-06 0.98627 0.013727

10000.0 2.4799e-06 0.99344 0.006561

In [12]: fig, axs = plt.subplots(1, 2, figsize=(3.5*2, 2.45), constrained_layout=True, squeeze=True)

In [13]: ax0, ax1 = axs.flat

In [14]: (a.density_df.p / a.bs).plot(ylim=[0, 0.0002], xlim=[-100, 10000], lw=2, ax=ax0)

Out[14]: <Axes: xlabel='loss'>

In [15]: ax0.set(title='Density')

Out[15]: [Text(0.5, 1.0, 'Density')]

In [16]: a.density_df.F.plot(ylim=[-0.05, 1.05], xlim=[-100, 10000], lw=2, ax=ax1)

Out[16]: <Axes: xlabel='loss'>

In [17]: ax0.set(title='Mixed density');

In [18]: ax1.set(title='Distribution function');

2.13.6.4. Approximations to the Tweedie, Example 4.3

aggregate largely circumvents the need for approximations, but it does support their creation. The following reproduces Table 4.3.

In [19]: fz = a.approximate('all')

In [20]: bit['Normal'] = fz['norm'].cdf(bit.index)

In [21]: bit['Norm err'] = bit.Normal / bit.F - 1

In [22]: bit['sGamma'] = fz['sgamma'].cdf(bit.index)

In [23]: bit['sGamma err'] = bit.sGamma / bit.F - 1

In [24]: qd(bit, accuracy=4)

p F S Normal Norm err sGamma sGamma err

loss

0.0 0.082085 0.082085 0.91792 0.085452 0.041016 0.045932 -0.44044

500.0 5.9764e-05 0.10958 0.89042 0.12692 0.15821 0.10104 -0.077947

1000.0 8.8058e-05 0.18677 0.81323 0.18066 -0.032733 0.17751 -0.049594

2000.0 9.6726e-05 0.37558 0.62442 0.32404 -0.13723 0.36803 -0.020087

3000.0 8.6514e-05 0.56132 0.43868 0.5 -0.10924 0.56073 -0.0010453

4000.0 6.6611e-05 0.71519 0.28481 0.67596 -0.054848 0.71854 0.0046875

5000.0 4.5895e-05 0.82731 0.17269 0.81934 -0.0096235 0.83105 0.0045249

6000.0 2.8971e-05 0.90135 0.098646 0.91455 0.014639 0.90379 0.0027037

7000.0 1.7022e-05 0.94653 0.053468 0.96606 0.020626 0.94752 0.0010466

8000.0 9.4148e-06 0.97234 0.027662 0.98876 0.01689 0.97238 4.3133e-05

9000.0 4.9432e-06 0.98627 0.013727 0.99692 0.01079 0.98589 -0.00038586

10000.0 2.4799e-06 0.99344 0.006561 0.9993 0.0059007 0.99298 -0.00046669

Here is Table 4.4. The FFT overstates \(F(0)\) because of discretization error.

In [25]: a2 = build('agg Bahn.4.2b 10 claims '

....: 'sev 6000 * gamma 0.05 poisson')

....:

In [26]: qd(a2)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 10 0.31623 0.31623

Sev 300 299.94 -0.00018672 4.4721 4.473 8.9443 8.9441

Agg 3000 2999.4 -0.00018672 1.4491 1.4494 2.8293 2.8293

log2 = 16, bandwidth = 5, validation: fails sev mean, agg mean.

In [27]: fz = a2.approximate('all')

In [28]: bit = a2.density_df.loc[

....: sorted(np.hstack((500, np.arange(0, 20000, 2000)))),

....: ['p', 'F', 'S']]

....:

In [29]: bit['Normal'] = fz['norm'].cdf(bit.index)

In [30]: bit['Norm err'] = bit.Normal / bit.F - 1

In [31]: bit['sGamma'] = fz['sgamma'].cdf(bit.index)

