2.4.11. The tweedie Keyword

Prerequisites: Tweedie distribution from GLMs. Use of build.

See also: The Tweedie Distribution.

The aggregate language keyword tweedie makes it easy to build Tweedie distributions.

It uses reproductive

parameters \(\mu, p, \sigma^2\) (mean, power, and dispersion), since these are most natural for GLM modeling.

Example.

The keyword is used as follows to produce \(\mathsf{Tw}_{1.05}(2, 5)\), mean 2, \(p=1.05\), and dispersion 5.

In [1]: from aggregate import build, qd, mv

In [2]: a15 = build('agg DecL:15 tweedie 2 1.05 5')

In [3]: qd(a15)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.40671 1.568 1.568

Sev 4.9175 4.9175 -2.3315e-15 0.22942 0.22942 0.45883 0.45883

Agg 2 2 -2.2204e-15 1.6088 1.6088 1.6892 1.6892

log2 = 16, bandwidth = 1/512, validation: not unreasonable.

In [4]: mv(a15)

mean = 2

variance = 10.35265

std dev = 3.21755

In [5]: print(f'Expected variance = disp x mean ** p = {2**1.05 * 5:.5f}')

Expected variance = disp x mean ** p = 10.35265

Inspecting the (non-trivial parts of the) specification shows the parser converts it into the additive form:

In [6]: {k: v for k,v in a15.spec.items()

...: if v!=0 and v is not None and v!=''}

...:

Out[6]:

{'name': 'DecL:15',

'exp_en': 0.4067100332315139,

'exp_limit': inf,

'sev_name': 'gamma',

'sev_a': 18.999999999999982,

'sev_scale': 0.2588162309603446,

'sev_wt': 1,

'sev_ub': inf,

'sev_conditional': True,

'freq_name': 'poisson',

'freq_p0': nan,

'note': 'Tw(p=1.05, μ=2.0, σ^2=5.0) --> CP(λ= 0.40671, ga(α=19, β=0.25881623), scale=0.25881623'}

The note shows the compound Poisson specification.

The helper function tweedie_convert translates between parameterizations. The scale (dispersion) parameter \(\sigma^2\) has offsetting effects: higher \(\sigma^2\) results in a lower claim count, a higher gamma mean, and a more skewed aggregate distribution with a bigger mass at zero.

Example.

The code below shows the three Tweedie representations, starting with the easiest to interpret.

In [7]: from aggregate import tweedie_convert

In [8]: import pandas as pd

In [9]: p = 1.005; μ = 1; σ2 = 0.1; \

...: m0 = tweedie_convert(p=p, μ=μ, σ2=σ2); \

...: λ = μ**(2-p) / ((2-p) * σ2); \

...: α = (2 - p) / (p - 1); \

...: β = μ / (λ * α); \

...: tw_cv = σ2**.5 * μ**(p/2-1); \

...: sev_m = α * β; \

...: sev_cv = α**-0.5; \

...: m1 = tweedie_convert(λ=λ, m=sev_m, cv=sev_cv); \

...: m2 = tweedie_convert(λ=λ, α=α, β=β);

...:

In [10]: assert np.allclose(m0, m1, m2)

In [11]: temp = pd.concat((m0, m1, m2), axis=1); \

....: temp.columns = ['mean p disp', 'lambda sev m cv', 'lambda shape scale'];

....:

In [12]: with pd.option_context('display.float_format', lambda x: f'{x:.12g}'):

....: print(temp)

....:

mean p disp lambda sev m cv lambda shape scale

μ 1 1 1

p 1.005 1.005 1.005

σ^2 0.1 0.1 0.1

λ 10.0502512563 10.0502512563 10.0502512563

α 199 199 199

β 0.0005 0.0005 0.0005

tw_cv 0.316227766017 0.316227766017 0.316227766017

sev_m 0.0995 0.0995 0.0995

sev_cv 0.0708881205008 0.0708881205008 0.0708881205008

p0 4.31748997327e-05 4.31748997327e-05 4.31748997327e-05

Three different ways of specifying the same Tweedie distribution.

