2.4.6. Mixed Severity Distributions

Prerequisites: Examples use build and qd, and basic Aggregate output.

The variables in the severity clause (scale, location, distribution ID, shape parameters, mean and CV) can be vectors to create a mixed severity distribution. All elements are broadcast against one-another.

Example:

sev lognorm 1000 cv [0.75 1.0 1.25 1.5 2] wts [0.4, 0.2, 0.1, 0.1, 0.1]

expresses a mixture of five lognormals, each with a mean of 1000 and CVs equal to 0.75, 1.0, 1.25, 1.5, and 2, and with weights 0.4, 0.2, 0.1, 0.1, 0.1. Equal weights are expressed

as wts=5, or the relevant number of components (note equals sign). A missing weights clause is

interpreted as giving each severity weight 1 which results in five times the

total loss. Commas in the lists are optional.

Warning

Weights are applied to exposure, and their meaning depends on how exposure is entered.

If exposure is given by claim count, then the weights apply to claim count. This gives the usual mixture of severity curves. However, if exposure is entered as loss or premium times a loss ratio, then the weights give the proportion of expected loss, not the claim count. Make sure the weights are appropriate to the way exposure is expressed. For example, if the mixture is used to split small and large claims, then an 80/20 split small/large claim counts may well correspond to a 20/80 split of expected losses (Pareto rule of thumb).

Example.

This example illustrates the different behaviors of wts.

The weights adjust claim counts for each mixture component when exposures are given by claims.

In [1]: from aggregate import build, qd

In [2]: a01 = build('agg DecL:01 '

...: '100 claims '

...: '5000 xs 0 '

...: 'sev lognorm [10 20 50 75 100] '

...: 'cv [0.75 1.0 1.25 1.5 2] '

...: 'wts [0.4, 0.25, 0.15, 0.1, 0.1] '

...: 'poisson'

...: , bs=1/2, approximation='exact')

...:

In [3]: qd(a01)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 100 0.1 0.1

Sev 33.978 33.978 2.5414e-09 2.3807 2.3807 15.161 15.161

Agg 3397.8 3397.8 2.5414e-09 0.25822 0.25822 1.2927 1.2927

log2 = 16, bandwidth = 1/2, validation: not unreasonable.

Mixed severity with Poisson frequency is the same as the sum of five independent components. The report_df shows the mixture details.

In [4]: qd(a01.report_df.iloc[:, :-3])

view 0 1 2 3 4 independent

statistic

name DecL:01 DecL:01 DecL:01 DecL:01 DecL:01 DecL:01

limit 5000 5000 5000 5000 5000 5000

attachment 0 0 0 0 0 0

el 400 500 750 749.93 997.86 3397.8

freq_m 40 25 15 10 10 100

freq_cv 0.15811 0.2 0.2582 0.31623 0.31623 0.1

freq_skew 0.15811 0.2 0.2582 0.31623 0.31623 0.1

sev_m 10 20 50 74.993 99.786 33.978

sev_cv 0.75 1 1.2498 1.4942 1.9175 2.3807

sev_skew 2.6719 4 5.6619 7.1636 8.3826 15.161

agg_m 400 500 750 749.93 997.86 3397.8

agg_cv 0.19764 0.28284 0.41329 0.56857 0.68386 0.25822

agg_skew 0.30882 0.56568 1.054 1.7191 2.224 1.2927

This aggregate can also be built as a Portfolio.

In [5]: a02 = build(

...: 'port DecL:02 '

...: 'agg Unit1 40 loss 5000 xs 0 sev lognorm 10 cv 0.75 poisson '

...: 'agg Unit2 25 loss 5000 xs 0 sev lognorm 20 cv 1.00 poisson '

...: 'agg Unit3 15 loss 5000 xs 0 sev lognorm 50 cv 1.25 poisson '

...: 'agg Unit4 10 loss 5000 xs 0 sev lognorm 75 cv 1.50 poisson '

...: 'agg Unit5 10 loss 5000 xs 0 sev lognorm 100 cv 2.00 poisson '

...: , bs=1/2, approximation='exact')

...:

In [6]: qd(a02)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

unit X

Unit1 Freq 4 0.5 0.5

Sev 10 10 8.9604e-09 0.75 0.75014 2.6719 2.6704

Agg 40 40 8.9606e-09 0.625 0.62504 0.97656 0.97653

Unit2 Freq 1.25 0.89443 0.89443

Sev 20 20 -9.7705e-09 1 1 4 3.9997

Agg 25 25 -9.7705e-09 1.2649 1.2649 2.5298 2.5298

Unit3 Freq 0.3 1.8257 1.8257

Sev 50 50 -1.0074e-09 1.2498 1.2498 5.6619 5.6618

Agg 15 15 -1.0074e-09 2.9224 2.9224 7.4526 7.4526

Unit4 Freq 0.13335 2.7385 2.7385

Sev 74.993 74.993 -4.0382e-10 1.4942 1.4942 7.1636 7.1635

Agg 10 10 -4.0383e-10 4.9237 4.9237 14.887 14.887

Unit5 Freq 0.10021 3.1589 3.1589

Sev 99.786 99.786 1.1018e-08 1.9175 1.9175 8.3826 8.3826

Agg 10 10 1.1019e-08 6.8313 6.8313 22.216 22.216

total Freq 5.7836 0.41582 0.41582

Sev 17.29 17.29 2.0519e-09 2.2699 26

Agg 100 100 2.031e-09 1.0314 1.0314 8.7339 8.7338

log2 = 16, bandwidth = 1/2, validation: not unreasonable.

Actual frequency equals total frequency times weight. Setting wts=5 results in equal weights, here 0.2.

In [7]: a03 = build('agg DecL:03 '

...: '100 claims '

...: '5000 xs 0 '

...: 'sev lognorm [10 20 50 75 100] '

...: 'cv [0.75 1.0 1.25 1.5 2] '

...: ' wts=5 '

...: 'poisson'

...: , bs=1/2, approximation='exact')

...:

In [8]: qd(a03)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 100 0.1 0.1

Sev 50.956 50.956 3.5836e-09 2.1341 2.1341 11.891 11.891

Agg 5095.6 5095.6 3.5835e-09 0.23568 0.23568 0.99494 0.99494

log2 = 16, bandwidth = 1/2, validation: not unreasonable.

Missing weights are set to 1, resulting in five times loss. This behavior is generally not what you want!

In [9]: a04 = build('agg DecL:04 '

...: '100 claims '

...: '5000 xs 0 '

...: 'sev lognorm [10 20 50 75 100] '

...: 'cv [0.75 1.0 1.25 1.5 2] '

...: 'poisson'

...: , bs=1, approximation='exact')

...:

In [10]: qd(a04)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 500 0.044721 0.044721

Sev 50.956 50.956 -2.2323e-08 2.1341 2.1341 11.891 11.891

Agg 25478 25478 -2.2323e-08 0.1054 0.1054 0.44495 0.44495

log2 = 16, bandwidth = 1, validation: not unreasonable.

If exposures are determined via losses (directly or using premium and loss ratio or exposure and rate), then the weights apply to expected loss. The resulting mixture is quite different.

In [11]: a01e = build('agg DecL:01e '

....: f'{a01.agg_m} loss '

....: '5000 xs 0 '

....: 'sev lognorm [10 20 50 60 70] '

....: 'cv [0.75 1.0 1.25 1.5 2] '

....: 'wts [0.4, 0.25, 0.15, 0.1, 0.1] '

....: 'poisson'

....: , bs=1/2, approximation='exact')

....:

In [12]: qd(a01e)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 115.2 0.093168 0.093168

Sev 29.493 29.493 1.1694e-08 2.1101 2.1101 14.661 14.661

Agg 3397.8 3397.8 1.1694e-08 0.21755 0.21755 1.113 1.113

log2 = 16, bandwidth = 1/2, validation: not unreasonable.

In [13]: qd(a01e.report_df.iloc[:, :-3])

view 0 1 2 3 4 independent

statistic

name DecL:01e DecL:01e DecL:01e DecL:01e DecL:01e DecL:01e

limit 5000 5000 5000 5000 5000 5000

attachment 0 0 0 0 0 0

el 460.82 576.02 864.03 691.2 805.71 3397.8

freq_m 46.082 28.801 17.281 11.52 11.52 115.2

freq_cv 0.14731 0.18634 0.24056 0.29462 0.29462 0.093168

freq_skew 0.14731 0.18634 0.24056 0.29462 0.29462 0.093168

sev_m 10 20 50 59.997 69.938 29.493

sev_cv 0.75 1 1.2498 1.4968 1.9523 2.1101

sev_skew 2.6719 4 5.6619 7.3823 9.6027 14.661

agg_m 460.82 576.02 864.03 691.2 805.71 3397.8

agg_cv 0.18414 0.26352 0.38505 0.53034 0.64624 0.21755

agg_skew 0.28772 0.52703 0.98195 1.6404 2.3418 1.113

2.4.6.1. Mixed Exponential Distributions

The mixed exponential distribution (MED) is used by major US rating

bureaus to model severity and compute increased limits factors (ILFs).