In [32]: bit['sGamma err'] = bit.sGamma / bit.F - 1

In [33]: qd(bit, accuracy=4)

p F S Normal Norm err sGamma sGamma err

loss

0.0 0.047861 0.047861 0.95214 0.24512 4.1215 0.12322 1.5746

500.0 0.0014101 0.33964 0.66036 0.28267 -0.16774 0.33446 -0.015242

2000.0 0.00055391 0.59253 0.40747 0.40909 -0.30959 0.5887 -0.0064723

4000.0 0.00028651 0.75148 0.24852 0.59101 -0.21353 0.75043 -0.0013915

6000.0 0.00017056 0.84025 0.15975 0.75496 -0.1015 0.84022 -3.1891e-05

8000.0 0.00010741 0.89466 0.10534 0.87498 -0.022001 0.89493 0.00030275

10000.0 6.9725e-05 0.92946 0.070541 0.94633 0.018153 0.92976 0.0003232

12000.0 4.6131e-05 0.95227 0.047735 0.98079 0.029954 0.95251 0.00025575

14000.0 3.0919e-05 0.96745 0.032549 0.9943 0.027755 0.96762 0.00017682

16000.0 2.0919e-05 0.97768 0.022323 0.99861 0.021408 0.97779 0.00011036

18000.0 1.4255e-05 0.98462 0.01538 0.99972 0.015336 0.98468 6.1254e-05

2.13.6.5. Poisson-Discrete Distribution, Example 4.4

The claim-count random variable is Poisson distributed with mean 1.75. Severity has a discrete distribution with outcomes 1, 2, 3, 4, 5 occurring with probabilities 0.2, 0.4, 0.2, 0.15, 0.05 respectively. Compute the aggregate distribution.

Here is Table 4.5.

In [34]: a = build('agg Bahn.4.4 1.75 claims '

....: 'dsev [1 2 3 4 5] [.2 .4 .2 .15 .05] '

....: 'poisson')

....:

In [35]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1.75 0.75593 0.75593

Sev 2.45 2.45 -2.2204e-16 0.45588 0.45588 0.55603 0.55603

Agg 4.2875 4.2875 2.2204e-16 0.83078 0.83078 0.95453 0.95453

log2 = 7, bandwidth = 1, validation: not unreasonable.

In [36]: qd(a.density_df.query('p > .001')[['p', 'F', 'S']], accuracy=4)

p F S

loss

0.0 0.17377 0.17377 0.82623

1.0 0.060821 0.23459 0.76541

2.0 0.13229 0.36688 0.63312

3.0 0.10464 0.47152 0.52848

4.0 0.11704 0.58855 0.41145

5.0 0.093249 0.6818 0.3182

6.0 0.078644 0.76045 0.23955

7.0 0.064101 0.82455 0.17545

8.0 0.049889 0.87444 0.12556

9.0 0.037655 0.91209 0.087908

10.0 0.02737 0.93946 0.060537

11.0 0.019672 0.95913 0.040865

12.0 0.013764 0.9729 0.027101

13.0 0.0094201 0.98232 0.017681

14.0 0.0063168 0.98864 0.011364

15.0 0.0041654 0.9928 0.0071986

16.0 0.0027032 0.9955 0.0044954

17.0 0.0017249 0.99723 0.0027705

18.0 0.0010842 0.99831 0.0016863

2.13.6.6. Poisson-Gamma Distribution, Example 4.5

Aggregate losses have Poisson frequency with mean 2.5 and gamma severity with shape 3 and scale 400. Hence the aggregate mean equals 1,200 and variance equals 480,000.

Now approximate the distribution function using FFT with a fine bucket size and the midpoint method for assigning claim-size probabilities and then bs=20 and bs=100.

Here is Table 4.6, comparing the distributions. The update method re-runs the FFT computation with different options, here altering bs.

In [37]: import numpy as np

In [38]: import pandas as pd

In [39]: a = build('agg Bahn.4.5 2.5 claims '

....: 'sev 400 * gamma 3 poisson')

....:

In [40]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 2.5 0.63246 0.63246

Sev 1200 1200 1.5543e-15 0.57735 0.57735 1.1547 1.1547

Agg 3000 3000 -2.7578e-13 0.7303 0.7303 0.91287 0.91287

log2 = 16, bandwidth = 1/2, validation: not unreasonable.

In [41]: xs = sorted(np.hstack((500, np.arange(0, 10001, 1000))))

In [42]: bit = a.density_df.loc[xs, ['F']]

In [43]: a.update(bs=100)

In [44]: bit100 = a.density_df.loc[xs, ['F']]

In [45]: a.update(bs=20)

In [46]: bit20 = a.density_df.loc[xs, ['F']]

In [47]: bit = pd.concat((bit, bit100, bit20), axis=1, keys=['h0.25', 'h100', 'h20'])

In [48]: bit[('h100', 'Rel Error')] = bit[('h100', 'F')] / bit[('h0.25', 'F')] - 1

In [49]: bit[('h20', 'Rel Error')] = bit[('h20', 'F')] / bit[('h0.25', 'F')] - 1

In [50]: bit = bit.sort_index(axis=1)