In [13]: program = f'''

....: agg DecL:16 {λ} claims sev gamma {sev_m:.8g} cv {sev_cv} poisson

....: agg DecL:17 {λ} claims sev {β:.4g} * gamma {α:.4g} poisson

....: agg DecL:18 tweedie {μ} {p} {σ2}

....: '''

....:

In [14]: tweedies = build(program)

In [15]: for a in tweedies:

....: print(a.program)

....: qd(a.object.describe)

....: print()

....:

agg DecL:16 10.050251256281404 claims sev gamma 0.0995 cv 0.07088812050083283 poisson

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Err CV(X) Skew(X) Est Skew(X)

X

Freq 10.05 NaN NaN 0.31544 NaN NaN 0.31544 NaN

Sev 0.0995 0.0995 -8.2379e-14 0.070888 0.070888 3.12e-06 0.14178 0.14177

Agg 1 1 -1.1036e-13 0.31623 0.31623 1.5599e-08 0.31781 0.31781

agg DecL:17 10.050251256281404 claims sev 0.0005 * gamma 199 poisson

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Err CV(X) Skew(X) Est Skew(X)

X

Freq 10.05 NaN NaN 0.31544 NaN NaN 0.31544 NaN

Sev 0.0995 0.0995 -1.0825e-13 0.070888 0.070888 3.12e-06 0.14178 0.14177

Agg 1 1 -1.3756e-13 0.31623 0.31623 1.5599e-08 0.31781 0.31781

agg DecL:18 tweedie 1 1.005 0.1

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Err CV(X) Skew(X) Est Skew(X)

X

Freq 10.05 NaN NaN 0.31544 NaN NaN 0.31544 NaN

Sev 0.0995 0.0995 -8.6597e-14 0.070888 0.070888 3.12e-06 0.14178 0.14177

Agg 1 1 -1.148e-13 0.31623 0.31623 1.5599e-08 0.31781 0.31781

Convert from reproductive form:

In [16]: tweedie_convert(p=1.05, μ=2, σ2=5)

Out[16]:

μ 2.000000

p 1.050000

σ^2 5.000000

λ 0.406710

α 19.000000

β 0.258816

tw_cv 1.608777

sev_m 4.917508

sev_cv 0.229416

p0 0.665837

dtype: float64

Convert from additive form:

In [17]: tweedie_convert(λ=0.406710033, m=4.917508388, cv=0.229415734)

Out[17]:

μ 2.000000

p 1.050000

σ^2 5.000000

λ 0.406710

α 19.000000

β 0.258816

tw_cv 1.608777

sev_m 4.917508

sev_cv 0.229416

p0 0.665837

dtype: float64

Build a Tweedie using reproductive parameters, p, mu, sigma2.

In [18]: a19 = build('agg DecL:19 tweedie 2 1.05 5')

In [19]: a19.plot()

In [20]: qd(a19)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 0.40671 1.568 1.568

Sev 4.9175 4.9175 -2.3315e-15 0.22942 0.22942 0.45883 0.45883

Agg 2 2 -2.2204e-15 1.6088 1.6088 1.6892 1.6892

log2 = 16, bandwidth = 1/512, validation: not unreasonable.

In [21]: print(a19.spec)

{'name': 'DecL:19', 'exp_el': 0, 'exp_premium': 0, 'exp_lr': 0, 'exp_en': 0.4067100332315139, 'exp_attachment': None, 'exp_limit': inf, 'sev_name': 'gamma', 'sev_a': 18.999999999999982, 'sev_b': 0, 'sev_mean': 0, 'sev_cv': 0, 'sev_loc': 0, 'sev_scale': 0.2588162309603446, 'sev_xs': None, 'sev_ps': None, 'sev_wt': 1, 'sev_lb': 0, 'sev_ub': inf, 'sev_conditional': True, 'sev_pick_attachments': None, 'sev_pick_losses': None, 'occ_reins': None, 'occ_kind': '', 'freq_name': 'poisson', 'freq_a': 0, 'freq_b': 0, 'freq_zm': False, 'freq_p0': nan, 'agg_reins': None, 'agg_kind': '', 'note': 'Tw(p=1.05, μ=2.0, σ^2=5.0) --> CP(λ= 0.40671, ga(α=19, β=0.25881623), scale=0.25881623'}

In [22]: print(a19.cdf(0), np.exp(-.40671))

0.6658372329829731 0.6658372551097528

Example.