This example explains how to create a MED in aggregate. The

distribution is initially created as an Aggregate object with a degenerate

frequency identically equal to 1 claim to focus on the severity.

We then explain how frequency mixing interacts with a mixed severity.

The next table of exponential means and weights appears on slide 24 of Li Zhu, Introduction to Increased Limits Factors, 2011 RPM Basic Ratemaking Workshop,, titled a “Sample of Actual Fitted Distribution”. At the time, it was a reasonable curve for US commercial auto. We will use these means and weights.

Here the DecL to create this mixture.

In [14]: med = build('agg Decl:MED '

....: '1 claim '

....: 'sev [2.764e3 24.548e3 275.654e3 1.917469e6 10e6] * '

....: 'expon 1 '

....: 'wts [0.824796 0.159065 0.014444 0.001624, 0.000071] '

....: 'fixed')

....:

In [15]: qd(med)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1 0

Sev 13990 13798 -0.013708 12.034 12.203 103.79 103.76

Agg 13990 13798 -0.013708 12.034 12.203 103.79 103.76

log2 = 16, bandwidth = 4000, validation: fails sev mean, agg mean.

Note

Currently, it is necessary to enter a dummy shape parameter 1 for the exponential, even though it does not take a shape. This is a known bug in the parser.

The exponential distribution is surprisingly thick-tailed. It can be

regarded as the dividing line between thin and thick tailed distributions.

In order to achieve good accuracy, the modeling increases the number of

buckets to \(2^{18}\) (i.e., log2=18) and uses a bucket size bs=500.

The dataframe report_df is a more detailed version of the audit dataframe

that includes information from statistics_df about each severity component.

(The reported claim counts are equal to the weights and cannot be interpreted

as fixed frequencies. They can be regarded as frequencies for a Poisson or

mixed Poisson.)

In [16]: med.update(log2=18, bs=500)

In [17]: qd(med)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 1 0

Sev 13990 13987 -0.00022819 12.034 12.037 103.79 103.72

Agg 13990 13987 -0.00022819 12.034 12.037 103.79 103.72

log2 = 18, bandwidth = 500, validation: fails sev mean, agg mean.

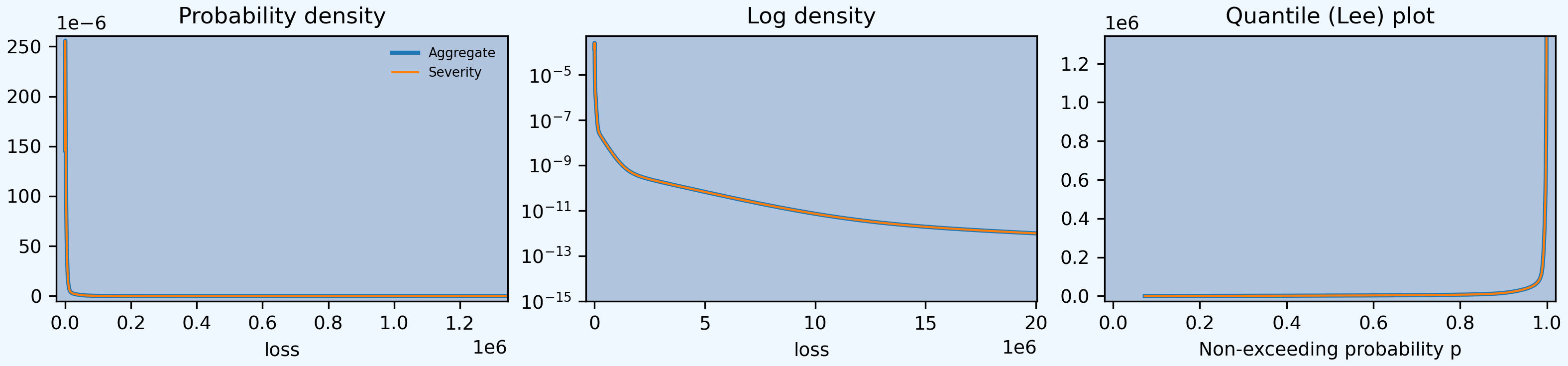

The middle diagnostic plot, the log density, shows the mixture components.