In [51]: qd(bit, accuracy=4)

h0.25 h100 h20

F F Rel Error F Rel Error

loss

0.0 0.082085 0.082146 0.00074147 0.082086 6.3895e-06

500.0 0.10958 0.11579 0.056708 0.11076 0.010735

1000.0 0.18677 0.19565 0.047526 0.18849 0.0092186

2000.0 0.37558 0.38525 0.025749 0.37747 0.0050273

3000.0 0.56132 0.56991 0.015294 0.56301 0.003004

4000.0 0.71519 0.72175 0.0091789 0.71648 0.0018127

5000.0 0.82731 0.8318 0.0054318 0.8282 0.0010783

6000.0 0.90135 0.90417 0.0031276 0.90192 0.00062395

7000.0 0.94653 0.94818 0.0017394 0.94686 0.00034868

8000.0 0.97234 0.97324 0.00093101 0.97252 0.0001875

9000.0 0.98627 0.98675 0.00047913 0.98637 9.6942e-05

10000.0 0.99344 0.99367 0.00023728 0.99349 4.8226e-05

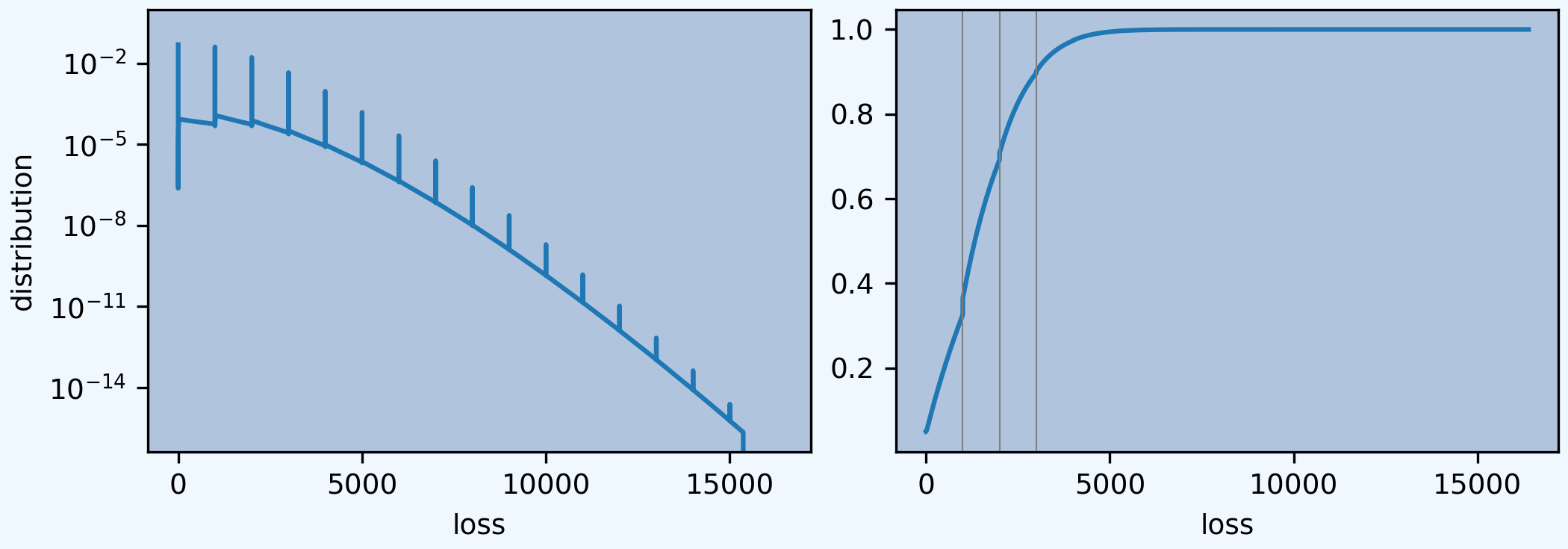

2.13.6.7. Poisson-Lognormal Distribution With Limit, Example 4.15

Consider an aggregate distribution with mean 3 Poisson frequency and lognormal claim size with parameters \((\mu, \sigma) = (6, 1.5)\). Moreover, claim size is limited by a policy limit of 1,000. Graph the aggregate distribution.

The log density (left) shows the probability masses at outcomes consisting of only limit losses. The distribution (right) shows the corresponding jumps. Compare with Figure 4.4.