When p is close to 1, the Tweedie approaches a Poisson. Here mean = 10 and sigma2 = 1, so the distribution is not over-dispersed. The gamma severity has mean 1 and a very small CV; it acts like degenerate distribution at 1.

In [23]: a20 = build('agg DecL:20 tweedie 10 1.0001 1')

In [24]: a20.plot()

In [25]: qd(a20)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 9.9987 0.31625 0.31625

Sev 1.0001 1.0001 1.9973e-11 0.010001 0.010004 0.019989 0.019977

Agg 10 10 1.997e-11 0.31626 0.31626 0.3163 0.3163

log2 = 16, bandwidth = 1/1024, validation: not unreasonable.

In [26]: tweedie_convert(p=1.0001, μ=10, σ2=1)

Out[26]:

μ 10.000000

p 1.000100

σ^2 1.000000

λ 9.998698

α 9999.000000

β 0.000100

tw_cv 0.316264

sev_m 1.000130

sev_cv 0.010001

p0 0.000045

dtype: float64

Example.

When p is close to 2, the Tweedie approaches a Gamma. Here mean = 10, and sigma2=0.04.

The variance equals sigma2 mu^2, so CV = sigma = 0.2

In [27]: a21 = build('agg DecL:21 tweedie 10 1.999 0.04', log2=16, bs=1/256)

In [28]: a21.plot()

In [29]: qd(a21)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 25058 0.0063173 0.0063173

Sev 0.00039908 0.00039773 -0.0033706 31.607 31.715 63.214 63.21

Agg 10 9.9663 -0.0033706 0.19977 0.20045 0.39934 0.39932

log2 = 16, bandwidth = 1/256, validation: fails sev mean, agg mean.

Build the same distribution explicitly from gamma severities. Here the gamma is built using mean and CV or shape and scale.

In [30]: tc = tweedie_convert(p=1.9999, μ=10, σ2=.04)

In [31]: print(tc)

μ 10.000000

p 1.999900

σ^2 0.040000

λ 250057.571255

α 0.000100

β 0.399868

tw_cv 0.199977

sev_m 0.000040

sev_cv 99.995000

p0 0.000000

dtype: float64

In [32]: m, cv = tc['μ'], tc['tw_cv']

In [33]: print(m, cv)

10.0 0.19997697547449372

In [34]: g = build(f'sev g gamma {m} cv {cv}')

In [35]: sh = cv ** -2; sc = m / sh

In [36]: print(sc, sh)

0.39990790719926267 25.005757125520617

In [37]: g2 = build(f'sev g2 {sc} * gamma {sh}')

In [38]: print(g2.stats(), g.stats())

(9.999999999999968, 3.999079071994487) (10.000000000000108, 3.999079071991673)

2.4.11.1. Analytic Error Analysis

There is a series expansion for the pdf of a Tweedie computed by conditioning on the number of claims and using that a convolution of gammas with the same scale parameter is again gamma. For a Tweedie with expected frequency \(\lambda\), gamma shape \(\alpha\) and scale \(\beta\), it is given by

for \(x>0\) and \(f(x)=\exp(-\lambda)\). The exact function shows the FFT method is very accurate.

In [39]: from aggregate import tweedie_convert, build, qd

In [40]: from scipy.special import loggamma

In [41]: import matplotlib.pyplot as plt

In [42]: import numpy as np

In [43]: from pandas import option_context

In [44]: a = build('agg Tw tweedie 10 1.01 1')

In [45]: qd(a)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 9.8711 0.31829 0.31829

Sev 1.0131 1.0131 -1.9318e-14 0.1005 0.1005 0.20101 0.20101

Agg 10 10 -2.2427e-14 0.31989 0.31989 0.32309 0.32309

log2 = 16, bandwidth = 1/1024, validation: not unreasonable.

In [46]: a.plot()

A Tweedie with \(p\) close to 1 approximates a Poisson. Its gamma severity is very peaked around its mean (high \(\alpha\) and offsetting small \(\beta\)).

The next function provides a transparent, if inefficient, implementation of the Tweedie density.