In [18]: med.plot()

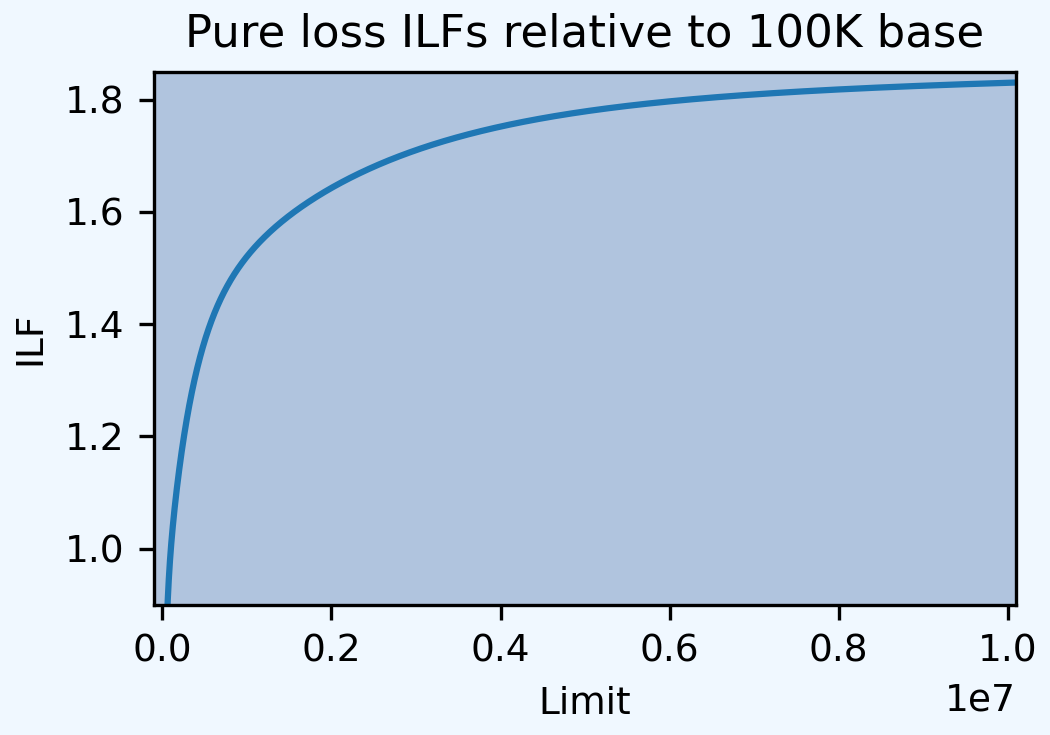

The density_df dataframe includes a column lev. From this we can pull

out ILFs. Zhu reports the ILF at 1M equals 1.52.

In [19]: qd(med.density_df.loc[1000000, 'lev'] / med.density_df.loc[100000, 'lev'])

1.5204

Here is a graph of the ILFs by limit.

In [20]: base = med.density_df.loc[100000, 'lev']

In [21]: ax = (med.density_df.lev / base).plot(xlim=[-100000,10.1e6], ylim=[0.9, 1.85],

....: figsize=(3.5, 2.45))

....:

In [22]: ax.set(xlabel='Limit', ylabel='ILF', title='Pure loss ILFs relative to 100K base');

2.4.6.2. Saving to the Knowledge

We can save the MED severity in the knowledge and then refer to it by name.

In [23]: build('sev COMMAUTO [2.764e3 24.548e3 275.654e3 1.917469e6 10e6] * '

....: ' expon 1 wts [0.824796 0.159065 0.014444 0.001624, 0.000071]');

....:

In [24]: a05 = build('agg DecL:05 [20 8 4 2] claims [1e6, 2e6 5e6 10e6] xs 0 '

....: 'sev sev.COMMAUTO fixed',

....: log2=18, bs=500)

....:

In [25]: qd(a05)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 34 0

Sev 11973 11970 -0.00026506 6.328 6.3298 31.665 31.665

Agg 4.0708e+05 4.0697e+05 -0.00026506 1.0852 1.0855 5.4306 5.4305

log2 = 18, bandwidth = 500, validation: fails sev mean, agg mean.

2.4.6.3. Different Distributions

The kind of distribution can vary across mixtures. In the following, exposure varies for each curve, rather than using weights, see Vectorization: Limit Profiles and Mixed Severity.