In [52]: a = build('agg Bahn.4.15 '

....: '3 claims '

....: '1000 xs 0 '

....: 'sev exp(6) * lognorm 1.5 '

....: 'poisson')

....:

In [53]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 3 0.57735 0.57735

Sev 502.97 502.97 1.1478e-09 0.74753 0.74753 0.23542 0.23542

Agg 1508.9 1508.9 1.1478e-09 0.72083 0.72083 0.82314 0.82314

log2 = 16, bandwidth = 1/4, validation: not unreasonable.

In [54]: fig, axs = plt.subplots(1, 2, figsize=(2*3.5, 2.45), constrained_layout=True)

In [55]: ax0, ax1 = axs.flat

In [56]: a.density_df.p.plot(ax=ax0, logy=True, label='FFT');

In [57]: a.density_df.F.plot(ax=ax1, label='FFT');

In [58]: ax0.set(ylabel='log density');

In [59]: ax0.set(ylabel='distribution', ylim=[0,1]);

In [60]: ax1.axvline(1000, c='C7', lw=.5);

In [61]: ax1.axvline(2000, c='C7', lw=.5);

In [62]: ax1.axvline(3000, c='C7', lw=.5);

2.13.6.8. Poisson-Gamma Distribution and Approximations, Problems 4.7 and 13

An aggregate distribution has mean 8 Poisson frequency and gamma severity with shape 0.2 and scale 3750. Compute the distribution and compare with normal and shifted-gamma approximations.

In [63]: a = build('agg Bahn.4.7 '

....: '8 claims '

....: 'sev 3750 * gamma 0.2 '

....: 'poisson')

....:

In [64]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 8 0.35355 0.35355

Sev 750 749.98 -2.9119e-05 2.2361 2.2361 4.4721 4.4721

Agg 6000 5999.8 -2.9119e-05 0.86603 0.86605 1.5877 1.5877

log2 = 16, bandwidth = 2, validation: not unreasonable.

In [65]: xs = np.arange(0, 30000,3000)

In [66]: qd(a.density_df.loc[xs, ['p', 'F','S']], accuracy=4)

p F S

loss

0.0 0.0018002 0.0018002 0.9982

3000.0 0.00020926 0.34209 0.65791

6000.0 0.00014322 0.60704 0.39296

9000.0 8.7227e-05 0.7775 0.2225

12000.0 5.0019e-05 0.87823 0.12177

15000.0 2.7618e-05 0.93494 0.065065

18000.0 1.4853e-05 0.96586 0.034143

21000.0 7.8339e-06 0.98233 0.017666

24000.0 4.0696e-06 0.99096 0.0090364

27000.0 2.0885e-06 0.99542 0.0045787

aggregate readily computes approximations and returns frozen scipy.stats objects.

In [67]: fz = a.approximate('all')

In [68]: comp = pd.DataFrame({k: v.cdf(xs) for k, v in fz.items()}, index=xs)

In [69]: comp['agg'] = a.density_df.loc[xs, 'F',]

In [70]: comp.loc[:, [f'{k} err' for k in fz.keys()]] = comp.loc[:, fz.keys()].values / comp.loc[:, ['agg']].values - 1

In [71]: comp = comp.sort_index(axis=1)

In [72]: qd(comp, accuracy=4)

agg gamma gamma err lognorm lognorm err norm norm err sgamma sgamma err \

0 0.0018002 0 -1 0 -1 0.12411 67.945 0.026306 13.613

3000 0.34209 0.33977 -0.0067746 0.29031 -0.15135 0.28186 -0.17605 0.33624 -0.017089

6000 0.60704 0.61485 0.012868 0.64583 0.063894 0.50001 -0.17631 0.60542 -0.0026701

9000 0.7775 0.78363 0.0078835 0.82019 0.054907 0.71816 -0.07632 0.77824 0.00095764

12000 0.87823 0.88084 0.0029796 0.90331 0.02856 0.8759 -0.0026494 0.87926 0.0011727

15000 0.93494 0.9352 0.00028096 0.94508 0.010852 0.95837 0.025066 0.93559 0.0007034

18000 0.96586 0.96506 -0.00082253 0.96731 0.0015039 0.98954 0.024521 0.96614 0.00028959

21000 0.98233 0.98128 -0.0010704 0.97975 -0.0026265 0.99805 0.016002 0.98239 5.1729e-05

24000 0.99096 0.99002 -0.00095081 0.98703 -0.0039667 0.99973 0.0088504 0.99091 -5.1265e-05