In [47]: def tweedie_density(x, mean, p, disp):

....: pars = tweedie_convert(p=p, μ=mean, σ2=disp)

....: λ = pars['λ']

....: α = pars['α']

....: β = pars['β']

....: if x == 0:

....: return np.exp(-λ)

....: logl = np.log(λ)

....: logx = np.log(x)

....: logb = np.log(β)

....: logbase = -λ

....: log_term = 100

....: const = -λ - x / β

....: ans = 0.0

....: for n in range(1, 2000): #while log_term > -20:

....: log_term = (const +

....: + n * logl +

....: + (n * α - 1) * logx +

....: - loggamma(n+1) +

....: - loggamma(n * α) +

....: - n * α * logb)

....: ans += np.exp(log_term)

....: if n > 20 and log_term < -227:

....: break

....: return ans

....:

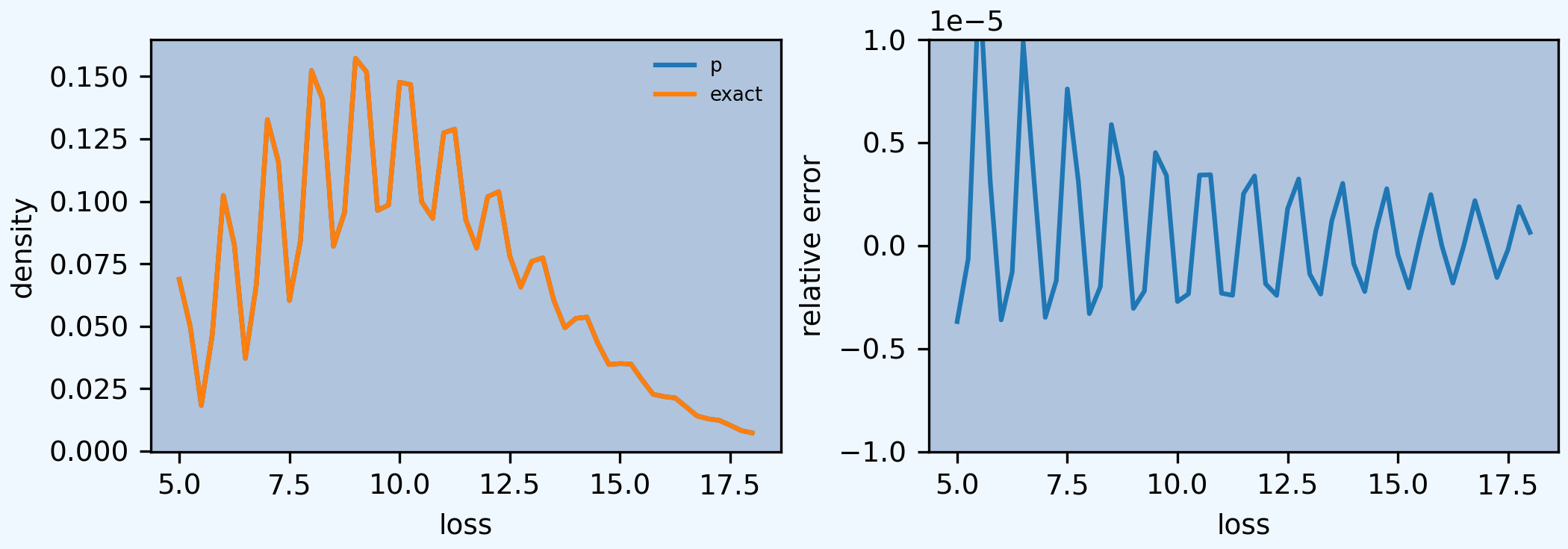

The following graphs show that the FFT approximation is excellent, across a wide range, just as its good moment-matching performance suggests it would be.

In [48]: bit = a.density_df.loc[5:a.q(0.99):256, ['p']]

In [49]: bit['exact'] = [tweedie_density(i, 10, 1.01, 1) for i in bit.index]

In [50]: bit['p'] /= a.bs

In [51]: fig, axs = plt.subplots(1, 2, figsize=(2 * 3.5, 2.45), constrained_layout=True, squeeze=True)

In [52]: ax0, ax1 = axs.flat

In [53]: bit.plot(ax=ax0);

In [54]: ax0.set(ylabel='density');

In [55]: bit['err'] = bit.p / bit.exact - 1

In [56]: bit.err.plot(ax=ax1);

In [57]: ax1.set(ylabel='relative error', ylim=[-1e-5, 1e-5]);