In [26]: a06 = build('agg DecL:06 [100 200] claims '

....: '5000 xs 0 '

....: 'sev [gamma lognorm] [100 150] cv [1 0.5] '

....: 'mixed gamma 0.5',

....: log2=16, bs=2.5)

....:

In [27]: qd(a06.report_df.iloc[:, :-2])

view 0 1 independent mixed

statistic

name DecL:06 DecL:06 DecL:06 DecL:06

limit 5000 5000 5000 5000

attachment 0 0 0 0

el 10000 30000 40000 40000

freq_m 100 200 300 300

freq_cv 0.5099 0.50498 0.37712 0.50332

freq_skew 1.0002 1 0.80295 1

sev_m 100 150 133.33 133.33

sev_cv 1 0.5 0.65551 0.65551

sev_skew 2 1.625 1.4508 1.4508

agg_m 10000 30000 40000 40000

agg_cv 0.51962 0.50621 0.40127 0.50474

agg_skew 1.0022 1.0002 0.88112 1.0001

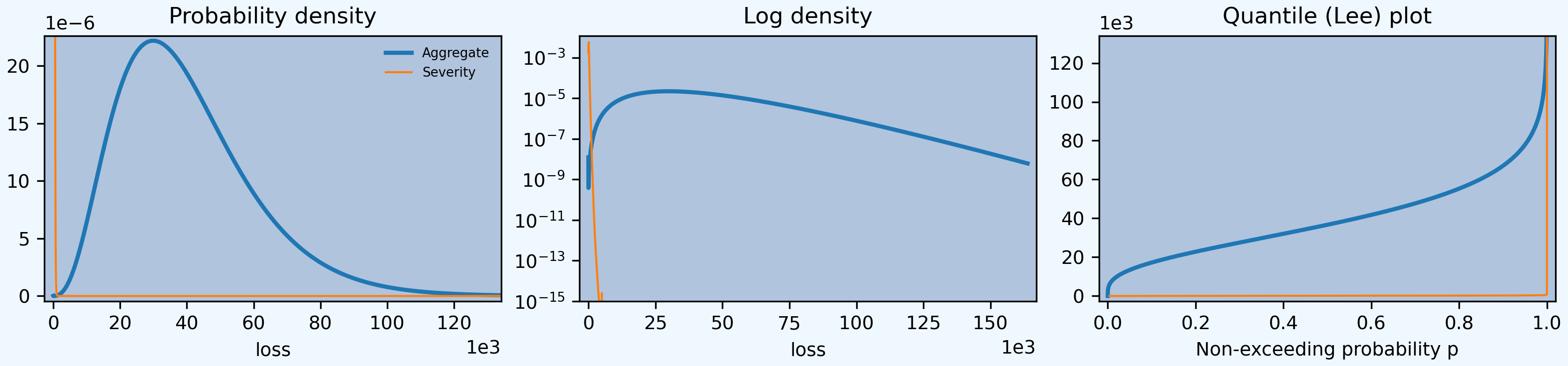

In [28]: a06.plot()

Using a Delaporte (shifted) gamma mixing often produces more realistic output than a gamma, avoiding very good years.

In [29]: a07 = build('agg DecL:07 [100 200] claims '

....: '5000 xs 0 '

....: 'sev [gamma lognorm] [100 150] cv [1 0.5] '

....: 'mixed delaporte 0.5 0.6',

....: log2=18, bs=2.5)

....:

In [30]: qd(a07.report_df.iloc[:, :-2])

view 0 1 independent mixed

statistic

name DecL:07 DecL:07 DecL:07 DecL:07

limit 5000 5000 5000 5000

attachment 0 0 0 0

el 10000 30000 40000 40000

freq_m 100 200 300 300

freq_cv 0.5099 0.50498 0.37712 0.50332

freq_skew 2.4145 2.4561 1.9682 2.4705

sev_m 100 150 133.33 133.33

sev_cv 1 0.5 0.65551 0.65551

sev_skew 2 1.625 1.4508 1.4508

agg_m 10000 30000 40000 40000

agg_cv 0.51962 0.50621 0.40127 0.50474

agg_skew 2.3386 2.4456 2.1507 2.4582

In [31]: a07.plot()

2.4.6.4. Severity Mixtures and Mixed Frequency

All severity components in an aggregate share the same frequency mixing value, inducing correlation between the parts. An Aon study, Aon Benfield [2015], shows that commercial auto has parameter uncertainty CV around 25%. Building with

In [32]: a08 = build('agg DecL:08 '

....: '500 claims '

....: '500000 xs 0 sev sev.COMMAUTO '

....: 'poisson'

....: , approximation='exact')

....:

In [33]: a09 = build('agg DecL:09 '

....: '500 claims '

....: '500000 xs 0 sev sev.COMMAUTO '

....: 'mixed gamma 0.25'

....: , approximation='exact')

....:

In [34]: qd(a08)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 500 0.044721 0.044721

Sev 10266 10266 -4.9496e-05 3.9519 3.9522 9.4914 9.4913

Agg 5.1332e+06 5.1329e+06 -4.9496e-05 0.18231 0.18232 0.41833 0.41833

log2 = 16, bandwidth = 200, validation: not unreasonable.

In [35]: qd(a09)

E[X] Est E[X] Err E[X] CV(X) Est CV(X) Skew(X) Est Skew(X)

X

Freq 500 0.25397 0.50006

Sev 10266 10264 -0.0001979 3.9519 3.9528 9.4914 9.491

Agg 5.1332e+06 5.1321e+06 -0.0001979 0.30941 0.30943 0.55969 0.5597

log2 = 16, bandwidth = 400, validation: fails sev mean, agg mean.

The effect of shared mixing is shown in report_df. In order to focus on the mixing and ease the computational

burden, apply a 500,000 policy limit to model a self-insured retention.

Assume a claim count of 500 claims; for smaller portfolios the impact of mixing is less pronounced because idiosyncratic process risk dominates.

The independent column in report_df shows statitics assuming the mixture components are independent; mixed includes the effect of shared mixing variables.

The next block shows results with a Poisson frequency, where there is no mixing. The independent and mixed columns are identical.

In [36]: qd(a08.report_df.drop(['name']).iloc[:, :-2])

view 0 1 2 3 4 independent mixed

statistic

limit 5e+05 5e+05 5e+05 5e+05 5e+05 5e+05 5e+05

attachment 0 0 0 0 0 0 0

el 1.1399e+06 1.9524e+06 1.6662e+06 3.5738e+05 17314 5.1332e+06 5.1332e+06

freq_m 412.4 79.532 7.222 0.812 0.0355 500 500

freq_cv 0.049243 0.11213 0.37211 1.1097 5.3074 0.044721 0.044721

freq_skew 0.049243 0.11213 0.37211 1.1097 5.3074 0.044721 0.044721

sev_m 2764 24548 2.3072e+05 4.4013e+05 4.8771e+05 10266 10266

sev_cv 1 1 0.73847 0.29449 0.12909 3.9519 3.9519

sev_skew 2 2 0.39392 -2.071 -5.6054 9.4914 9.4914

agg_m 1.1399e+06 1.9524e+06 1.6662e+06 3.5738e+05 17314 5.1332e+06 5.1332e+06

agg_cv 0.06964 0.15858 0.46257 1.1569 5.3515 0.18231 0.18231

agg_skew 0.10446 0.23787 0.54133 1.1826 5.3739 0.41833 0.41833

This block shows mixed gamma (negative binomial) frequency. There are two differences: the individual components have higher CVs (they asymptotically approach 25% for a large portfolio), and the mixed column includes correlation between units (aggregate CV is greater than independent). Glenn Meyers had the idea of using shared mixing variables to ensure aggregate portfolio dynamics are not influenced by how the portfolio is split into units.

In [37]: qd(a09.report_df.drop(['name']).iloc[:, :-2])

view 0 1 2 3 4 independent mixed

statistic

limit 5e+05 5e+05 5e+05 5e+05 5e+05 5e+05 5e+05

attachment 0 0 0 0 0 0 0

el 1.1399e+06 1.9524e+06 1.6662e+06 3.5738e+05 17314 5.1332e+06 5.1332e+06

freq_m 412.4 79.532 7.222 0.812 0.0355 500 500

freq_cv 0.2548 0.274 0.44829 1.1376 5.3133 0.21474 0.25397

freq_skew 0.50009 0.5021 0.58771 1.1925 5.3251 0.473 0.50006

sev_m 2764 24548 2.3072e+05 4.4013e+05 4.8771e+05 10266 10266

sev_cv 1 1 0.73847 0.29449 0.12909 3.9519 3.9519

sev_skew 2 2 0.39392 -2.071 -5.6054 9.4914 9.4914

agg_m 1.1399e+06 1.9524e+06 1.6662e+06 3.5738e+05 17314 5.1332e+06 5.1332e+06

agg_cv 0.25952 0.29605 0.52581 1.1836 5.3573 0.22858 0.30941

agg_skew 0.50102 0.51935 0.6983 1.2604 5.3913 0.42255 0.55969