27000 0.99542 0.9947 -0.00072386 0.99145 -0.0039875 0.99997 0.0045731 0.99534 -7.866e-05

slognorm slognorm err

0 0.058626 31.567

3000 0.31389 -0.082441

6000 0.59173 -0.025232

9000 0.77906 0.002005

12000 0.88465 0.0073188

15000 0.94022 0.0056501

18000 0.96881 0.0030552

21000 0.9835 0.001191

24000 0.99113 0.0001684

27000 0.99515 -0.00027715

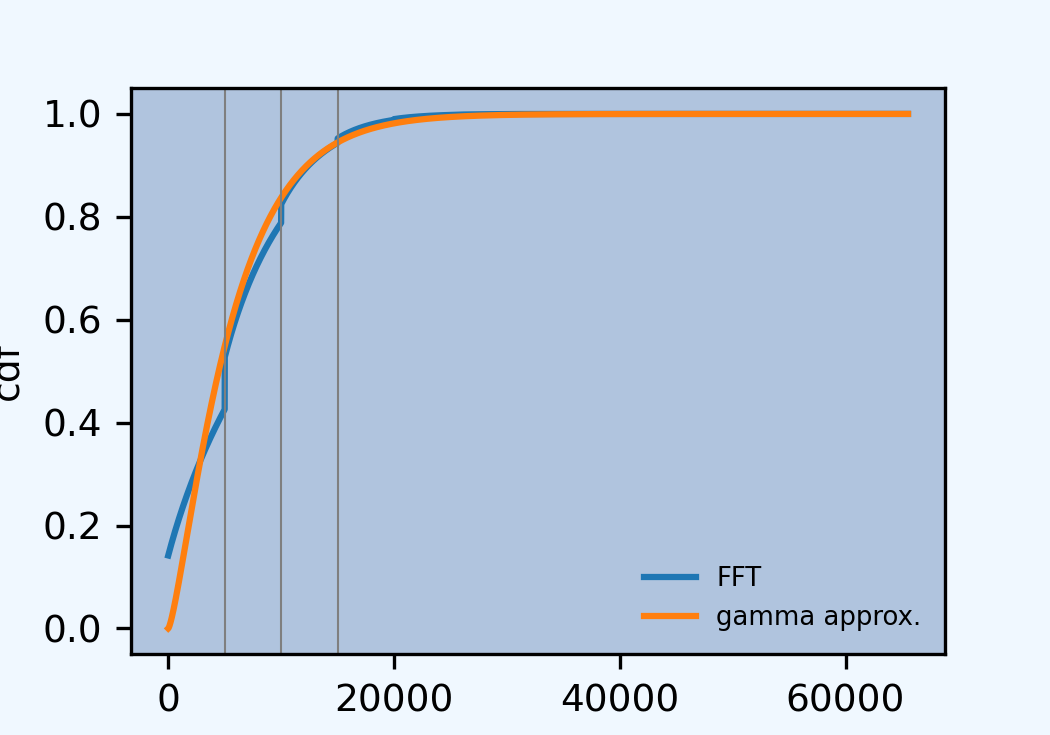

2.13.6.9. Poisson-Lognormal Layer Statistics, Example 5.13

Consider an aggregate distribution with mean 15 Poisson frequency and lognormal claim size with parameters \((\mu, \sigma) = (5.9809, 1.8)\). What are the distribution characteristics for random variable S for claims in the layer 5,000 excess of 3,000?

The exact and FFT-estimated mean, cv, and skewness are reported in the describe dataframe, for frequency and severity. The values reported agree with the text, up to rounding.

In [73]: a = build('agg Bahn.5.13 ' ....: '15 claims 5000 xs 3000 ' ....: 'sev exp(5.9809) * lognorm 1.8 ! ' ....: 'poisson') ....: In [74]: qd(a) E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X) X Freq 15 0.2582 0.2582 Sev 385.68 385.68 -3.4957e-09 3.1319 3.1319 3.1942 3.1942 Agg 5785.3 5785.3 -3.4982e-09 0.84887 0.84887 0.93405 0.93405 log2 = 16, bandwidth = 1, validation: not unreasonable. In [75]: mv(a) mean = 5785.25 variance = 2.411727e+07 std dev = 4910.93

The exact severity can be accessed directly, as a.sevs[0].fz, allowing us to compute the expected layer claim count. The aggregate can then be written in conditional form, producing the same statistics. The distribution function shows probability masses at multiples of the limit.

In [76]: xs = 15 * a.sevs[0].fz.sf(3000) In [77]: print(f'excess claim count = {xs:.5f}') excess claim count = 1.95359 In [78]: a = build('agg Bahn.5.13b ' ....: f'{xs} claims 5000 xs 3000 ' ....: 'sev exp(5.9809) * lognorm 1.8 ' ....: 'poisson') ....: In [79]: qd(a) E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X) X Freq 1.9536 0.71546 0.71546 Sev 2961.3 2961.3 -3.4956e-09 0.63853 0.63853 -0.16374 -0.16374 Agg 5785.3 5785.3 -3.4982e-09 0.84887 0.84887 0.93405 0.93405 log2 = 16, bandwidth = 1, validation: not unreasonable. In [80]: fig, ax = plt.subplots(1,1,figsize=(3.5, 2.45)) In [81]: a.density_df.F.plot(ax=ax, label='FFT'); In [82]: fz = a.approximate('gamma') In [83]: ax.plot(a.density_df.loss, fz.cdf(a.density_df.loss), c='C1', label='gamma approx.'); In [84]: ax.axvline(5000, c='C7', lw=.5); In [85]: ax.axvline(10000, c='C7', lw=.5); In [86]: ax.axvline(15000, c='C7', lw=.5); In [87]: ax.set(ylabel='cdf'); In [88]: ax.legend(loc='lower right');

2.13.6.10. Lognormal Increased Limits Factors (ILFs), Example 6.3

Indemnity losses for a portfolio of insurance policies have a lognormal claim-size distribution with parameters \((\mu, \sigma) = (7, 2.4)\). The policy per-claim limit applies only to the indemnity portion of a claim, and the average per-claim loss adjustment expense is 2,200. Claim frequency for these policies is 0.0005 per exposure unit, and variable expenses equal 35% of premium.

A lognormal with \(\sigma = 2.4\) has cv \(\sqrt{\exp(2.4^2)-1}=17.78\) and is extremely thick-tailed, despite having moments of all orders. It is challenging to approximate numerically. Luckily, we only need to compute up to 5M. The aggregate parameters deliberately select a range that is too narrow for the entire distribution, but adequate for our purposes. Use log2=17 and select bs greater than 5e6 // 2**17 = 38. We use bs=50.

It is important to set normalize=False to avoid rescaling bucket probabilities to sum to one. These parameters are not a good model for the entire distribution; the mean error is too high.

The density_df dataframe includes limited expected values. Here is a sample.

In [89]: a = build('agg Bahn.6.3 '

....: '1 claim '

....: 'sev exp(7) * lognorm 2.4 '

....: 'fixed',

....: bs=50, log2=17,

....: normalize=False,

....: )

....:

In [90]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1 0

Sev 19536 18328 -0.061835 17.786 7.7935 5680 27.885

Agg 19536 18328 -0.061835 17.786 7.7935 5680 27.885

log2 = 17, bandwidth = 50, validation: fails sev mean, agg mean.

In [91]: xs = [1e5, 5e5, 7.5e5, 1e6, 2e6, 3e6, 4e6, 5e6]

In [92]: qd(a.density_df.loc[xs, ['F', 'S', 'lev']], accuracy=4)

F S lev

loss

100000.0 0.96998 0.030021 8895.8

500000.0 0.99463 0.0053706 13625

750000.0 0.99674 0.0032647 14668

1000000.0 0.99774 0.002257 15345

2000000.0 0.99912 0.00087817 16738

3000000.0 0.99951 0.00048765 17390

4000000.0 0.99968 0.00031609 17782

5000000.0 0.99978 0.00022372 18048

The following reproduces Table 6.1. The ILF factors assume fixed (middle) and variable ALAE (right).

In [93]: alae = 2200

In [94]: bit = a.density_df.loc[xs, ['lev']]

In [95]: bit['Fixed ALAE'] = (bit.lev + alae) / (bit.lev.iloc[0] + alae)

In [96]: bit['Prop ALAE'] = bit.lev / bit.lev.iloc[0]

In [97]: qd(bit, accuracy=4)

lev Fixed ALAE Prop ALAE

loss

100000.0 8895.8 1 1

500000.0 13625 1.4262 1.5317

750000.0 14668 1.5202 1.6488

1000000.0 15345 1.5812 1.725

2000000.0 16738 1.7067 1.8815

3000000.0 17390 1.7655 1.9549

4000000.0 17782 1.8009 1.9989

5000000.0 18048 1.8248 2.0288

2.13.6.12. Risk Loads, Example 6.5

Example 6.5, computes risk loads as a percentage of standard deviation. aggregate can compute multiple limits at once, and the report_df dataframe returns individual severity and aggregate distribution statistics. The risk loads can be deduced from these. The risk load can be computed as k' * ex2 or k * agg_cv (not shown).

The following code reproduces Table 6.3. First, define the controlling variables, and then set up the tower of limits within one object, using Vectorization: Limit Profiles and Mixed Severity.

In [104]: k_prime = 0.0277

In [105]: m = 400

In [106]: ϕ = 0.0005

In [107]: u = 0.2

In [108]: k = k_prime / np.sqrt(m * ϕ)

In [109]: limits = [1e5, 5e5, 1e6, 2e6, 3e6, 4e6, 5e6]

In [110]: bl = build('agg Bahn.6.5 '

.....: f'{m * ϕ} claims '

.....: f'{limits} xs 0 '

.....: 'sev exp(7) * lognorm 2.4 '

.....: 'poisson'

.....: , bs=50, log2=18)

.....:

In [111]: qd(bl.report_df.iloc[:, :-4], accuracy=4)

view 0 1 2 3 4 5 6

statistic

name Bahn.6.5 Bahn.6.5 Bahn.6.5 Bahn.6.5 Bahn.6.5 Bahn.6.5 Bahn.6.5

limit 1e+05 5e+05 1e+06 2e+06 3e+06 4e+06 5e+06

attachment 0 0 0 0 0 0 0

el 1779.2 2725.1 3069 3347.6 3478 3556.5 3609.6

freq_m 0.2 0.2 0.2 0.2 0.2 0.2 0.2

freq_cv 2.2361 2.2361 2.2361 2.2361 2.2361 2.2361 2.2361

freq_skew 2.2361 2.2361 2.2361 2.2361 2.2361 2.2361 2.2361

sev_m 8896 13626 15345 16738 17390 17782 18048

sev_cv 2.3401 3.7719 4.63 5.6565 6.3357 6.851 7.2685

sev_skew 3.3416 7.0585 9.9524 14.303 17.849 20.975 23.827

agg_m 1779.2 2725.1 3069 3347.6 3478 3556.5 3609.6

agg_cv 5.6903 8.7257 10.592 12.844 14.342 15.482 16.406

agg_skew 8.1747 15.898 22.157 31.683 39.494 46.396 52.704

Next, extract the required columns from report_df and manipulate to compute the ILFs.

In [112]: bit = bl.report_df.loc[['sev_m', 'sev_cv', 'agg_m', 'agg_cv']].iloc[:, :-4].T

In [113]: bit.index = limits

In [114]: bit.index.name = 'limit'

In [115]: bit['vx'] = (bit.sev_m * bit.sev_cv) ** 2

In [116]: bit['ex2'] = bit.vx + bit.sev_m**2

In [117]: bit['risk load'] = k_prime * bit.ex2 ** 0.5

In [118]: bit['lev'] = (1+u) * bit.sev_m

In [119]: bit['ILF w/o risk'] = bit['lev'] / bit.loc[100000, 'lev']

In [120]: bit['ILF with risk'] = (bit['lev'] + bit['risk load']) / (bit.loc[100000, 'lev'] + bit.loc[100000, 'risk load'])

In [121]: qd(bit, accuracy=4)

statistic sev_m sev_cv agg_m agg_cv vx ex2 risk load lev ILF w/o risk \

limit

100000.0 8896 2.3401 1779.2 5.6903 4.3337e+08 5.1251e+08 627.09 10675 1

500000.0 13626 3.7719 2725.1 8.7257 2.6414e+09 2.8271e+09 1472.8 16351 1.5316

1000000.0 15345 4.63 3069 10.592 5.0478e+09 5.2833e+09 2013.4 18414 1.7249

2000000.0 16738 5.6565 3347.6 12.844 8.964e+09 9.2441e+09 2663.3 20085 1.8815

3000000.0 17390 6.3357 3478 14.342 1.2139e+10 1.2442e+10 3089.7 20868 1.9548

4000000.0 17782 6.851 3556.5 15.482 1.4842e+10 1.5158e+10 3410.4 21339 1.9989

5000000.0 18048 7.2685 3609.6 16.406 1.7208e+10 1.7534e+10 3667.9 21658 2.0288

statistic ILF with risk

limit

100000.0 1

500000.0 1.577

1000000.0 1.8074

2000000.0 2.0127

3000000.0 2.1197

4000000.0 2.1897

5000000.0 2.2407

2.13.6.14. Deductible Credits, Example 6.7

(Continues Example 6.3.) Consider a portfolio of policies for which the ground-up indemnity claim size has a lognormal distribution with parameters \((\mu, \sigma) = (7.0, 2.4)\) and allocated loss adjustment expense is 20% of the indemnity amount. The basic limit is 100,000. Calculate the credit factors, as well as the resulting frequency and severity, for six straight deductible options: 1,000; 2,000; 3,000; 4,000; 5,000; and 10,000. Base frequency equals 0.0005.

We can build all of the required distributions simultaneously using vectorization. Remember that the basic limit is ground up. The severity is unconditional, indicated by ! at the end of the severity clause. The limit is eroded by the deductible.

In [138]: deductibles = [0, 1e3, 2e3, 3e3, 4e3, 5e3, 10e3]

In [139]: limits = [100000 - i for i in deductibles]

In [140]: ϕ = 0.0005

In [141]: alae = 1.2

In [142]: bl = build('agg Bahn.6.7 '

.....: f'{ϕ} claims '

.....: f'{limits} xs {deductibles} '

.....: 'sev exp(7) * lognorm 2.4 ! '

.....: 'poisson'

.....: , bs=50, log2=18)

.....:

In [143]: qd(bl.report_df.iloc[:, :-4], accuracy=4)

view 0 1 2 3 4 5 6

statistic

name Bahn.6.7 Bahn.6.7 Bahn.6.7 Bahn.6.7 Bahn.6.7 Bahn.6.7 Bahn.6.7

limit 1e+05 99000 98000 97000 96000 95000 90000

attachment 0 1000 2000 3000 4000 5000 10000

el 4.448 4.1183 3.8926 3.7092 3.5517 3.4124 2.8758

freq_m 0.0005 0.0005 0.0005 0.0005 0.0005 0.0005 0.0005

freq_cv 44.721 44.721 44.721 44.721 44.721 44.721 44.721

freq_skew 44.721 44.721 44.721 44.721 44.721 44.721 44.721

sev_m 8896 8236.6 7785.2 7418.4 7103.4 6824.9 5751.7

sev_cv 2.3401 2.5106 2.6287 2.7269 2.813 2.8907 3.2067

sev_skew 3.3416 3.3681 3.4054 3.4444 3.4833 3.5215 3.6997

agg_m 4.448 4.1183 3.8926 3.7092 3.5517 3.4124 2.8758

agg_cv 113.81 120.85 125.78 129.89 133.51 136.79 150.22

agg_skew 163.49 165.89 168.03 170.02 171.89 173.66 181.54

Next, manipulate the report_df dataframe to compute the required quantities. The final exhibit replicates Table 6.5.

In [144]: bit = bl.report_df.iloc[:, :-4].loc[['attachment', 'freq_m', 'sev_m', 'agg_m']].T

In [145]: bit = bit.rename(columns={'attachment': 'deductible'}).set_index('deductible')

In [146]: bit['F(d)'] = np.array([bl.sevs[0].fz.cdf(i) for i in bit.index])

In [147]: bit['freq_m'] = bit.loc[0, 'freq_m'] * (1 - bit['F(d)'])

In [148]: bit['E[X;d]'] = (bit.sev_m[0] - bit.sev_m)

In [149]: bit['C(d)'] = bit['E[X;d]'] / bit.sev_m[0]

In [150]: bit['sev_m'] = bit['sev_m'] / (1 - bit['F(d)']) * alae

In [151]: bit = bit.iloc[:, [-2, 3, -1, 0, 1]]

In [152]: bit['pure prem'] = bit.freq_m * bit.sev_m

In [153]: qd(bit, accuracy=4)

statistic E[X;d] F(d) C(d) freq_m sev_m pure prem

deductible

0.0 0 0 0 0.0005 10675 5.3376

1000.0 659.42 0.48467 0.074125 0.00025766 19180 4.942

2000.0 1110.8 0.59885 0.12487 0.00020057 23289 4.6711

3000.0 1477.7 0.66251 0.16611 0.00016875 26377 4.451

4000.0 1792.7 0.70512 0.20151 0.00014744 28907 4.262

5000.0 2071.2 0.73636 0.23282 0.00013182 31064 4.0949

10000.0 3144.4 0.82147 0.35346 8.9266e-05 38660 3.451

2.13.6.15. Summary

Here is a summary of all the objects created in this section.

In [154]: from aggregate import pprint_ex

In [155]: for n, r in build.qlist('^Bahn').iterrows():

.....: pprint_ex(r.program, split=20)

.....: